2024-08-27 08:15

The distributions were made in liquid cryptocurrency and cash at Jan. 16 prices to roughly two-thirds of all eligible creditors by number and 93% by value. Celsius has distributed over $2.53 billion to more than 251,000 creditors as part of its bankruptcy process. Another 121,000 eligible creditors have yet to successfully claim their distribution. Celsius' bankruptcy administrator has distributed more than $2.53 billion to some 251,000 creditors, it said in its first status report on the payouts. The disbursements were made in liquid cryptocurrency and cash at Jan. 16 prices. They cover roughly two-thirds of all eligible creditors of the crypto lender by number and about 93% of the eligible value, the administrator said in a Monday court filing. Another 121,000 eligible creditors with an average distribution of approximately $1,500 have yet to successfully claim their distributions. "Approximately 64,000 of these remaining creditors have a distribution of less than $100, and approximately 41,000 more have a distribution of between $100 and $1,000," the filing said. "Given the small amounts at issue for many of these creditors, they may not be incentivized to take the steps needed to successfully claim a distribution." The bankruptcy is officially closed after the United States Southern District of New York Bankruptcy Court approved a reorganization plan in November. The plan to distribute more than $3 billion to Celsius creditors was determined at the end of January. In the seven months since, the "distribution process contemplated by the Plan is likely the most complicated and ambitious distribution process ever attempted in a chapter 11 case," the filing said. The plan involves distributing liquid crypto, cash and common stock in MiningCo – the new company that evolved out of Celsius – to around 375,000 creditors in over 165 different countries. Because "Celsius was not a fully regulatorily compliant business prepetition, and many regulators were pursuing enforcement actions against the Debtors" the complexity of the distribution process has increased, the filing said. Earlier this month, Celsius asked the bankruptcy court to order Tether to relinquish bitcoin worth some $3.3 billion based on allegations that Tether labeled a "shakedown" litigation that it would contest. Read More: Celsius to Distribute $3B Crypto to Creditors as Firm Emerges From Bankruptcy https://www.coindesk.com/business/2024/08/27/celsius-bankruptcy-plan-administrator-pays-out-over-25b/

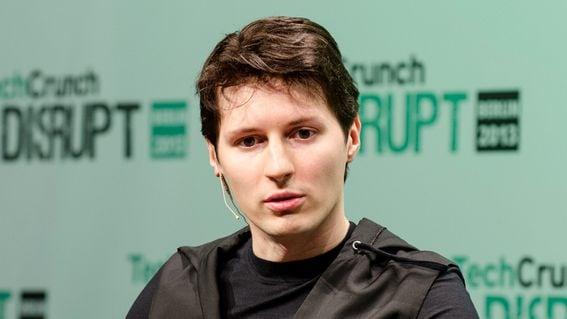

2024-08-27 05:39

A press release from French prosecutors said he could be released Wednesday, but the market isn't confident he'll be out by then. Telegram CEO Pavel Durov was arrested in France over the weekend. Bettors on Polymarket are putting money on him remaining in custody after the 96-hour deadline prescribed by courts, as there's a growing belief he may be formally charged. Telegram CEO Pavel Durov could be free to go as soon as Wednesday local time, French prosecutors said. However, Polymarket isn't confident he'll be released in August, with bettors putting money on a release before the end of September. Durov has not yet been formally charged, prosecutors said. Instead, he is being held as part of an investigation that stems as a result of crimes allegedly planned or broadcasted on Telegram, including money laundering, drug trafficking, child pornography, and non-cooperation with law enforcement. Bettors say there's a 72% chance he'll be out before October, with shares of the yes side trading at 72 cents. Each share pays out $1 in USDC, a stablecoin, if the prediction comes true, and $0 if it does not. As Durov was arrested on Saturday, August 24, 2024, at 8:00 PM local time when his plane landed at Le Bourget airport, a general aviation airport north of Paris, he could be held until Wednesday, August 28, 2024, at 8:00 PM, but bettors have their money on an extended stay. The press release indicates that if investigators uncover sufficient evidence during questioning, Durov's detention could be extended, or he could be formally charged and moved to pre-trial detention. This possibility likely fuels market skepticism about his release by the initial deadline. Toncoin (TON) is trading above $5.38, according to CoinDesk Indices data, down 6.8%, while the CoinDesk 20 (CD20) a measure of the largest digital assets, is down 1.87%. https://www.coindesk.com/markets/2024/08/27/telegram-ceo-pavel-durov-could-be-free-by-october-polymarket/

2024-08-26 23:19

Newspapers are dead. Can Superbasedd make it with a monthly glossy? SALT LAKE CITY — Crypto's got a demographic problem: too many men. The scene's newest culture magazine wants to leverage that imbalance harder than a memecoin trader's credit line. Superbasedd, a month-old wannabe lifestyle rag with deep LA roots, is planning to stand up a print publication that appeals to the crypto space's baser instincts. On the front page: a cover girl. On the back: an authoritative-looking male startup founder. And in between: tales from crypto's trader trenches. "We're all dudes, we're all degenerates, and if there's one thing I know about degenerate dudes, they love women. And that's a really good way to start a brand," said Superbasedd founder Steve McHugh. Women are the "bait" for what McHugh and his co-founders described as an authoritative but edgy magazine that brings web3 culture to male audiences over the world. Lure in readers with alluring photos and then smack 'em with "really good culture and profile pieces highlighting this industry." Whether sex+culture can still sell magazines is an open question. Playboy is only just plotting its return to newstands with an annual glossy edition. That once-vaunted dude institution published articles that had appeal for pretty much anyone up on the culture. Meanwhile, Superbasedd's content will tap a far-smaller pool of younger guys who like crypto, though McHugh said its female-forward marketing targets "guys" at large. Superbasedd's "dangerous" content strategy complements its staff. McHugh's lanky business partner Jake Hillhouse was slated for an undercard bout at the upcoming Karate Kombat fight night in Singapore in a few weeks. Then he blew up his elbow in a dune buggy accident; Hillhouse showed up to our impromptu interview in an arm sling and a hospital wristband barely 48 hours old. Still, the publication has some capital to burn. Earlier this month Superbasedd generated almost $1.1 million by selling NFTs that come with a three year subscription, which hasn't yet launched. Another subscription option will offer one year of access for $99. McHugh plans to feature a part of crypto that the established media brands are either missing or have abandoned. Of the major crypto-focused publications, only Decrypt has reporters dedicated to documenting the often zany ways this industry's participants express themselves. Those stories often veer toward the insane, and even obscene. Seemingly every week the memecoin factory Pump.Fun sees another ridiculous stunt of token creators embarrassing, or injuring themselves to make the token's price climb higher, like that time a guy smoked crack and had his head shaved by a stripper on a livestream. "Our edginess is going to start with the girls and then end with crackhead dev," said Hillhouse. Superbasedd plans to tell those tales alongside in-depth features of the leading male figures in crypto. During our interview McHugh toyed with getting Solana's founders Raj Gokal and Anatoly Yakovenko for the first edition, coming in October. There's something deeply strange about a crypto-focused publication betting on print for distribution. It's a critically endangered medium within the twenty-first century's fast-dying institution, journalism. Superbasedd's team thinks tactile formats will nonetheless work when paired with the lessons of the Instagram age. First, use pictures of sexy women to capture guys' attention. Then, hold that attention with snappy articles that tell stories in digestible ways, perhaps by outlining them like a thread on X. McHugh harbors visions of elevating Superbasedd into "high snobciety" with enough caché to sit atop any moneyed coffee table in the Hollywood Hills. he's betting that America's trickle-down celebrity culture should make the magazine broadly relevant. For now, though, Superbasedd is leaning hard into overtures that would only mean something to the most dedicated NFT swapper on Solana, the chain for which this magazine's publishers seem most aligned. Superbasedd recently bought the intellectual property for Catalina Whale Mixer – a once-popular NFT collection with a $2.5 million market cap – for less than $50,000, according to McHugh. It is planning to take over the Thug Birdz NFT collection next. The publication's three-man team came to mtnDAO to work on outreach to other crypto founders, said McHugh, a two-time attendee. In-person crypto workspaces can help startups move faster on the strange business propositions of this industry, like standing up a token. Their background diverges from the norm at this twice-a-year hacker house, now in its sixth edition. Every August and February a growing flock of Solana developers decamp to Salt Lake City for one month of collaborating on projects, which often tilt toward new financial primitives. "We're not devs, we're not builders, we're startup, content guys," McHugh said. https://www.coindesk.com/business/2024/08/26/upstart-degenerate-crypto-culture-publication-bets-on-print/

2024-08-26 20:01

BlackRock's ETHA and other Ethereum funds have collected billions of dollars worth of inflows. Massive outflows from the Grayscale Ethereum Trust (ETHE) have overshadowed that, though. At first glance, spot ether ETFs appear to have bled money, but it's more complicated than that. BlackRock's ETHA was the seventh-most-successful ETF launch this year with over a billion dollars worth of inflows. Other ether funds have seen brisk demand as well. Grayscale's ETHE product lost billions, offsetting the overall success of the funds. The headline could easily be this: Recently launched ether exchange-traded funds have been a dud. After all, investors have removed $465 million of assets in total from the nine funds that began trading in the U.S. a month ago. Dig a little deeper and you'll find success, however. BlackRock’s iShares Ethereum Trust (ETHA) just passed $1 billion of net inflows, making it the seventh-most-successful ETF launch this year, according to Nate Geraci, president of the ETF Store. Fidelity’s Advantage Ether ETF and the Bitwise Ethereum ETF have taken in $390 million and $312 million, respectively, according to data from Farside Investors. But back to the overall removal of money, which stems from the billions of dollars yanked from the fact that Grayscale Ethereum Trust (ETHE). That product was first sold to investors in 2017 and began trading publicly in 2019 – albeit in a less-appealing trust format. It was turned into an ETF in July as new funds from the likes of BlackRock sprung into existence. The Grayscale product features a much higher fee for investors, meaning many might want to shift to cheaper fund. Exclude the massive Grayscale outflows and investors have allocated over $2 billion to the other funds in the first five weeks. “The fact that over $2 billion has been purposefully allocated to the other spot ether ETFs is a good sign as it shows that investors want ether exposure,” Geraci said. “While not the dazzling debut we saw from spot bitcoin ETFs, I think spot ether ETFs have clearly had a successful first month and I expect this to continue.” In regards to Grayscale, Geraci believes that the outflows muddy the waters and make it difficult to get a clear picture of how much demand there is for the funds. “We simply don’t know all of the underlying motivations of ETHE sellers, which is why I think it’s important to look beyond that product.” Demand is likely to continue and grow over the next few months, said Sui Chung, CEO of index provider CF Benchmarks. He predicts that more wealth managers will offer the products to their clients. “We anticipate flows into ETH ETFs will continue to climb once wealth managers and financial advisors complete the education process for what ETH is, its utility and why they should hold it alongside their BTC ETF,” he said. “The educational process will expose investors to the Ethereum economy and highlight its key differences to Bitcoin, making it abundantly clear that the allocation drivers are different and both belong in a balanced investment portfolio.” Spot bitcoin ETFs, which began trading in January, have seen nearly $18 billion in inflows. Investors have allocated roughly $20 billion into BlackRock’s product, which is mostly offset by $17 billion worth of outflows out of the Grayscale Bitcoin Trust (GBTC), another Grayscale fund that existed for years as a trust before converting to an ETF this year. https://www.coindesk.com/business/2024/08/26/ether-etfs-have-bled-money-but-thats-not-the-whole-story/

2024-08-26 19:07

The securities regulator says Abra sold half a billion dollars in unregistered Abra Earn while also operating without registration as an investment company. Crypto platform Abra is the latest to agree to a settlement with the Securities and Exchange Commission over accusations of unregistered securities. The settlement focused on its Abra Earn product, which the agency said had amassed as much as $500 million at one point. Abra has agreed to a settlement with the U.S. Securities and Exchange Commission over accusations the platform, owned by Plutus Lending, inappropriately pushed Abra Earn to customers when the product qualified as a security that should have been registered, the agency said Monday. Starting in 2020, the crypto investment platform and lender began offering Abra Earn to customers, promising high levels of returns for letting the firm use their assets, the SEC said in its complaint. At one point, the program had about $600 million, and almost $500 million was from U.S. investors. Also, for at least two years, Abra operated as an investment company without registering, the SEC said. The company, which accepted the sanction without admitting or denying the allegations, consented to a prohibition from violating the U.S. securities-registration rules and whatever civil penalties a court deems appropriate. The company had already similarly settled with 25 states for operating without licenses and agreed to return as much as $82 million to customers in the U.S. Read More: Abra Settles With 25 States for Operating Without Licenses, Will Return Up to $82M to U.S. Customers "Abra sold nearly half a billion dollars of securities to U.S. investors without complying with registration laws designed to ensure that investors have sufficient, accurate information to make informed decisions before they invest,” said Stacy Bogert, associate director of the SEC’s Division of Enforcement, in a statement. She added that the agency is governed by "economic realities, not cosmetic labels." A lawyer representing Abra didn't immediately respond to a request for comment. Monday's action is Abra's second SEC settlement, after it agreed to pay $150,000 each to it and the Commodity Futures Trading Commission in 2020 to end an investigation into its swaps product. https://www.coindesk.com/policy/2024/08/26/us-sec-settles-with-abra-over-unregistered-sales-of-securities/

2024-08-26 18:46

The federal regulator sued Kraken in California last year, alleging that the crypto company failed to register with the SEC as a broker, exchange or clearinghouse. A federal judge ruled that the Securities and Exchange Commission had brought plausible allegations against crypto exchange Kraken, meaning its lawsuit will proceed to trial. The SEC sued Kraken last year, alleging the exchange failed to register as a broker, exchange or clearinghouse. The U.S. Securities and Exchange Commission’s (SEC) lawsuit against Kraken will proceed to trial, a California judge ruled Friday. The SEC sued Kraken in the Northern District of California last November, alleging that the crypto exchange had violated federal securities laws by failing to register with the agency as a broker, clearinghouse or exchange. The complaint requested that Kraken be permanently enjoined from further securities violations, as well as disgorgement of its “ill-gotten gains” and other civil penalties. Kraken is just one of the major crypto exchanges currently caught up in the SEC’s legal dragnet. Similar lawsuits were filed against Binance and Coinbase last year, alleging that both exchanges also violated securities laws by failing to register as brokers, clearinghouses and exchanges with the SEC. Both Coinbase and Binance attempted to get the cases against them thrown out – and both failed, with the judges overseeing each case ruling that the bulk of the cases against them can move forward to trial. Now, Kraken’s motion to dismiss the SEC’s case has also been denied. In his Aug. 23 ruling, U.S. District Court Judge William H. Orrick of the Northern District of California wrote that the SEC has “plausibly alleged that at least some of the cryptocurrency transactions that Kraken facilitates on its network constitute investment contracts, and therefore securities, and are accordingly subject to securities laws.” Kraken’s ill-fated motion to dismiss, filed in February, argued that the SEC had failed to state a claim – essentially, that the facts in the case, even if true, did not constitute a violation of the law – arguing that cryptocurrencies do not meet the definition of a security as defined by the Howey Test. Orrick agreed with Kraken in part, ruling that the cryptocurrencies named by the SEC in its lawsuit were “not themselves investment contracts" – an argument that SEC attorneys have distanced themselves from in hearings in some of these cases. “Numerous courts have distinguished between the digital assets and the offers to sell them before engaging in an analysis of whether cryptocurrency transactions constitute investment contracts. The distinction is valuable,” Orrick wrote. “Although the way the SEC labels the crypto assets at issue – as ‘crypto asset securities’ – is unclear at best and confusing at worst, I do not understand the SEC to be alleging that the individual cryptocurrency tokens in which Kraken enables transactions are themselves securities." "The meat of the SEC’s pleadings alleges that during their initial offerings and throughout subsequent transactions on Kraken, those assets were offered as, or sold as, investment contracts. This is an acceptable framing, and one that the SEC has repeatedly advanced in other cases," the judge added. Kraken’s Chief Legal Officer Marco Santori celebrated this section of Orrick’s ruling on X (formerly Twitter) writing: “Today, the Federal Court for the Northern District of California ruled, as a matter of law, that none of the tokens trading on Kraken are securities. This is a significant win for Kraken, for the principle of clarity and for crypto users everywhere. It also confirms Kraken’s long-standing position that it does not list securities.” A representative for Kraken declined to comment beyond Santori’s X post. But just because Orrick ruled that the cryptocurrencies themselves were not securities, it does not mean that the purchase and sale of them cannot plausibly be considered an investment contract. “Orange groves are no more securities than cryptocurrency tokens are,” Orrick wrote. “But the contracts surrounding the sale of both may form an investment contract, bringing them within the purview of the [Exchange] Act.” Kraken’s motion to dismiss also argued that the case should be tossed out under the Major Questions Doctrine – a legal principle established by the Supreme Court that holds that agencies should not expand their regulatory powers without clear authorization from Congress. But like other judges asked to weigh in on the doctrine, Orrick disagreed with Kraken, stating that the $3 trillion cryptocurrency industry is simply not big or important enough in the U.S. economy or political sphere to invoke the Major Questions Doctrine. “Other courts have already considered whether similar claims brought by the SEC violate the major questions doctrine and found that they do not,” Orrick wrote. “The same is true here…while cryptocurrency itself is a relatively novel financial instrument, the principles driving the SEC’s attempt to assert regulatory authority over it are not new.” Both parties are required to submit a Joint Statement by Oct. 8, which will include a proposed case schedule and trial date. https://www.coindesk.com/policy/2024/08/26/secs-case-against-kraken-will-proceed-to-trial-california-judge-rules/