like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Forex trading idea

US job market may be near tipping point, research shows

JACKSON HOLE, Wyoming, Aug 23 (Reuters) - As inflation fell fast in 2023 and continued to slow this year, Federal Reserve officials were cheered that the steam seemed to come out of the U.S. economy not through rising unemployment but rather a decline in the large number of job openings businesses posted during the peak of the pandemic-era labor shortage.

But the economy may now be near a tipping point where a continued drop in job openings will translate into faster increases in unemployment, an argument in favor of the Fed beginning to cut interest rates to guard the labor market, according to new research presented on Friday at the Kansas City Fed's annual economic conference in Jackson Hole, Wyoming.

"Policymakers face two risks: being too slow to ease policy, potentially causing a 'hard landing' with high unemployment ... or cutting rates prematurely, leaving the economy vulnerable" to rising inflation, economists Pierpaolo Benigno of the University of Bern and Gauti B. Eggertsson of Brown University wrote in their research paper. Based on their new analysis of the job market, "our current assessment suggests the former risk outweighs the latter."

Fed officials appear to have reached the same conclusion, with reductions to the U.S. central bank's benchmark policy rate expected to begin at the upcoming Sept. 17-18 meeting and likely continue in subsequent sessions.

Still, the new research adds further detail to several ongoing Fed debates by combining in a single economic model two key relationships; one between the unemployment rate and rate of inflation, known as the Phillips Curve, and one between the job vacancy rate and the unemployment rate, known as the Beveridge Curve.

The paper suggests, for example, that when labor markets are loose, policymakers can continue to regard supply shocks as of less consequence to underlying inflation and to appropriate monetary policy. It takes a combination of supply problems and tight labor markets, they conclude, to generate the sort of persistent inflation surge the U.S. just experienced.

It also adds a dose of caution to a debate that has been underway at the Fed now for years over what constitutes the maximum level of employment that is consistent with the central bank's 2% inflation target - Congress has made the Fed responsible for both objectives - and what risks policymakers may need to take with the job market to keep inflation low and stable.

The answer, the research suggests, is that it depends heavily on the underlying demand and supply of labor, which Benigno and Eggertsson capture by focusing less on the unemployment rate itself and more on the ratio of job openings to the number of people looking for work.

When the number of openings and the number of unemployed jobseekers is close to balance, taming an inflation outbreak involves a large rise in joblessness, as happened in the 1970s when the U.S. experienced high inflation and unemployment simultaneously.

When the labor market is tight, by contrast, with demand for workers high relative to their numbers, "the cost of reducing inflation in terms of increased unemployment is relatively low," the researchers concluded.

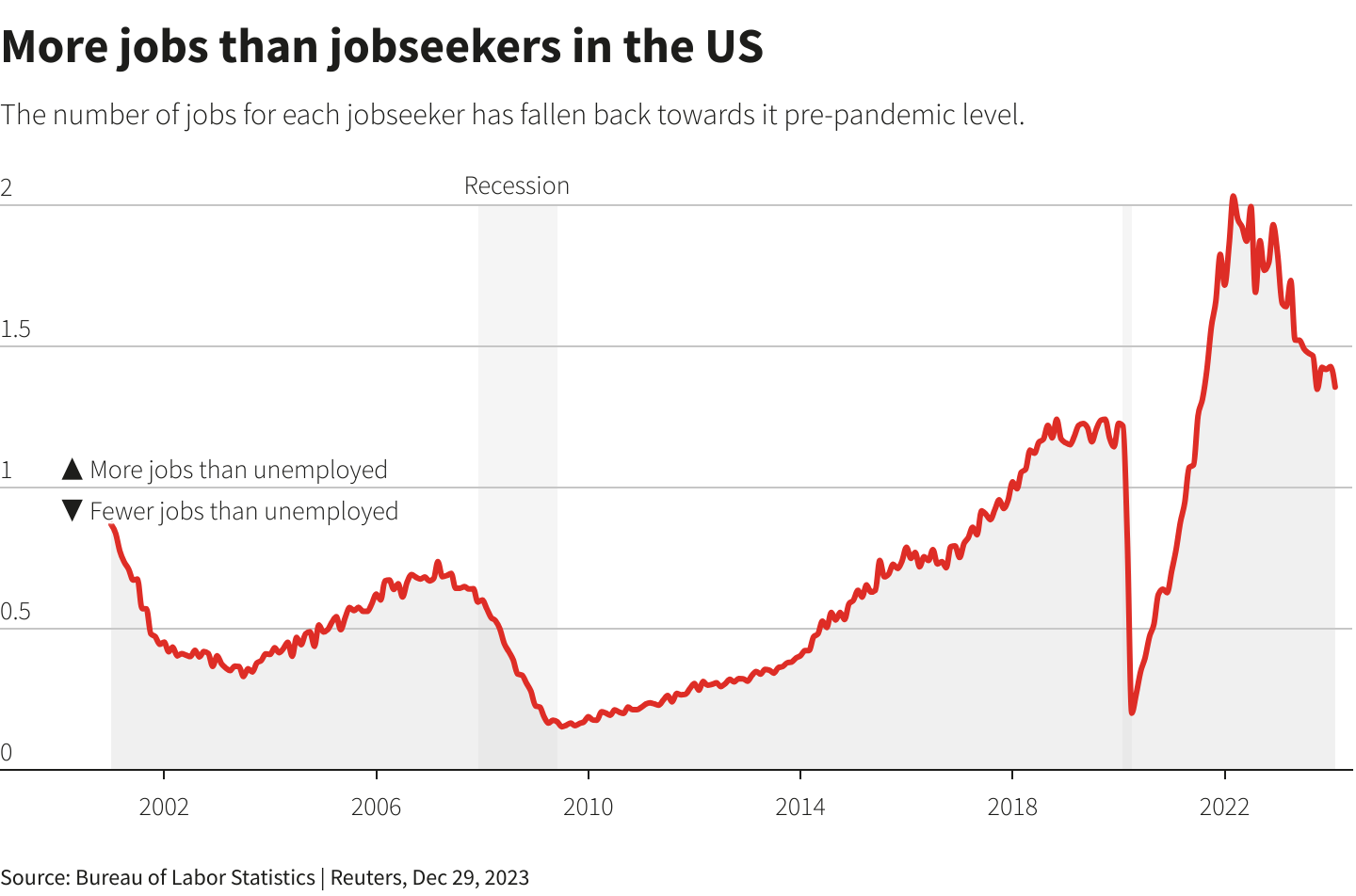

The job-openings-to-unemployed metric became important in recent U.S. central bank discussions, a focus of policymakers and Fed Chair Jerome Powell in particular when it spiked above the 2-to-1 mark during the reopening from the COVID-19 pandemic, with firms posting two jobs for every available body.

RISKS OF RUNNING 'HOT'

Analysis by Fed Governor Christopher Waller and staff economist Andrew Figura in 2022 suggested that bringing that ratio closer to balance could lower inflation without the unemployment rate rising much, if at all, a counter to predictions by other top economists that unemployment rates as high as 10% might be needed to tame the worst U.S. inflation outbreak in 40 years.

Their findings have been proven in practice, with the ratio now down to 1.2, the Fed's preferred measure of inflation down to 2.5% from a peak of more than 7% in June of 2022, and the unemployment rate until recently remaining below 4%.

Yet even the current ratio is above the one-to-one level that the researchers say seems to mark the breakpoint - at least approximately - between labor market conditions that generate inflation and those that don't. Since World War One, they found, most inflation outbreaks have involved job openings rising above the number of people who are out of work and looking for a job.

After years of persistently low inflation and falling unemployment in the decade before the pandemic, Fed officials had felt they could potentially run the economy "hot," to the benefit of workers, with little chance of rising prices. The new research suggests there are risks in that approach.

The researchers also warn that if the openings-to-unemployed ratio continues to slide, the economy is at a point where unemployment could rise fast, a fear Waller himself has recently raised.

In the current situation, they project the Fed could achieve its inflation objective, with the number of job openings in balance with the number of unemployed, at a jobless rate of around 4.4% - still below the long-term average for the U.S. but significantly higher than the experience of the past roughly two years.

Once the one-to-one threshold is passed, "further reductions in inflation are likely to be more costly," they wrote, with a job openings-to-unemployed ratio of 0.8 - with fewer jobs than people looking - causing unemployment to rise above 5%.

Sign up here.

https://www.reuters.com/markets/us/us-job-market-may-be-near-tipping-point-research-shows-2024-08-23/