2023-09-11 06:44

The US Dollar absolutely crushed it against its major counterparts this past week. In fact, the Euro confirmed its 8th weekly loss against the Greenback, matching an identical losing streak back in 2014. A 9th disappointment would mean the longest monthly losing streak since 1997! But, the Chinese Yuan took the cake in terms of being one of the worst performers. Financial market sentiment also deteriorated, with the Nasdaq Composite, S&P 500 and Dow Jones weakening -1.95%, -1.11% and -0.42% last week, respectively. Things were not looking much better across the Atlantic, with the DAX 40 and Euro Stoxx 50 falling -0.63% and -1.06%, respectively. Japan’s Nikkei 225 weakened -0.32% while Australia’s ASX 200 sank -1.67%. A key contributor to the cautious pessimism likely stemmed from the US Treasury market. The 10-year yield gained 2.08%, bringing medium-term rates closer to the August high following a dip a few weeks ago. There is a slew of event risk in the coming week. On Wednesday, all eyes turn to the next US inflation report. A mixed bag could lay ahead for the Federal Reserve. While core inflation is seen weakening to 4.3% y/y from 4.7% in July, the headline rate is estimated to rise from 3.2% to 3.6%, likely owing to the rise in crude oil prices of late. Outside of the United States, the week starts off with United Kingdom employment data for British Pound traders, followed by GDP figures later. Meanwhile, AUD/USD will be tuning in for Australian employment data on Thursday. Then, EUR/USD will be eyeing the next ECB rate decision. What else is in store for markets in the week ahead? How Markets Performed – Week of 9/4 Forecasts: British Pound Forecast: GBP/USD, EUR/GBP Face Heavyweight Risk Events After a quiet few days for data and events, next week the calendar has a few high importance releases that will shift British Pound pairs. Australian Dollar Forecast: New Lows Question the Outlook for AUD/USD and AUD/JPY The Australian Dollar is struggling to get off the matt with rates on hold and the global economic outlook under question. Treasury yields are rising again, lifting the US Dollar. USD/JPY Price Forecast: Yen Ready to Take on USD According to Japanese Officials USD/JPY is approaching intervention territory as the pair heads towards the 150 mark. Upcoming US CPI is likely to provide short-term directional guidance this week. Euro Forecast: ECB to Save EUR/USD Slide? EUR/GBP in Neutral Zone An outside chance of a hike from the ECB presents an opportunity to halt EUR/USD selloff. UK GDP and jobs data could reinforce Governor Bailey’s terminal rate reference Crude Oil Early September Rally Sets the Stage for Another Monthly Gain? After an early jump, crude oil prices are on course for a 4th monthly. While bearish reversal signals brew, the broader trend remains firmly bullish. What are key levels to watch next? Gold/Silver Forecast: Real Yields to Drive XAU/USD, XAG/USD Precious metals are in search of some positive catalysts, and the sector is looking to US real yields for some reprieve. What is the outlook and what are the key levels to watch in gold and silver? US Dollar Forecast: How Will US Inflation Data Impact Yields and USD? The upcoming August U.S. inflation report will play a crucial role in shaping financial markets, determining the trajectory of Treasury yields and the U.S. dollar in the near term. https://www.dailyfx.com/news/markets-week-ahead-euro-ecb-us-dollar-gold-treasuries-us-cpi-aud-usd-jobs-data-20230910.html

.png)

2023-09-11 06:41

Japanese Yen, USD/JPY, US Dollar, BoJ, Ueda, Intervention, JGB, Yields, - Talking Points USD/JPY recoiled lower on Monday after remarks from BoJ Governor Ueda The BoJ might be prepping the market for policy adjustments further down the track The yield spread between JGBs and Treasuries might be worth watching The Japanese Yen has had a wild start to the week after comments from Bank of Japan Governor (BoJ) Kazuo Ueda opened the door to speculation for the end of its negative interest rate policy (NIRP). In early Asian trade on Monday morning, USD/JPY retreated from its 10-month peak of 147.87. It traded down to 146.67 before steadying back over 147. It has since dipped below 146.40. Live prices can seen on the right-hand side of this article. The Yomiuri Shimbun newspaper is reporting that Ueda san may tilt monetary policy if wages and prices rise, citing that there are various options. He made it clear that any policy adjustment will be dependent on circumstance by saying, “We have a variety of options if economic and price conditions turn upward.” However, the market might have got ahead of itself in seeking tightening from the BoJ. Ueda also remarked, “There is still some way to go before the price target can be realized. We will continue our persistent monetary easing policy.” The BoJ has a policy rate of -0.10% and is maintaining yield curve control (YCC) by targeting a band of +/- 0.50% around zero for Japanese Government Bonds (JGBs) out to 10 years. The bank has become flexible on YCC implementation, recently allowing the 10-year Japanese Government Bond (JGB) to yield above 0.50%. It traded at 0.70% today, its highest return in almost 10 years. The spread between JGBs and Treasury yields might be worth paying attention to as there has traditionally been a strong correlation to USD/JPY. The next few sessions may see some volatility in this part of the market. USD/JPY AND YIELD SPREAD BETWEEN 10-YEAR TREASURIES AND JGBS Chart created in TradingView Governor Ueda’s comments follow some soft jawboning last week from Masato Kanda, Japan’s Vice Minister of Finance for International Affairs and BoJ board member Hajime Takata. It might be reasonable to expect more remarks from Japanese officials if USD/JPY makes another move to the topside. The market is generally not anticipating physical intervention until the price moves toward 152.00, if at all. The November 2022 high was 151.95. To learn more about how to trade USD/JPY, click on the banner below. USD/JPY TECHNICAL ANALYSIS SNAPSHOT USD/JPY made a 10-month high last Tuesday before consolidating. A breakout on either side of the range could see momentum evolve in that direction. If a bullish run emerges, resistance might be at the prior peaks of 148.85 and 151.95. On the downside, support may lie at the breakpoints in the 145.05 – 145.10 area ahead of the prior lows near 144.50 and 141.50. The 34-day Simple Moving Average (SMA) is also near 144.80 and may lend support. https://www.dailyfx.com/news/japanese-yen-rallies-on-bank-of-japan-s-ueda-comments-will-usd-jpy-reverse-20230911.html

.png)

2023-09-11 06:39

Major US indices attempted to stabilise towards the end of last week (DJIA +0.22%; S&P 500 +0.14%; Nasdaq +0.09%), but gains remained feeble following recent de-risking in tech and concerns of a resurgence in inflationary pressures. Thus far, Wall Street’s performance has been in line with the weak seasonality pattern for September, but several support lines may still have to give way before there are greater conviction that the broader upward trend is reversing. For now, the VIX has struggled to move higher, seemingly placing its sight back at its year-to-date low. For the S&P 500, the index continues to trade within its Ichimoku cloud pattern on the daily chart, with buyers successfully defended it back in mid-August this year. Further downside may leave the 4,400 level on watch as support to hold, while sentiments could likely stay cautious to start the new week amid the Fed blackout period and lead-up to the US Consumer Price Index (CPI) – the last piece of key inflation data to anchor rate expectations before the next Federal Open Market Committee (FOMC) meeting. Market expectations have been firmly priced for the Fed to keep rates on hold at the September meeting, but the central bank’s guidance for policymaking to be on a meeting-by-meeting basis still leaves the November meeting wavered. This may likely be in line with the Fed’s previous guidance of having one last rate hike by the end of this year before heading into a prolonged pause. Source: IG charts Asia Open Asian stocks look set for a downbeat open, with Nikkei -0.37%, ASX -0.29% and KOSPI -0.12% at the time of writing. The key story for markets to digest may revolve around the weekend remarks from Bank of Japan (BoJ) Governor Kazuo Ueda, with him guiding that the central bank may have enough wages data by year-end to decide on its ultra-loose monetary policies. With the option for an end to negative interest rates on the table, it is perceived to lay the groundwork for further policy normalisation ahead, although the Governor is also quick to downplay some speculations by indicating patience. The slightly hawkish takeaway from his comments brought the Japan’s 10-year yields to another new high since 2014, narrowing the yield differential with the US which has been a key driving force for the USD/JPY. That said, with the next BoJ meeting scheduled to be less than two weeks away, there may still be room for disappointment for near-term hawkish bets, given that the Governor’s comments seem to place any rate decision only in 2024, along with the less likelihood of back-to-back policy tweaks given its broadly patient stance. The 145.80 level may be a key support level on watch for the USD/JPY, which marked the upper bound of previous yen-buying intervention back in September 2022. Declining moving average convergence/divergence (MACD) and lower highs on relative strength index (RSI) may suggest ebbing upward momentum for now, but the broader upward trend may remain intact until several support lines are broken, with the 145.80 level serving as an immediate support to hold. Source: IG charts On the watchlist: US dollar on watch ahead of US CPI data this week Thus far, US Treasury yields have stayed firm in the lead-up to the US CPI release this week, pricing for rates to be kept high for longer with ongoing expectations for a resurgence in US headline inflation (est 3.6% vs previous 3.2%). That have kept the US dollar near its six-month high, following a 5.6% rebound since mid-July this year. While the US dollar continues to trade above its key 200-day moving average (MA), a potential bearish divergence in the making on the daily RSI may point to some near-term indecision with ebbing upward momentum. Ahead, the 105.00 level will be a crucial resistance to overcome, which marks the upper bound of a long-ranging pattern since the start of the year. Failing to cross the level may leave the 103.12 level on watch as immediate support. Source: IG charts https://www.dailyfx.com/news/asia-day-ahead-cautious-mood-ahead-of-us-cpi-jpy-on-watch-amid-boj-s-ueda-comments-20230911.html

.png)

2023-09-11 06:38

AUSTRALIAN DOLLAR VS US DOLLAR, EURO, BRITISH POUND – PRICE SETUPS: AUD/USD is attempting to form a temporary base. The consolidation/correction in EUR/AUD and GBP/AUD may not be over yet. What is the outlook and the key levels to watch in select AUD crosses? AUD/USD: Growing odds of a minor rebound After an initial attempt to break higher in late August, AUD/USD is back around its August lows. However, a new/minor high created at the end of last month raises the prospect of AUD/USD retesting the 200-period moving average on the 240-minute charts (now at about 0.6500). AUD/USD 240-Minute Chart Chart Created by Manish Jaradi Using TradingView Zooming out, in recent weeks, AUD/USD has been attempting to hold above quite strong support on a downtrend line from the end of 2022. Any break above the August 30 low of 0.6525 could indicate the start of a material consolidation. That’s because, on higher timeframe charts, including the weekly charts, AUD/USD is looking oversold and is showing tentative signs of fatigue. For more discussion, including fundamentals, see “Australian Dollar Looks to Recoup Losses Ahead of CPI; AUD/USD, AUD/NZD, AUD/JPY,” published August 29. EUR/AUD 240-Minute Chart Chart Created by Manish Jaradi Using TradingView EUR/AUD: Consolidation within a broadly bullish phase The failure of EUR/AUD to resume its uptrend last week could be a sign that the consolidation that started last month isn’t over. EUR/AUD retreated from near a tough hurdle at the end-August highs of around 1.6880, coinciding with the upper edge of the Ichimoku cloud on the 240-minute charts.The cross is now testing a vital floor area: the 200-period moving average, slightly above a horizontal trendline since August (at about 1.6635). Any break below 1.6635 could raise the odds of further losses, initially toward 1.6450. GBP/AUD 240-Minute Chart Chart Created by Manish Jaradi Using TradingView GBP/AUD: Testing a crucial cushion GBP/AUD is testing a crucial converged cushion: the 200-period moving average, coinciding with a horizontal trendline from the end of August (at about 1.9450), not too far from an uptrend line from June. A hold above the support area is key for the uptrend to resume. To be sure, a break below isn’t imminent, but any break below would point to an extended consolidation with a slightly weak bias. On the upside, GBP/AUD would need to break above last week’s high of 1.9750 for the bullish bias to resume. https://www.dailyfx.com/analysis/australian-dollar-could-rebound-a-bit-aud-usd-eur-aud-gbp-aud-price-setups-20230911.html

.png)

2023-09-11 06:36

US Dollar, DXY Index, USD/JPY, Ueda, BoJ, USD/CNH, China, India, Commodities - Talking Points US Dollar is under pressure as BoJ Governor's Comments Shake Currency Markets Government bond yields are higher globally with JGBs leading the way The ascending trend remains in play for the DXY index for now. Will it reverse? The US Dollar has taken a battering across the board to start Monday with the DXY (USD) index giving up a large portion of last week’s gains. The Japanese Yen scored the largest gains in the aftermath of comments by the Bank of Japan (BoJ) Governor. In an interview with the Yomiuri Shimbun newspaper, Governor Kazuo Ueda said, “We have a variety of options if economic and price conditions turn upward.” However, he clarified that “There is still some way to go before the price target can be realized. We will continue our persistent monetary easing policy.” USD/JPY initially traded near the recent peak of 147.87 at the open before collapsing toward 146.00 throughout the Asian session. 10-year Japanese Government Bond yields traded above 0.70% today for the first time since early 2014. Elsewhere, the G-20 summit concluded in India, with a joint communique that has been viewed as a positive for India, indicating a possible shift in global geo-political and economic dynamics. China's credit data exceeded expectations, leading to a dip in the USD/CNH (US Dollar/Chinese Yuan) after the fix. New Yuan loans were CNY 1.36 billion in August, above forecasts of CNY 1.25 billion. This news could be a positive signal for traders, as a healthier credit environment in China can potentially lead to increased economic activity and investment opportunities. The growth linked Aussie and Kiwi Dollars notched sizable gains, as did Sterling do a lesser extent. APAC equity indices are mixed with Australia’s ASX 200 and mainland China’s CSI 300 seeing small gains while Hong Kong’s Hang Seng index dipped. In Japan, bank shares experienced noticeable gains with the prospect of higher interest rates. The Nikkei 500 banking index rose by over 3%, while the broader Nikkei 225 index fell by approximately 0.5%. This divergence highlights the potential for sector-specific trading strategies, as different industries can react differently to the same macroeconomic indicators. In commodities markets, iron ore futures traded higher on the Dalian and Singaporean exchanges. Gold and silver have seen small gains on the weaker USD. Crude oil is mostly steady with the West Texas Intermediate (WTI) futures contract slipping slightly toward US$ 87 while the Brent contract is trading near Friday’s close just above US$ 90.50. Looking ahead, the highlight this week will be the US Consumer Price Index (CPI) data release on Wednesday. This key economic indicator can significantly influence the Federal Reserve's monetary policy, and thus impact the USD and other correlated assets. DXY (USD) INDEX TECHNICAL ANALYSIS SNAPSHOT The DXY Index broke below a breakpoint near 104.70 and that level may offer resistance ahead of another breakpoint and prior peak in the 105.10 – 105.15 area. The index remains in an ascending trend channel and support might be found at the breakpoints near 104.45 and 103.57 or further below at the previous lows in the 102.90 – 103.00 area. https://www.dailyfx.com/news/us-dollar-on-the-ropes-with-yen-leading-the-way-aud-nzd-and-gbp-piled-in-20230911.html

.png)

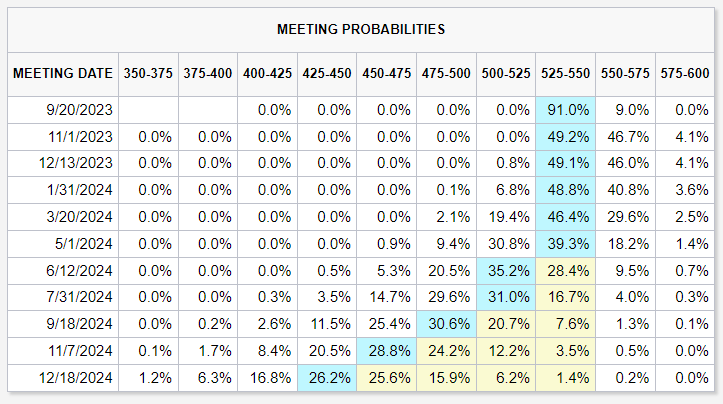

2023-09-07 03:41

EUR/USD ANALYSIS EUR/USD retreated on Wednesday, falling to a three-month low around the 1.0700 handle, as strong U.S. economic data increased the probability of additional FOMC policy firming in 2023, reinforced the case for a restrictive monetary policy position for an extended period and propelled U.S. Treasury yields upwards, with the 2-year yield comfortably breaking above the 5.0% threshold. Focusing on catalysts, the ISM non-manufacturing PMI showed that the U.S. services sector grew strongly in August, rising to 54.5 versus the expected 52.5, reaching its highest mark since February, a sign that the U.S. economy remains remarkably resilient and that sturdy demand pressures may prevent inflation from slowing materially towards the 2.0% target in the coming months. Although the Fed has pledged to “proceed carefully”, upside surprises in macroeconomic indicators could prompt policymakers to reevaluate their “cautious” approach, potentially nudging them towards contemplating additional hikes in 2023 or, at the very least, fully committing to a "higher-for-longer" strategy. This scenario could weigh on EUR/USD, especially if the Eurozone economy weakens further. FOMC INTEREST RATE EXPECTATIONS Source: CME FedWatch Tool https://www.dailyfx.com/news/forex-euro-forecast-eur-usd-on-bearish-path-on-us-exceptionalism-key-levels-ahead-20230906.html