2023-09-25 04:27

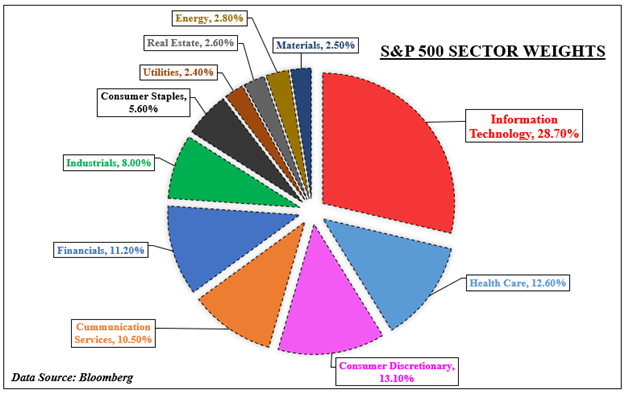

S&P 500, VIX INDEX, STOCK SECTOR DIVERSIFICATION, MACRO - TALKING POINTS The S&P 500 has 11 sectors to choose from to diversify stock portfolios Broadening exposure is not always perfect at avoiding market volatility What levels of VIX undermine this strategy and what can traders do? WHAT IS STOCK SECTOR DIVERSIFICATION? If an investor wants to diversify exposure in the US stock market, there are plenty of sectors to choose from in the S&P 500. On the pie chart below, there are 11 to pick that range from growth-oriented information technology to value-centered industrial firms. To hedge against sector-specific risks, a trader could spread out their portfolio between some combination of these. In such a case, if the S&P 500 hits a bump, losses in one corner of the market might be offset or be reduced by gains in another. This might work if all the sectors in the market are not falling in unison. However, when almost every corner of the index is declining in a binary move, a stock diversification strategy becomes increasingly unreliable. This is not a case against a stock diversification strategy. Rather, this is analyzing conditions in the market that impact sectors moving together in the S&P 500. This is performed using the CBOE Volatility Index (VIX), also known as the market’s preferred ‘fear gauge’. With that in mind, what levels of VIX should traders and investors watch that risk undermining a stock diversification strategy? S&P 500 SECTOR BREAKDOWN WHAT IS THE VIX AND WHY SHOULD TRADERS WATCH IT? The VIX was created in 1990 to use as a benchmark for analyzing volatility projections in the US stock market. It trades in real-time, reflecting expectations of the price movement over the next 30 days. As such, it tends to have a very close inverse relationship with the S&P 500. In other words, as stocks fall, the VIX rises and vice versa. For a deeper dive into the VIX, check out a complete guide here. This inverse relationship can be seen in the next chart, which shows the average S&P 500 performance compared to equivalent VIX levels since 2002. For the study, average weekly data is used to calculate monthly outcomes. This is done so that it helps avoid truncating the ‘volatility of volatility’, whereas a monthly reading could run into the data failing to capture the broader trend. Looking at the data, April tended to see the most optimistic performance for the S&P 500, averaging 2.06%. Afterwards, this performance tapered before bottoming in October, when the benchmark stock index returned about -0.1%. During this period, we saw the VIX climb, starting at 18.30 in April, then rising to 21.23 in October. Knowing this, we can now look at what happens within the S&P 500. VIX VERSUS THE S&P 500 S&P 500 CROSS-SECTOR CORRELATIONS WITH THE VIX To see when a stock sector diversification strategy can fail, we will need dedicated price indices of the 11 sectors in the S&P 500. The data used for the latter only goes back to 2002. We can then find correlation levels between the VIX and for each sector using a one-month rolling basis. The correlations range between -1 and 1. A -1 reading means perfect inverse movements between two variables, while 1 is perfect unison. Averaging all 11 outcomes in each period offers a cross-sector correlation reading with the VIX. Next, the correlations are separated into groups ranging from strong (-1 to -0.75), medium (-0.75 and -0.50), and weak (all values greater than -0.5). A strong inverse reading reflects the VIX rising/falling as sectors dropped/climbed together with the most consistency. Weak ones represent sectors moving more freely. In 7 out of 12 months, higher levels of VIX were associated with stronger cross-sector inverse correlations with the ‘fear gauge’. For example, the average weekly price of the VIX in March was 26.55 when the S&P sectors moved the most in unison. The price dropped to 15.28 when we saw sectors move more freely. Knowing this, what levels of VIX can undermine a cross-sector diversification strategy? VIX PRICE VERSUS DIFFERENT LEVELS OF S&P CROSS-SECTOR INVERSE CORRELATIONS WHEN CAN A STOCK SECTOR DIVERSIFICATION STRATEGY FAIL? We can now average the prices of the VIX for all months and years since 2002 based on the 3 correlation groupings. Simultaneously, we will average the weekly performance of all the S&P sectors and align them based on the same categories. On the chart below, we can see that the outcome was fairly predictable. Stronger inverse correlations with the VIX aligned with increasingly worse performance between sectors. When we saw all the sectors move the most opposite to the VIX, the average price of the ‘fear gauge’ was 22.85. When this occurred, the average return of each sector was -0.47%. Conversely, when the sectors moved more freely relative to the VIX, the price of the latter was 16.72. At that price, the average return between each sector was +1.08%. It should be noted that correlation does not imply causation. Just because the VIX is at some arbitrary price does not mean that it is the sole cause of trading dynamics between sectors. Rather, it is being used here as a frame of reference. What actually causes markets to fall in binary moves is a combination of fundamental factors: monetary policy, fiscal spending, company guidance and more. WHAT CAN TRADERS DO ABOUT VOLATILITY? Knowing this information, what can traders do when expecting high volatility and strong cross-correlations across market sectors? High bursts of volatility are often short-lived and temporary. During these times, haven-oriented assets tend to outperform. This includes the US Dollar, which often rises during times of global market stress. Short-selling stocks is another. Scaling back exposure on current and new undertakings also help. Combining these could help prepare traders for some bumpy roads. VIX PRICE VERSUS PERFORMANCE OF S&P 500 SECTORS BASED ON CORRELATION GROUPINGS https://www.dailyfx.com/forex/fundamental/article/special_report/2022/07/04/When-Can-SP-500-Volatility-Break-a-Stock-Diversification-Strategy-Analyzing-the-VIX.html

2023-09-25 04:25

Major US indices attempted to bounce off their respective near-term support last Friday, but gains failed to sustain into the latter half of the session as selling pressures dominate. This came as the Federal Reserve’s (Fed) recent hawkish hold remains the overarching theme for the risk environment, which was further followed up by hawkish Fed officials’ comments to end the week. More notably, Governor Michelle Bowman, a Fed’s voting member, downplayed recent inflation progress and called for the need for additional rate hikes. US Treasury yields remain elevated near their 16-year high, despite some cooling on Friday. That kept a lid on gold prices, which have been struggling to overcome a key resistance confluence at the US$1,945 level, where its 100-day moving average (MA) stands alongside its Ichimoku cloud on the daily chart. The formation of a near-term ascending triangle may still reflect buyers attempting to take back some control lately, but the US$1,900 level may have to see some defending ahead. Failure to do so may potentially open the door to retest the US$1,850 level next. Source: IG charts Asia Open Asian stocks look set for a subdued open, with Nikkei +0.13%, ASX -0.54% and KOSPI +0.02% at the time of writing. Despite the downbeat showing in Wall Street, Chinese equities have been resilient, with some dip-buying near key technical support. The Hang Seng Index was up 2.6% last Friday, after retesting its August 2023 low, while the Nasdaq Golden Dragon China Index was also up 2.9% - a divergence in performance from the US session. Profit-taking in outperforming markets, such as in US equities, may drive some potential rotation of capital into Chinese equities for now, where conditions have been far more undervalued while hopes are in place that recent positive economic surprise are reflecting early signs of policy success. Singapore’s August inflation data will be on watch today. The core pricing pressures are expected to moderate for the fourth straight month to 3.5% from previous 3.8%, while headline inflation could soften to 4% from previous 4.1% as well. Alongside the recent decision from the Fed to keep rates on hold, these factors may allow the Monetary Authority of Singapore (MAS) to further extend its pause on monetary policy tightening at its October meeting, while keeping watch on ongoing economic risks. To recall, Singapore’s non-oil exports have fallen for an 11th straight month in August as a reflection of soft global demand. The USD/SGD has delivered a new nine-month high lately on US dollar strength, with the pair overcoming a key resistance at the 1.360 level, which marked the upper edge of a long-ranging pattern since the start of the year. Near-term lower highs on its RSI on the daily chart may point to some exhaustion for now, but the broader upward trend may stay intact as long as the 1.360 level holds. Any success in overcoming its recent tops at the 1.367 level may pave the way for further upside to retest the 1.380 level next. Source: IG charts On the watchlist: Dovish takeaway from Bank of Japan (BoJ) meeting keeps USD/JPY at its 10-month high Comments from the BoJ Governor on Friday have served as a pushback to recent hawkish bets, with patience in policy normalisation being the key takeaway from the BoJ meeting. Uncertainty over the economic outlook and wanting to see more on the ‘sustainable 2% inflation’ condition for a policy pivot are factors highlighted for more wait-and-see, at least for now, although rate expectations continue to price for an end to its negative interest rates in 1Q 2024. The USD/JPY has held firm at its 10-month high, as the Fed-BoJ policy divergence was reinforced. While the lower highs on the daily Relative Strength Index (RSI) may still point to some near-term exhaustion, the prevailing trend for USD/JPY remains upward-bias, with an ascending channel pattern in place since the start of the year. Further upside may leave the 150.00 level as a key resistance to overcome while on the downside, the 145.80 level will be an immediate support to defend for the bulls. Friday: DJIA -0.31%; S&P 500 -0.23%; Nasdaq -0.09%, DAX -0.09%, FTSE +0.07%. https://www.dailyfx.com/news/asia-day-ahead-risk-mood-remains-cautious-usd-sgd-at-nine-month-high-20230925.html

.png)

2023-09-22 06:39

JAPANESE YEN - USD/JPY OUTLOOK Bank of Japan’s decision on Friday will steal the limelight. BoJ is expected to stand pat on monetary policy, but could subtly signal that a change in strategy in looming on the horizon. This article looks at key USD/JPY levels to watch in the coming days The Bank of Japan will announce its September decision on Friday following the Fed’s verdict on Wednesday. The institution, led by Kazuo Ueda, is largely expected to stand pat on monetary policy, holding its key interest rate steady at -0.10% and keeping its yield curve control program unchanged. In terms of forward guidance, the BoJ is likely to maintain its characteristic dovish tone, but may slowly start laying the groundwork for an exit from its ultra-accommodative stance to prevent market disruptions and minimize surprises when the actual policy shift begins to unfold. Governor Ueda recently indicated that sufficient data on consumer prices may be available by the end of the year to make a decision on possible increases in borrowing costs. These comments suggest that there is a growing inclination among policymakers to consider moving away from negative interest rates. With headline inflation running above the 2% target for more than a year, excessive yen devaluation and oil prices on a tear, it wouldn’t be surprising to see a less dovish central bank. While ‘less dovish’ does not equal ‘hawkish’, it would still be a departure from the old status quo. Any subtle change in the overall message that signals the central bank is finally starting to consider the possibility of adopting a less accommodative posture could be bullish for the Japanese yen, creating the right conditions for a brief rally against the U.S. dollar. In the event of a USD/JPY pullback, the reversal could be of temporary nature, as multi-year highs in U.S. Treasury yields, particularly those on the long end of the curve, will continue to support the greenback's attractiveness in the FX market for the foreseeable future. USD/JPY TECHNICAL ANALYSIS USD/JPY fell towards 146.00 early last week, but found support and quickly rebounded, rising towards channel resistance near 148.00 in recent days. Despite its constructive bias, the pair has been unable to clear the 148.00 barrier decisively, with the bulls being repeatedly rebuffed in this region. After latest rejection, sellers have gained some impetus, pushing the exchange rate towards 147.50 at the time of writing. If the pullback deepens in the coming sessions, initial support is seen at 145.90, followed by 144.55. On further weakness, the crosshairs will be fixed on 143.85. On the flip side, if market momentum shifts in favor of buyers again, the first technical ceiling to watch is located around 148.00. Upside clearance of this resistance could reinforce upside pressure, opening the door for a move towards 148.80 and 150.00 thereafter. USD/JPY TECHNICAL CHART USD/JPY Chart Prepared Using TradingView https://www.dailyfx.com/news/forex-japanese-yen-forecast-bank-of-japan-may-rock-the-boat-for-usd-jpy-how-20230921.html

.png)

2023-09-22 06:38

GOLD, RETAIL TRADER POSITIONING, TECHNICAL ANALYSIS – IGCS UPDATE Gold prices extend losses in the aftermath of the Fed Retail traders are increasing their upside exposure This is a sign of more pain to come from XAU/USD Gold prices fell about -0.6 percent over the past 24 hours as financial markets continued digesting the aftermath and implications of the Federal Reserve interest rate decision. In response, retail traders have increased bullish exposure in the precious metal. This can be seen by looking at IG Client Sentiment (IGCS), which often functions as a contrarian indicator. Gold Sentiment Outlook - Bearish The IGCS gauge shows that about 74% of retail traders are net-long gold. Since most are biased to the upside, this things that prices may continue falling down the road. Meanwhile, upside bets have increased by 8.02% and 5.9% compared to yesterday and last week, respectively. With that in mind, the combination of overall positioning and recent changes produces a stronger bearish contrarian trading bias. XAU/USD Daily Chart On the daily chart, recent losses have continued pushing gold lower towards rising support from February. At the same time, near-term falling resistance from July is offering a downside trajectory. As the two trendlines converge, this brings prospects of a breakout increasingly sooner. Key support is the rising trendline, as well as the 38.2% Fibonacci retracement level of 1903.46. Breaking lower would open the door to an increasingly bearish bias, placing the focus on the August low of 1884.89. Otherwise, a turn higher and breakout through the falling trendline exposes the 23.6% Fibonacci retracement level of 1971.63. That would offer a shift to an increasingly bullish technical outlook. Chart Created in Trading View https://www.dailyfx.com/analysis/gold-price-extend-losses-in-the-aftermath-of-the-fed-xau-usd-upside-bets-grow-20230921.html

.png)

2023-09-22 06:37

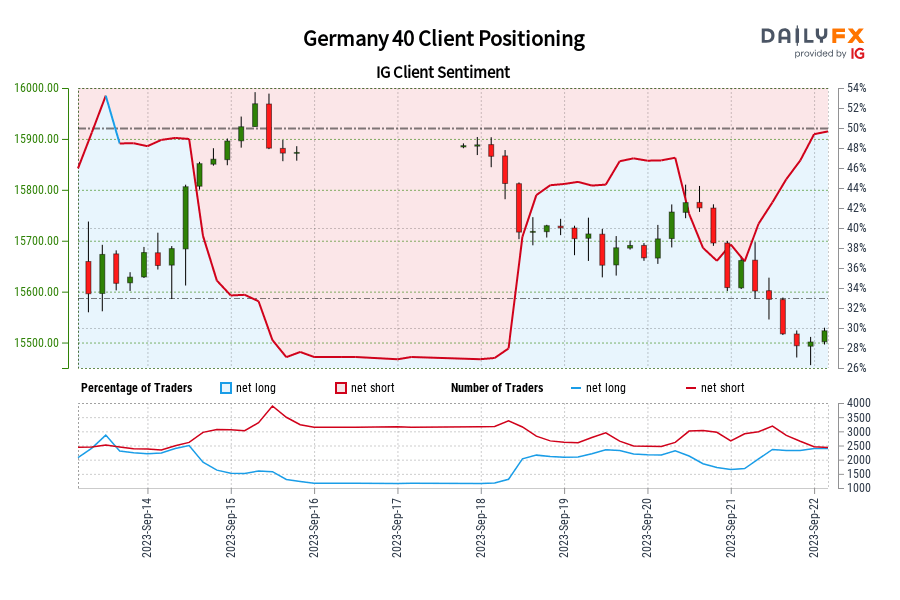

NUMBER OF TRADERS NET-SHORT HAS DECREASED BY 20.26% FROM LAST WEEK. Germany 40: Retail trader data shows 50.07% of traders are net-long with the ratio of traders long to short at 1.00 to 1. In fact, traders have remained net-long since Sep 14 when Germany 40 traded near 15,860.10, price has moved 2.12% lower since then. The number of traders net-long is 40.72% higher than yesterday and 60.80% higher from last week, while the number of traders net-short is 16.90% lower than yesterday and 20.26% lower from last week. We typically take a contrarian view to crowd sentiment, and the fact traders are net-long suggests Germany 40 prices may continue to fall. Our data shows traders are now net-long Germany 40 for the first time since Sep 14, 2023 11:00 GMT when Germany 40 traded near 15,860.10. Traders are further net-long than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger Germany 40-bearish contrarian trading bias. https://www.dailyfx.com/analysis/DE30-IG-Client-Sentiment-202309220523.html

2023-09-22 06:35

UNDERSTANDING AUSTRALIAN DOLLAR FUNDAMENTAL BIAS – EDUCATIONAL REPORT: The Australian Dollar is influenced by sentiment, commodity prices and monetary policy From 2011 - 2023, RBA vs Fed policy became a poorer predictor of AUD/USD direction More focus was placed on financial market sentiment heading into the global pandemic The surge in Australia’s trade balance post-Covid made commodities a key AUD driver Like other exchange rates, AUD/USD can be influenced by the difference in relative monetary policy, which in this case is between the RBA and the Fed. But that alone is one of the many ingredients that drive the direction of the Aussie. Financial markets are constantly adapting to changing economic environments. That also means the importance of what impacts the Australian Dollar changes over time. For example, another ingredient that influences AUD/USD is financial market sentiment. That is because Australia finds itself sitting at the front end of the global supply chain, or in other words, the world business cycle. That is why you will often see the exchange rate being influenced by stock markets, especially those related to Emerging Markets. China is Australia’s largest trading partner, and the latter heavily exports commodities to the former. That also means that understanding the dynamics of commodity prices is another factor that determines Australian Dollar direction. This means three vital ingredients are impacting the exchange rate: relative monetary policy, market sentiment and commodity prices. With that in mind, this is a special report that focuses on trying to understand how the influence of these variables on the Australian Dollar changed from 2006 up until the middle of 2023. The purpose of the study will be to demonstrate why it is important to adapt fundamental analysis to constantly changing environments. With that in mind, let us cover how this was performed. How the Study Was Conducted Rolling regression modeling over a 36-month window in steps was used on the following variables (all of which were expressed in month-over-month form): AUD/USD, the spread between Australian and United States 2-year government bond yields, the MSCI Emerging Markets Index (EEM) and the Bloomberg Commodities Index (BCOM). Doing this created explanatory coefficients that changed in influence over time. It should also be noted that to gauge underlying relationships, a few data outliers were removed. If you are interested, a full analysis of how this was performed was outlined in a Twitter thread. How Has RBA & Fed Policy Divergence Been Influencing AUD/USD? We will start with the importance of relative monetary policy. The dark red line on the chart below is the rolling bond yield spread coefficient and how it changed over time. When this line is rising above 0, that means a 1 percentage point improvement in 2-year bond yield returns in Australia relative to the United States produced an increasingly more positive reaction from AUD/USD (m/m), controlling for EEM and BCOM. In other words, increasingly higher interest rates in Australia relative to the United States typically means stronger Aussie appreciation. What you may notice is that the dark red line has been falling steadily since 2011 and turned slightly negative around the time of 2020. When the dark red line is at 0, that means there is practically no relationship between AU-US bond yield spreads and AUD/USD. So, what happened to this relationship? The yield advantage that Australia once had relative to the United States slowly evaporated after the 2008 Financial Crisis (light red line), turning negative heading into Covid and remaining mostly thereafter. In other words, interest rates in the US became higher than in Australia. As this happened, the ability of RBA monetary policy to influence AUD/USD (through setting interest rates) weakened significantly and remained so in the few years after Covid. How Has Emerging Market Sentiment Been Impacting AUD/USD? While RBA policy became an increasingly poorer predictor of AUD/USD, Emerging Market sentiment became more important. The dark green line on the chart below is the rolling EEM coefficient. When this line is rising above 0, a 1 percentage point boost in monthly Emerging Market performance shows increasingly better returns in AUD/USD (m/m), controlling for bond yield spreads and BCOM. I have overlaid this with G4 central bank balance sheet assets. What you can see is that as major central banks injected liquidity into the financial system after the 2008 recession, sentiment became an increasingly better predictor of the Aussie exchange rate. But, you might notice that the dark green line peaked just before Covid and stayed lower thereafter despite the surge in asset holdings. That would speak to less influence from market sentiment driving AUD/USD in the post-Covid era (although the relationship remained positive). Let us take a closer look at why this happened. What About Commodity Prices? The dark blue line on the chart below is the rolling BCOM coefficient, zoomed in on just 2016+. When this line is rising increasingly above 0, a 1 percentage point boost in the BCOM Index tends to elicit a stronger positive effect on AUD/USD (m/m), controlling for bond yield spreads and EEM. What is very interesting is that the dark blue line surged higher heading into Covid and remained elevated thereafter. This is as Australia’s trade balance exploded during Covid, meaning the value of the nation’s exports became significantly larger than its imports. In other words, as commodity prices surged, benefiting Australia, AUD/USD paid more attention to the BCOM Index and less so to EEM and AU-US bond yield spreads. A Closer Look at Post-Covid The last chart below plots the EEM and BCOM coefficients zoomed in on 2016+. The reason this was performed is to visualize the evolution of AUD/USD underlying fundamental dynamics during Covid. Specifically, you can see how entering the pandemic, commodities became a more important factor than Emerging Market sentiment for driving the Aussie exchange rate. This was likely due to the significance of how global trading and surging prices impacted Australia’s economy, and thus the exchange rate. Conclusion and Study Limitations While it is generally correct that monetary policy is a key driver of exchange rates, the truth is each currency behaves differently because of the unique traits of various economies. For the Australian Dollar, sentiment and commodity prices are other key factors that are involved in this equation. On top of this, fundamental conditions change, and the influence of certain variables is no different. What this study has demonstrated is that for the Australian Dollar, RBA policy direction became an increasingly poorer predictor of the exchange rate in the aftermath of the 2008 financial crisis. Instead, factors like market sentiment and commodity prices become better predictors of the exchange rate as underlying fundamental conditions evolved heading into Covid. Perhaps this could reverse course in the future, such as in a scenario where interest rates in Australia begin far outpacing those in the US. It should be noted that this kind of modeling with rolling regressions creates many outputs, 180 to be exact in this sample. That is 180 different regressions that could each have their quirks or issues, such as creating a coefficient that is not statistically significant. This was not considered. Instead, a general comprehensive regression of the entire dataset was thoroughly analyzed for potential issues. This included testing for correlation between control variables, residual normality, residual autocorrelation and heteroskedasticity. No major faults were identified. https://www.dailyfx.com/news/australian-dollar-fundamental-bias-breakdown-what-matters-the-most-for-aud-usd-20230611.html

.png)