2023-08-25 06:16

USD/ZAR PRICE, ANALYSIS AND CHARTS: USD/ZAR Rises Despite BRICS Expansion Plans, Dollar Bulls Return. BRICS Bloc Has Extended an Invitation to 6 Countries to Join the Bloc with Saudi Arabia the Surprise. The BRICS Bloc Has Bold Ambitions but a Lot of Work Lies Ahead to Bring the Vision to Reality. The First Steps are Definitely Positive for the Bloc as it Looks to Challenge the Established Global Order. The South African Rand (ZAR) has been enjoying an excellent run of late thanks to a combination of factors. That run has come in for a slight reprieve today as the USD regained some momentum with USDZAR up 1.24% on the day and back above the 18.50 mark. BRICS SUMMIT AND EXPANSION PLANS The BRICS Summit finally kicked into serious mode today with the BLOC confirming it has extended invitations to 6 countries while leaving the door open to further expansion. Among the countries mooted for the Blocs first expansion include Iran, Argentina, Ethiopia, Egypt, UAE and of course the big name in Saudi Arabia. What is intriguing about the announcement is the historically close ties between Saudi Arabia and Egypt with the powers that be in Washington DC, and how any decision to join BRICS may affect the relationship dynamics between the nations. GDP (at Current Prices) of the Expanded BRICS Bloc Source:Twitter South African President Cyril Ramaphosa stated that the Bloc has embarked on a new chapter in an effort to build a world that is fair, just and inclusive and prosperous. South Africa remains the smallest economy in the current BRICS make-up and with powerful countries set to join it will be interesting to see if the Southern African Nation loses any clout in the Bloc, a fear first brought up by Brazil. Both countries today however seemed to be looking forward to the expansion with both Brazilian President Lula and SA counterpart Ramaphosa stating that this is the first phase of the expansion with others likely to follow. In response to the invite Ethiopian Prime Minister Abiy Ahmed called the decision ‘a great moment’ while UAE President Mohammed bin Zayed said he appreciated the inclusion of his country. Also in attendance today was the United Nations Secretary-General Antonio Guterres who echoed a recurring plea by BRICS for reforms of institutions like the U.N. Security Council, the International Monetary Fund and World Bank, stating that global governance structures "reflect yesterday's world". Indian Prime Minister Narendra Modi said the expansion and modernization of BRICS is a message that all institutions in the world need to mold themselves according to changing times. Despite all the positivity around the announcement there was fierce debate around the size and speed of the expansion among members and it will be interesting to gauge the groups dynamics moving forward. The inclusion of Saudi Arabia in particular is likely to accelerate talk of de-dollarisation. As mentioned above the Kingdom had been mooted as a possible member but the geopolitical implications as well as its relationship with the West made the prospect even more intriguing. The move will now spark debate about the use of local currencies for trade among the Bloc specifically when it comes to crude oil. The addition of Saudi Arabia, Iran and UAE would see the group make up almost 42% of the global crude oil output. However as mentioned previously de-dollarisation is a complex topic given the makeup of global markets. Saudi Arabia may be viewed as the key given the Kingdoms position in global oil trade. Despite discussions with India and China about accepting payment in Rupees and Yuan the Saudis have thus far remained stubborn which may have something to do with the Saudi Riyal being pegged to the US Dollar. Interesting times ahead indeed but the expansion does certainly pave the way for more serious talk around de-dollarisation. The task of accomplishing that, however, is another story altogether and would require time, willpower, diplomacy and the willingness of the BRICS Bloc to put the Group first at times if it wishes to achieve de-dollarisation. JACKSON HOLE AND US DOLLAR RISK As the BRICS summit comes to a close all eyes are now on the Jackson Hole Symposium which will play host to Central Bankers from the G7 in Wyoming, United States. Last year the symposium focused on the growing challenge of inflation and the impact saw volatility and fireworks across markets, something Central Bankers would like to avoid this time around. The reason I say this is given the recent uncertainty around China and further downgrade to US Banks by S&P Global earlier this week coupled with dire set of PMI data from Europe and the US we could see a more cautious and pragmatic approach from Central Banks. The US Dollar continues to surprise at the minute supported by the rise in US yields as well as some safe haven demand thanks to ongoing uncertainty. Following a bout of weakness yesterday the Dollar Index resumed its advance today with USDZAR rebounding following a brief stint below the 18.50 handle. Any comments from Central Bankers at Jackson Hole have the potential to cause a ripple effect in markets with volatility to be expected heading into the weekend. FINAL THOUGHTS AND TECHNICAL OUTLOOK USDZAR from a technical standpoint has always fascinated me as we tend to trend for a sustained period of time. Looking back historically and trends seem to run for 3-4 months at a time before we see a significant change in the overall trend of the pair. This is something which has continued this year with the upside rally beginning on February 2 from the lows around the 16.9200 mark all the way to the 19.9200 mark on June 1. Looking ahead and the drop this week toward support around the 18.50 handle was met with significant buying pressure with USDZAR up around 1.78% at the time of writing, trading at 18.77. Support was provided by a combination of the 50 and 100-day MA with immediate resistance on the upside around the 19.00 handle. Fed Chair Jerome Powell is expected to deliver remarks at Jackson Hole tomorrow and that could have an impact on the immediate direction of USDZAR. However, given signs of economic improvement and a lower inflation rate, any sign that the US could be done on their hiking cycle could help facilitate another leg to the downside for USDZAR. As seen with many asset classes of late fundamental factors are playing a key role and I expect USDZAR to be no different. USD/ZAR Daily Chart, August 24, 2023 https://www.dailyfx.com/news/forex-usd-zar-forecast-rand-zar-slides-despite-brics-expansion-plans-a-temporary-blip-20230824.html

.png)

2023-08-25 06:12

UNDERSTANDING AUSTRALIAN DOLLAR FUNDAMENTAL BIAS – EDUCATIONAL REPORT: The Australian Dollar is influenced by sentiment, commodity prices and monetary policy From 2011 - 2023, RBA vs Fed policy became a poorer predictor of AUD/USD direction More focus was placed on financial market sentiment heading into the global pandemic The surge in Australia’s trade balance post-Covid made commodities a key AUD driver Like other exchange rates, AUD/USD can be influenced by the difference in relative monetary policy, which in this case is between the RBA and the Fed. But that alone is one of the many ingredients that drive the direction of the Aussie. Financial markets are constantly adapting to changing economic environments. That also means the importance of what impacts the Australian Dollar changes over time. For example, another ingredient that influences AUD/USD is financial market sentiment. That is because Australia finds itself sitting at the front end of the global supply chain, or in other words, the world business cycle. That is why you will often see the exchange rate being influenced by stock markets, especially those related to Emerging Markets. China is Australia’s largest trading partner, and the latter heavily exports commodities to the former. That also means that understanding the dynamics of commodity prices is another factor that determines Australian Dollar direction. This means three vital ingredients are impacting the exchange rate: relative monetary policy, market sentiment and commodity prices. With that in mind, this is a special report that focuses on trying to understand how the influence of these variables on the Australian Dollar changed from 2006 up until the middle of 2023. The purpose of the study will be to demonstrate why it is important to adapt fundamental analysis to constantly changing environments. With that in mind, let us cover how this was performed. How the Study Was Conducted Rolling regression modeling over a 36-month window in steps was used on the following variables (all of which were expressed in month-over-month form): AUD/USD, the spread between Australian and United States 2-year government bond yields, the MSCI Emerging Markets Index (EEM) and the Bloomberg Commodities Index (BCOM). Doing this created explanatory coefficients that changed in influence over time. It should also be noted that to gauge underlying relationships, a few data outliers were removed. If you are interested, a full analysis of how this was performed was outlined in a Twitter thread. How Has RBA & Fed Policy Divergence Been Influencing AUD/USD? We will start with the importance of relative monetary policy. The dark red line on the chart below is the rolling bond yield spread coefficient and how it changed over time. When this line is rising above 0, that means a 1 percentage point improvement in 2-year bond yield returns in Australia relative to the United States produced an increasingly more positive reaction from AUD/USD (m/m), controlling for EEM and BCOM. In other words, increasingly higher interest rates in Australia relative to the United States typically means stronger Aussie appreciation. What you may notice is that the dark red line has been falling steadily since 2011 and turned slightly negative around the time of 2020. When the dark red line is at 0, that means there is practically no relationship between AU-US bond yield spreads and AUD/USD. So, what happened to this relationship? The yield advantage that Australia once had relative to the United States slowly evaporated after the 2008 Financial Crisis (light red line), turning negative heading into Covid and remaining mostly thereafter. In other words, interest rates in the US became higher than in Australia. As this happened, the ability of RBA monetary policy to influence AUD/USD (through setting interest rates) weakened significantly and remained so in the few years after Covid. How Has Emerging Market Sentiment Been Impacting AUD/USD? While RBA policy became an increasingly poorer predictor of AUD/USD, Emerging Market sentiment became more important. The dark green line on the chart below is the rolling EEM coefficient. When this line is rising above 0, a 1 percentage point boost in monthly Emerging Market performance shows increasingly better returns in AUD/USD (m/m), controlling for bond yield spreads and BCOM. I have overlaid this with G4 central bank balance sheet assets. What you can see is that as major central banks injected liquidity into the financial system after the 2008 recession, sentiment became an increasingly better predictor of the Aussie exchange rate. But, you might notice that the dark green line peaked just before Covid and stayed lower thereafter despite the surge in asset holdings. That would speak to less influence from market sentiment driving AUD/USD in the post-Covid era (although the relationship remained positive). Let us take a closer look at why this happened. What About Commodity Prices? The dark blue line on the chart below is the rolling BCOM coefficient, zoomed in on just 2016+. When this line is rising increasingly above 0, a 1 percentage point boost in the BCOM Index tends to elicit a stronger positive effect on AUD/USD (m/m), controlling for bond yield spreads and EEM. What is very interesting is that the dark blue line surged higher heading into Covid and remained elevated thereafter. This is as Australia’s trade balance exploded during Covid, meaning the value of the nation’s exports became significantly larger than its imports. In other words, as commodity prices surged, benefiting Australia, AUD/USD paid more attention to the BCOM Index and less so to EEM and AU-US bond yield spreads. A Closer Look at Post-Covid The last chart below plots the EEM and BCOM coefficients zoomed in on 2016+. The reason this was performed is to visualize the evolution of AUD/USD underlying fundamental dynamics during Covid. Specifically, you can see how entering the pandemic, commodities became a more important factor than Emerging Market sentiment for driving the Aussie exchange rate. This was likely due to the significance of how global trading and surging prices impacted Australia’s economy, and thus the exchange rate. Conclusion and Study Limitations While it is generally correct that monetary policy is a key driver of exchange rates, the truth is each currency behaves differently because of the unique traits of various economies. For the Australian Dollar, sentiment and commodity prices are other key factors that are involved in this equation. On top of this, fundamental conditions change, and the influence of certain variables is no different. What this study has demonstrated is that for the Australian Dollar, RBA policy direction became an increasingly poorer predictor of the exchange rate in the aftermath of the 2008 financial crisis. Instead, factors like market sentiment and commodity prices become better predictors of the exchange rate as underlying fundamental conditions evolved heading into Covid. Perhaps this could reverse course in the future, such as in a scenario where interest rates in Australia begin far outpacing those in the US. It should be noted that this kind of modeling with rolling regressions creates many outputs, 180 to be exact in this sample. That is 180 different regressions that could each have their quirks or issues, such as creating a coefficient that is not statistically significant. This was not considered. Instead, a general comprehensive regression of the entire dataset was thoroughly analyzed for potential issues. This included testing for correlation between control variables, residual normality, residual autocorrelation and heteroskedasticity. No major faults were identified. https://www.dailyfx.com/news/australian-dollar-fundamental-bias-breakdown-what-matters-the-most-for-aud-usd-20230611.html

.png)

2023-08-25 06:11

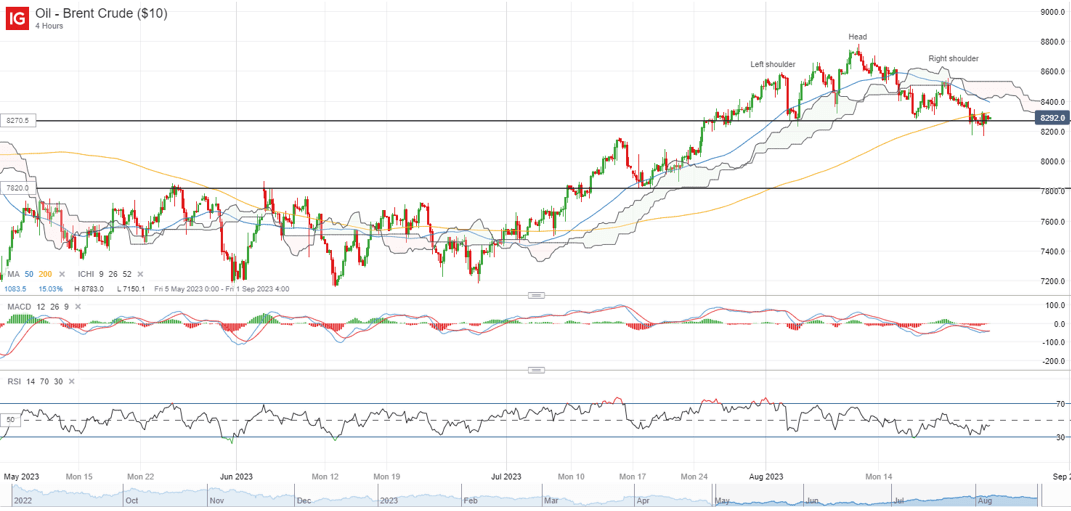

MARKET RECAP Initial gains in Wall Street reversed sharply overnight, with Nvidia’s stellar results hit with a sell-the-news market reaction, as market participants de-risk ahead of Fed Chair Jerome Powell’s Jackson Hole speech later tonight. The VIX was up 7.6% as a reflection of increased hedging activities, while market sentiments (from the CNN Fear and Greed Index) have fallen back into ‘fear’ territory for the first time since March this year. No doubt the Fed’s policy outlook will be the key driving force for markets ahead. With fresh updates on US inflation and labour market data after the previous FOMC meeting, focus will be on what factors the Fed Chair will have his attention on. Maintaining his emphasis on the Fed’s data-dependent stance and bringing up progress in US inflation may potentially be perceived as a less hawkish view, but on the other hand, highlighting the risks of a reacceleration in demand and the need for high-for-longer rates will likely be a more hawkish message. For now, expectations remain firmly priced for rates to be kept on hold in September, but the probability for a November hike has increased to the current 41%, from 32% just a month ago. Treasury yields firmed overnight, following an earlier sell-off on Wednesday, while the US dollar is back at its two-month high, as some positioning for a hawkish takeaway gets underway. Perhaps one to watch may be Brent crude prices, which saw dip buyers attempting to defend the neckline of a head-and-shoulder formation (four-hour chart), with the formation of a series of long-legged pin bars overnight. Greater conviction may have to come from a move back above its shoulders at the 85.40 level, where the upper edge of its Ichimoku cloud resistance (four-hour) may have to be overcome as well. On the other hand, price projection from any breakdown of the head-and-shoulder neckline at the 82.70 level could leave the 78.20 level on watch next. Source: IG charts ASIA OPEN Asian stocks look set for a negative open, with Nikkei -1.55%, ASX -1.05% and KOSPI -0.81% at the time of writing. The rush for market participants to further de-risk ahead of Fed Chair Jerome Powell’s comments has spilled over to the Asia session, given that the previous Fed minutes did not reflect the level of unity among policymakers for a rate pause as what many have expected. The Nasdaq Golden Dragon China Index is down 0.7% overnight, which may challenge the rebound in Chinese equities from oversold technical levels in the earlier session. The formation of lower highs and lows in the Hang Seng Index year-to-date, along with its weekly RSI failing to sustain above the 50 level for the third time this year may still call for more wait-and-see. On the economic calendar, this morning saw the release of Tokyo’s August Consumer Price Index (CPI) data, with moderating headline inflation (2.9% versus previous 3.2%) but a further uptick in the ‘core-core’ aspect (2.6% versus previous 2.5%) providing a mixed view overall. That did not trigger too much of a reaction in the USD/JPY, with the pair taking its lead from US dollar strength on mounting hawkish Fed views. Aside, the AUD/JPY seems to be trading on a near-term descending triangle, with the formation of lower highs and the triangle base around the 93.00 level. Arguably, the recent retracement to a 38.2% Fibonacci level from its March 2023 bottom to June 2023 peak may also leave some hopes on a broader bullish pennant formation. The 93.00 level may be an immediate support level to hold, failing which could pave the way to retest the 91.80 level next, where strong dip-buying off a 50% Fibonacci retracement level was sighted on 28 July 2023. On the upside, the downward trendline resistance will be a key line to overcome, with greater conviction probably having to come from a move back above the 95.34 level. Source: IG charts On the watchlist: 200-day MA for EUR/USD in the crosshair Strength in the US dollar overnight has kept the EUR/USD under pressure, with the pair pushing to a new two-month low and leaving its 200-day MA under threat of a breakdown. Its weekly RSI is also back to retest the key 50 level for the third time this year, with any failure to defend the MA-line over the coming days likely to leave sellers in greater control. For now, the 1.080 level seems like an immediate key support to hold. Any subsequent move below the 1.080 level may potentially pave the way towards the 1.063 level next, which will also mark the first time where the pair trades below its 200-day MA since November 2022. https://www.dailyfx.com/news/de-risking-ahead-of-fed-chair-s-jackson-hole-speech-brent-crude-aud-jpy-eur-usd-20230825.html

2023-08-24 09:24

NZD/USD, AUD/NZD, GBP/NZD - OUTLOOK: China cut its 1-year benchmark lending rate but left is 5-year rate unchanged. NZD gave up early gains, with NZD/USD testing key support. What is the outlook for NZD/USD, GBP/NZD, and AUD/NZD? The New Zealand dollar gave up early gains against its peers after China cut its one-year benchmark lending rate but left its five-year rate unchanged. The one-year benchmark lending rate was cut by 10 basis points, while the five-year rate was left unchanged, contrary to expectations for 15 basis-point cuts to both. Over the weekend, China pledged to coordinate financial support to resolve local government debt problems. Local government finances have worsened due to the prolonged weakness in the property sector, causing a credit crunch for a number of developers. Last week, China unexpectedly lowered key policy rates for the second time in three months in a bid to revive the faltering post-Covid economic recovery, rising deflation risks, and tightening credit conditions. NZD/USD Daily Chart Beijing has announced a series of measures in recent months to cushion some of the downside risks to the economy, including cuts in key lending benchmarks, targeted measures toward the property sector aimed at the supply side, and signaled the end of the years-long crackdown on the technology sector. Many are awaiting additional measures for the struggling property sector addressing the demand side and infrastructure. China is New Zealand’s largest trading partner, and any improvement in China’s growth prospects bodes well for NZD. NZD has been underperforming against some of its amid deteriorating NZ economic growth outlook for the current year and the belief that NZ interest rates have peaked. Last week, the Reserve Bank of New Zealand (RBNZ) kept its cash rate steady, as expected, but slightly pushed out when it expects to start cutting interest rates to 2025. NZD/USD: At the lower edge of the support On technical charts, NZD/USD looks oversold as it tests support on a downtrend line from March, slightly above the bottom end of a downtrend channel from the beginning of the year. There is no sign of reversal yet, and NZD/USD would need to rise above the end-June low of 0.6050 for the immediate downward pressure to ease. GBP/NZD Monthly Chart GBP/NZD: Testing a tough barrier GBP/NZD is testing a key converged hurdle at 2.10-2.20, including the 200-month moving average, coinciding with a downtrend line from 2007, and the 2020 high of 2.18. This resistance is very important, and a decisive break above could clear the path toward the 2015 high of 2.46. AUD/NZD Weekly Chart AUD/NZD: Well within the range AUD/NZD continues to trade sideways, but well within the lower edge of a rising pitchfork channel from last year. The broader range established is 1.05-1.11, but most recently the range has narrowed to 1.07-1.09. A break above 1.11 or a break below 1.05 is needed for AUD/NZD to start trending. https://www.dailyfx.com/news/new-zealand-dollar-reverses-gains-after-pboc-move-nzd-usd-aud-nzd-gbp-nzd-setups-20230821.html

.png)

2023-08-21 09:04

Euro, EUR/USD, US Dollar, Fed, Jackson Hole, China, PBOC, HSI, Crude Oil, Gold - Talking Points Euro support has held so far but may falter if the US Dollar resumes strengthening China eased monetary policy today, but not by enough looking at the price response Markets are now eyeing the Fed’s Jackson Hole symposium. If they’re hawkish, will EUR/USD break lower? The Euro steadied to start the week as it pauses in its recent run lower on the back of the US Dollar regaining its ascendency this month. Most of the other major currency pairs have also had a slow Monday so far. The Federal Reserve meeting minutes for the July gathering opened the door to a potential hike in the target rate going into the end of the year. Later this week the Kansas City Fed will host its annual Jackson Hole Economic Symposium. For the near term, the market will be looking for clues on the September Federal Open Market Committee (FOMC) rate decision. The podium at this event also lends itself for notable adjustments in the bigger picture for the Fed. As a result, Fed Chair Jerome Powell’s speech will be closely watched by the market this Friday. The People’s Bank of China (PBOC) eased monetary policy today by 15 basis points (bp) for the 1- and 5-year loan prime rate. They ended up moving the 1-rate by only 10 bp to 3.45% and kept the 5-year rate unchanged at 4.20%. Earlier today the People’s Bank of China (PBOC) eases monetary policy, moving the 1-year loan prime rate by only 10 basis points to 3.45% and kept the 5-year rate unchanged at 4.20%. The market had been anticipating a 15 bp cut for both instruments. Hong Kong’s Hang Seng Index (HSI) plunged on the news, trading more than 1.8% at one stage. Other APAC equity indices are generally, except for Japan, that saw modest gains. Crude oil has found firming footing with the WTI futures contract is nearing US$ 82 bbl while the Brent contract is a touch above US$ 85 bbl. Spot gold remains below US$ 1,900 and has been oscillating around US$ 1,890 today. Looking ahead, the US will see some existing home sales adata and a number of Fed speakers will be crossing the wires. EUR/USD DAILY TECHNICAL ANALYSIS SNAPSHOT EUR/USD remains below a descending trend line but has stalled in its bearish run just above a potential support zone in the 1.0830 – 1.0835 area where there are some breakpoints and prior lows. Support could also be near the 78.6% Fibonacci Retracement levels at 1.0770 which is just above the 200-day simple moving averages (SMA). Ahead of that level, some prior lows and the breakpoint in the 10830- 1.0835 area may provide support. If EUR/USD was to rally and approach the descending trend line, there could be resistance at the 21- and 55-day SMAs just ahead of it. Potential resistance might also be offered in the 1.1065 – 1.1095 area where several historical breakpoints reside along with a recent high and just ahead of the psychological level at 1.1100. Further up, resistance could be at the breakpoint from the March 2022 high at 1.1185 or the recent peak at 1.1275, which coincides with two historical breakpoints. Above those levels, resistance might be at the Fibonacci Extension of the move from 1.1095 to 1.0635 at 1.1380. Just above there are some more breakpoints in the 1.1385 – 95 area. https://www.dailyfx.com/news/euro-steadies-as-hang-seng-tanks-on-pboc-s-shallow-cut-lower-eur-usd-20230821.html

.png)

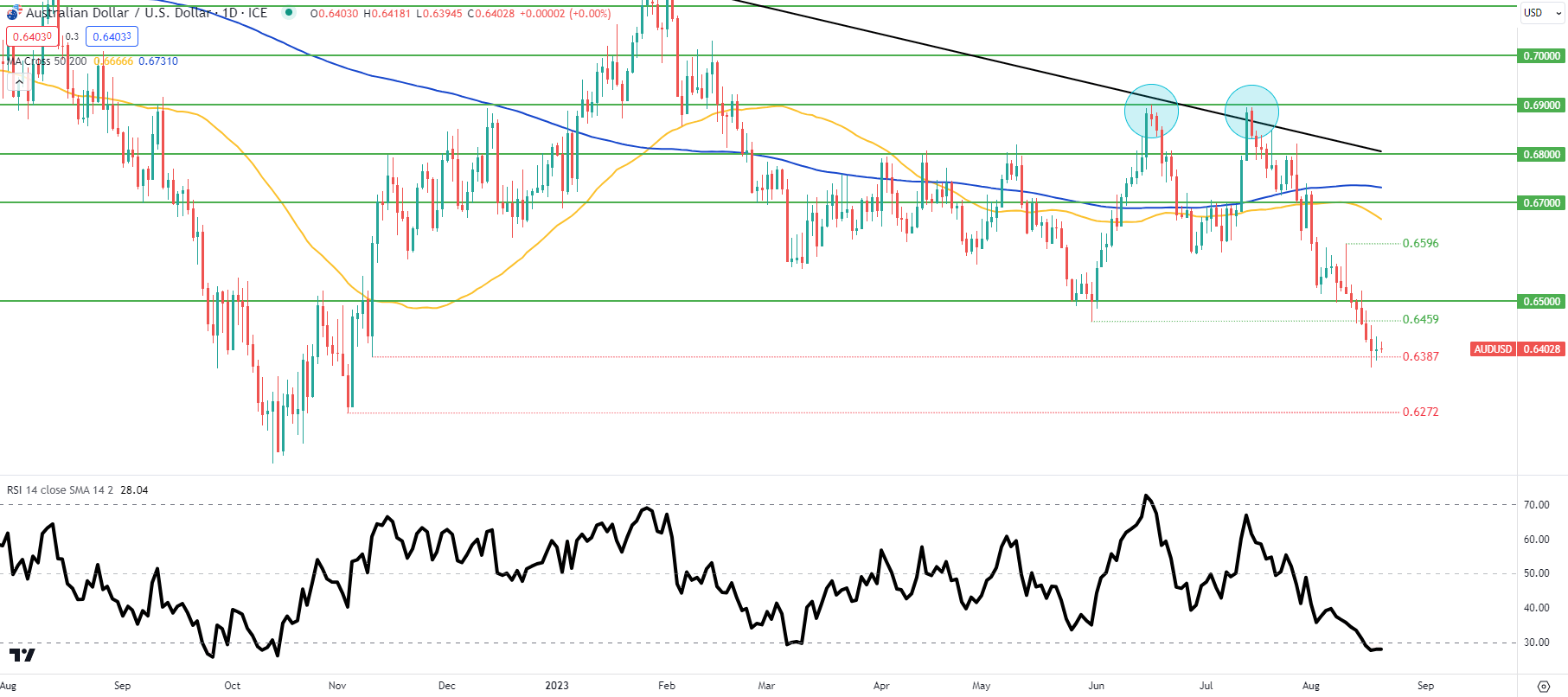

2023-08-21 09:03

AUD/USD ANALYSIS & TALKING POINTS Lack of Chinese stimulus weighs on Aussie dollar. RBA’s higher for longer > Federal Reserve. Turnaround or continuation for AUD/USD? AUSTRALIAN DOLLAR FUNDAMENTAL BACKDROP The Australian dollar is trading at extreme levels this Monday as the PBoC decided to modestly reduce interest rates (see economic calendar below) on the 1-year LPR while keeping the 5-year rate on hold. This unexpected outcome resulted in the pro-growth AUD weaker against the US dollar despite the DXY marginally lower for the day. Pricing today across FX markets are relatively subdued with investor uncertainty increasing due to key upcoming risk events including the BRICS summer and Jackson Hole Economic Symposium. With Jackson Hole being the focal point as Fed Chair Jerome Powell could alter the current ‘higher for longer’ narrative, potentially providing some support for the fading Aussie dollar. AUD/USD ECONOMIC CALENDAR (GMT +02:00) Source: DailyFX economic calendar Looking at money market pricing for the Reserve Bank of Australia (RBA) below, expectations for a rate cut does not look to be priced in for 2023 or 2024 unlike the Fed who is forecasted to cut around May of 2024. Should Fed Chair Jerome Powell push a more accommodative stance this week, this interest rate differential may further augment any AUD upside. TECHNICAL ANALYSIS AUD/USD DAILY CHART Chart prepared by Warren Venketas, TradingView Daily AUD/USD price action continues to hover around the 0.6387 swing support and a daily confirmation candle close could spark another leg lower towards the November 2022 low at 0.6272. That being said, the Relative Strength Index (RSI) is now in oversold territory and could indicate a possible end to the recent downtrend although moving against the prevailing trend carries a high degree of risk. Investors may want to wait for the fundamental drivers to take place before entering the market as Jackson Hole traditionally carries significant price swings. Trader hesitancy has already commenced with the latest slew of doji candlesticks that could point to a pause before a resumption of the downtrend or a shift. Key resistance levels: 0.6596 0.6500 0.6495 Key support levels: 0.6387 0.6272 IG CLIENT SENTIMENT DATA: BULLISH (AUD/USD) IGCS shows retail traders are currently net LONG on AUD/USD, with 81% of traders currently holding long positions. Download the latest sentiment guide (below) to see how daily and weekly positional changes affect AUD/USD sentiment and outlook. https://www.dailyfx.com/news/forex-aud-price-forecast-no-respite-for-aussie-after-reserved-china-rate-cut-wv-20230821.html