2023-10-03 04:35

CRUDE OIL, WTI, RETAIL TRADER POSITIONING, TECHNICAL ANALYSIS – IGCS COMMODITIES UPDATE Crude oil prices fell the most over 2 days since early June Retail traders are increasingly building upside exposure This is an early warning sign that WTI may continue lower Over the past 2 days, crude oil prices have fallen more than -3.4 percent. This marked the worst 2-day performance since early June. In response, retail traders have begun increasing upside exposure. This can be seen by taking a look at IG Client Sentiment (IGCS), which often works as a contrarian indicator. With that in mind, could further pain be in store for oil next? Crude Oil Sentiment Outlook - Bearish According to IGCS, only about 45% of retail traders are net-long crude oil. Since most are still biased to the downside, this continues to suggest price may rise down the road. That said, upside exposure has increased by 8.8% and 11.11% compared to yesterday and last week, respectively. With that in mind, recent changes in bets warn that the current price trend may soon reverse lower. On the daily chart below, we can see that WTI has effectively rejected November highs, which make for a zone of resistance between 92.43 – 93.72. This also followed negative RSI divergence, which showed that upside momentum was fading. Since then, prices have extended lower, recently taking out the 20-day moving average. Oil is also testing a push under the 61.8% Fibonacci extension level at 88.75. Confirming a breakout lower may open the door to an increasingly downward technical bias. Such an outcome places the focus on the 50-day moving average, and the 84.84 inflection point from August. These may hold as support. Crude Oil Daily Chart Chart Created in Trading View https://www.dailyfx.com/analysis/crude-oil-vulnerable-as-recent-drop-pushes-retail-traders-to-build-upside-exposure-20231002.html

.png)

2023-10-03 04:33

BRITISH POUND, GBP/USD, GBP/JPY – TECHNICAL UPDATE: The British Pound is appearing more vulnerable GBP/USD downtrend faces next support point GBP/JPY Bearish Death Cross is now in focus The British Pound appears to be increasingly vulnerable against the US Dollar and Japanese Yen from a technical perspective. On the daily chart below, GBP/USD has continued making downside progress in the aftermath of a bearish Head & Shoulders chart formation. Now, recent losses have brought the exchange rate to the 78.6% Fibonacci retracement level of 1.209. There is a positive RSI divergence, which shows that downside momentum is fading. That can at times precede a turn lower. But, the 20- and 50-day moving averages remain sloping lower. These may hold as resistance, maintaining the broader downside focus. Further losses place the focus on the March low of 1.1804. GBP/USD – Daily Chart Chart Created in TradingView The Japanese Yen has been slightly more resilient to the British Pound compared to the US Dollar. GBP/JPY remains idling above the 180.84 support point that has been holding up since September. But, a Bearish Death Cross recently formed between the 20- and 50-day moving averages. This could spell further trouble for the exchange rate. A breakout lower offers a stronger bearish technical bias, exposing the 23.6% Fibonacci retracement level at 179.35. Below that is the 38.2% point of 174.77. Meanwhile, immediate resistance are the near-term moving averages. Breaking above would offer a neutral bias, placing the focus on the August peak of 186.76. GBP/JPY – Daily Chart Chart Created in TradingView https://www.dailyfx.com/analysis/british-pound-technical-outlook-gbp-usd-gbp-jpy-may-fall-as-sterling-remains-pressured-20231003.html

.png)

2023-10-03 04:32

Another push higher in Treasury yields kept risk sentiments broadly in check, as the US 10-year yields surged to touch another new high since 2007 at 4.68%. A lesser-than-expected contraction in US manufacturing purchasing managers index (PMI) reading (49 vs 47.8 est), along with a move in manufacturing employment back into expansion (51.2 vs 48.3 est), may be seen as validation for rates to be kept high for longer, despite some progress in easing prices (43.8 vs 48.6 est). This is further reinforced by comments from several Fed voting members (Michelle Bowman, Michael Barr), with the takeaway being that rates will have to be kept at ‘restrictive level for some time’. The US dollar found its way to a new 11-month high. In return, gold and silver prices head to a near seven-month low. Brent crude prices have also moderated for the third straight day, following a near-term bearish divergence on its daily Relative Strength Index (RSI). For the S&P 500, the index continues to trade in a tight range, attempting to hold above a lower channel trendline support but lacks the conviction to overcome the 4,330 support-turned-resistance level just yet. This may provide a moment of reckoning ahead, where a breakdown of the lower channel trendline could pave the way for further downside to the 4,000 level, just as the weekly RSI is back at its key 50 mid-point level. Market breadth are edging near its June and October 2022 lows, which may call for some dip buyers, but much indecision is still in place for now. Source: IG charts Asia Open Asian stocks look set for a downbeat open, with Nikkei -1.23%, ASX -1.20% and NZX -0.80% at the time of writing, as rising bond yields and a stronger US dollar did not provide much cues for risk-taking. South Korean and China markets are both closed for holidays. Ahead, the interest rate decision from the Reserve Bank of Australia (RBA) will be in focus. Broad expectations are for the RBA to keep its cash rate on hold for the fourth straight meeting, but markets are unconvinced that the peak rate has been seen just yet. Cash rate futures suggest that an additional 25 basis-point (bp) hike is still being priced for early next year to put the terminal rate at 4.35% from current 4.1%. All eyes will be on whether the recent upmove in Australia’s August inflation (5.2% year-on-year vs previous 4.9%) will be sufficient to prompt a more hawkish stance from the central bank, with the RBA likely to keep the option open for “further tightening of monetary policy” – a stance that could be largely unchanged from previous statements. The ASX 200 has registered a new six-month low this week, retracing close to 8% from its July 2023 top. The index is now back to retest a key support level at the 6,900 level, where the lower edge of its long-ranging pattern stands. Failure to defend the 6,900 level could pave the way to retest the 6,730 level, followed by the 6,400 level next. For now, its weekly Moving Average Convergence/Divergence (MACD) is edging into negative territory, with negative momentum broadly in place. Source: IG charts On the watchlist: AUD/NZD broke below key support ahead of RBA, RBNZ’s rate decisions Having largely traded in a range since July this year, the AUD/NZD has broken below its lower consolidation support at the 1.073 level yesterday, which may reflect sellers taking greater control for now. This has brought the pair to a new four-month low, with its daily MACD pushing further into negative territory as a sign of downside momentum. The RBA and the Reserve Bank of New Zealand (RBNZ) rate decisions will be on watch this week, with neither central banks expected to hike rates but policy guidance will be the key focus. Further downside may leave the 1.059 level on watch as the next level of support, while on the upside, 1.073 will now serve as a support-turned-resistance level for buyers to overcome. Source: IG charts https://www.dailyfx.com/news/asia-day-ahead-rba-rate-decision-on-watch-aud-nzd-below-key-support-20231003.html

.png)

2023-10-03 04:29

AUSTRALIAN DOLLAR VS US DOLLAR, NEW ZEALAND DOLLAR, RBA – TALKING POINTS: AUD held early losses after the RBA kept interest rates on hold. AUD/USD looks vulnerable as it tests vital support; AUD/NZD falls below key support. The Australian dollar held early losses after the Reserve Bank of Australia (RBA) kept benchmark interest rates steady, in line with market expectations. RBA kept the benchmark rate steady at 4.1% for the fourth straight month but said some further tightening of monetary policy may be required as inflation remains still too high and the labour market remains strong. The central bank maintained its central forecast for inflation returning to the 2-3% target range by late 2025. Australia's CPI accelerated to 5.2% on-year in August, significantly above the central bank’s 2-3% target range. The recent sharp rise in oil prices poses upside risks to RBA’s inflation forecast and keeps alive the possibility of one more rate hike in this cycle. Markets are pricing in one more RBA rate hike early next year and broadly steady rates thereafter in 2024. AUD/USD 5-minute Chart Chart Created by Manish Jaradi Using TradingView Meanwhile, tentative signs of a trough in manufacturing activity in China are emerging - factory activity expanded for the first time in six months in September. This follows a spate of other indicators in August, including retail sales and easing deflationary pressures, that suggested economic growth could be bottoming in the world’s second-largest economy. Any improvement in China’s growth outlook could bode well for Australia. AUD/USD Daily Chart Chart Created by Manish Jaradi Using TradingView Furthermore, the US Congress agreed on a last-minute deal to prevent a partial government shutdown briefly supporting AUD. However, broader risk appetite has remained in check amid surging US yields driven by higher-for-longer US rates view. Fed Governor Michelle Bowman reinforced the view on Monday saying she remains willing to support another increase in the central bank’s policy rate at a future meeting if incoming data shows progress on inflation has stalled or is too slow. AUD/USD: Testing key support On technical charts, AUD/USD has gone sideways over the past month, with stiff resistance at the late-August high of 0.6525 and quite strong support at the August low of 0.6350. For immediate downside risks to fade, AUD/USD needs to rise above 0.6525. Such a break could open the way toward the 200-day moving average (now at about 0.6675). On the downside, any break below 0.6350 could expose downside risks toward the October 2022 low of 0.6170. AUD/NZD Daily Chart Chart Created by Manish Jaradi Using TradingView AUD/NZD: Attempting to break below key support After remaining sideways for two months, AUD/NZD is attempting to break below the lower end of the range at the July low of 1.0720. Such a move could clear the path initially toward the May low of 1.0550, not too far from the December low of 1.0470. https://www.dailyfx.com/news/australian-dollar-holds-losses-after-rba-stands-pat-aud-usd-tests-key-support-20231003.html

2023-10-02 02:57

Gold: Needs to clear 1987 for the short-term bearish outlook to change On technical charts, gold appears to have settled in a triangle formation in recent weeks. The upper edge of the triangle is a downtrend line from July, while the lower edge of the pattern is a horizontal trendline since June. One reason for the stalled price action is because the yellow metal is flirting with the 200-day moving average. Given the relevance of the long-term moving average, the recent indecision isn’t surprising. XAU/USD Monthly Chart Chart Created Using TradingView Unless XAU/USD is able to break above the July high of 1987, the immediate downside risks are unlikely to fade. On the downside, any break below 1885-1890 would raise the odds of a termination of the uptrend that began in 2022. Such a break could clear the way toward the 200-week moving average (now at about 1810). XAU/USD Weekly Chart Chart Created Using TradingView Importantly, it would raise the odds that the spectacular multi-month rally was corrective and not the start of a new uptrend – a point highlighted in recent months. See “Gold Could Find It Tough to Crack $2000”,published March 28, and “Gold Weekly Forecast: Is it Time to Turn Cautious on XAU/USD?” published April 16. Silver: Key ceiling is at $26.00-$27.00 The rally in the past one year or so has been substantial, but two developments suggest the rally is no more than corrective (correction of the 2021-2022 slide). Firstly, XAG/USD remains well under stiff resistance on a declining trendline since 2020, reinforcing the downtrend. Secondly, the failure, at least so far, to clear the March 2022 peak of 27.00 - the inability to create a higher high reaffirms the lower-high-lower-low structure since 2021. XAG/USD Weekly Chart Chart Created Using TradingView Any break below immediate support on a horizontal trendline at about 22.00 would trigger a bearish triangle with a potential price objective toward the October low of 19.80. Any break below 19.80 would suggest that the rally since 2022 has reversed. Subsequent support is at the 2022 low of 17.50. https://www.dailyfx.com/news/gold-silver-q4-technical-forecast-tide-remains-against-xau-usd-xag-usd-20231001.html

.png)

2023-10-02 02:55

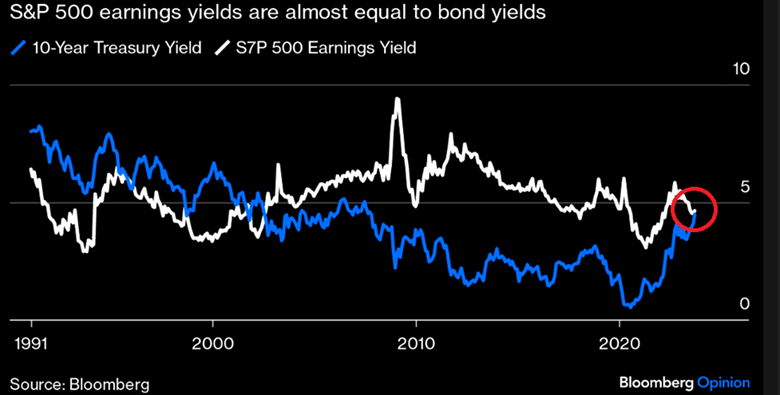

CHOPPY ROAD AHEAD AS HIKING CYCLE NEARS ITS END US equities defied logic for the first half of 2023 but has shown signs of concern more recently as the Fed makes its final policy adjustments before attempting to dismount from its aggressive rate hiking campaign. The fundamental landscape appears to be changing as equity markets struggle to bounce back with the same vigour as before. The Fed’s promise to maintain a restrictive stance sees real yields beginning to detract from expensive US stocks, the AI hype-train slows on TSMC demand concerns, and tech stocks show signs of vulnerability to higher rates. WHAT DOES ‘HIGHER FOR LONGER’ MEAN FOR US STOCKS IN Q4? Without actually hiking rates the Fed issued a hawkish message with the assistance of its summary of economic projections. The committee wiped out 50 basis points worth of cuts next year while raising estimates of growth and longer-term inflation. Equity markets appeared to look right past the growth story and focused on the chance of fewer cuts next year, effectively delaying when the first cut is likely to materialise. Raising rates to such restrictive levels and then holding can be likened to doing stomach crunches until you really start to fatigue and then being told to hold at the top. It’s going to be a major challenge! Rising rates have spurred US treasury yields higher. So much so, that the ‘risk-free’ 10-year yield is on the cusp of catching the S&P 500 earnings yield. Should equity values continue to decline into Q4, investors would be tempted to pivot from risky stocks into bonds purely to receive that risk-free yield. Elevated interest rates globally also weighs on US stocks moving forward as foreign revenues are likely to come under pressure. 10-Year US Treasury Yield vs S&P 500 Earnings Yield EQUITY DRIVERS: RISING GDP AND EPS GROWTH The US economy has put in an impressive performance ever since that technical recession in 2H 2022 and shows little sign of petering out and the Fed agrees. An uncharacteristically robust labour market means more people are employed and have discretionary income at their disposal. Of course, higher rates reduce disposable income but there is still a lot of money changing hands within the local economy. Services PMI data also remains in expansion territory but has been edging closer to the all-important 50 mark separating expansion from contraction. US Retail Sales Data (Monthly) Source: Tradingeconomics, Prepared by Richard Snow Additionally, forecasters now see earnings per share (EPS) growth turning positive for the first time since Q3 2021. While earnings per share consistently beat estimates throughout 2023, expectations had been moving lower as rate hikes flew higher. Now, in the first two months of Q3 analysts collectively reported higher expected EPS growth into year end. S&P 500 CY 2023 & CY 2024 Source: Factset, Prepared by Richard Snow SEASONALITY SIDES WITH BULLS BUT Q4 BRINGS GREATER UNCERTIANTY From a seasonal perspective, US stocks (using the S&P 500 as a proxy here) tend to rise over Q4 but something to look out for is the increased variation in returns over the near 23-year period analysed. The observed standard deviation in October and November is higher than that witnessed in other periods. S&P 500 Monthly Returns (1 Jan 2010 – Sep 2023) Seasonality Heatmap Source: Refinitiv, Prepared by Richard Snow https://www.dailyfx.com/news/equities-q4-fundamental-outlook-fed-rate-outlook-to-weigh-on-stocks-20231001.html