2023-08-16 08:54

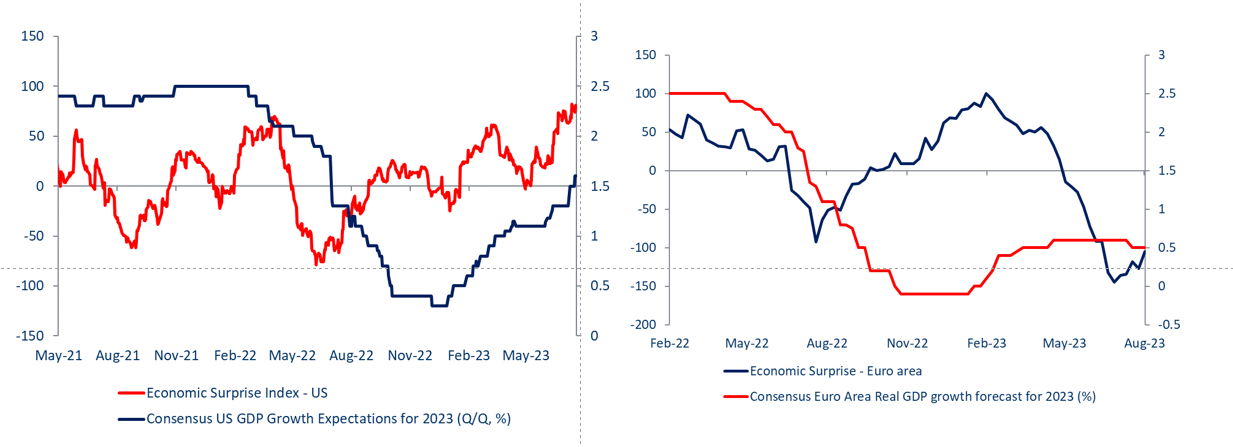

Euro Vs US Dollar, Australian Dollar, British Pound – Outlook: EUR/USD is nearing key support ahead of Euro area GDP and FOMC minutes. EUR/AUD is attempting to break above a vital ceiling; EUR/GBP is off highs. What is the outlook and the key levels to watch in key Euro crosses? The euro is testing key levels against some of its peers ahead of the release of Euro area GDP data (due later today) and the FOMC minutes (due Thursday). The Euro area economic growth likely slowed to 0.6% on-year in the April-June quarter from 1.1% in the previous quarter on tightened credit conditions as the effect of aggressive ECB rate hikes spills over. The underwhelming macro data is reflected in the Euro area Economic Surprise Index (ESI), which is just off 3-year lows. Economic Surprise Index – Euro Area and US While the unexpected improvement in German investor morale in August is positive, the economic growth outlook needs to reverse for a sustained rebound in EUR, especially against the US. Against other currencies, EUR has been largely resilient, reflecting stable ECB rate expectations until mid-2024. EUR/USD 240-Minutes Chart The US ESI is hovering around the highest level since early 2021. In addition, consensus has upgraded its US economic assessment for the current year. A data-dependent Fed is likely to keep the optimistic 2024 rate cut expectations in check. In this regard, the focus is on minutes of the June FOMC meeting due on Thursday, especially given a resilient US economy, a tight labour market, and market expectations that Fed rates may have peaked. EUR/USD Monthly Chart EUR/USD: Approaching a vital cushion On technical charts, EUR/USD is now approaching a fairly strong cushion zone, including the July low of 1.0830, the 200-day moving average, and the 89-day moving average. This follows a failed attempt to rise above the July 31 high of 1.1045 – a risk pointed out in the previous update. See “Euro Lifted Slightly by US Downgrade, but Will it Last? EUR/USD, EUR/AUD, EUR/NZD Price Action,” published August 2. EUR/USD Daily Chart Any break below could open the door toward the 1.0500-1.0600 area, including the early-2023 lows. This support area needs to hold for the broader uptrend to persist. On the upside, a break above last week’s high of 1.1065 is needed for the immediate weakness to fade. EUR/AUD Weekly Chart EUR/AUD: Attempting to break higher EUR/AUD is attempting to break above crucial resistance on a horizontal trendline from 2020, at about 1.6800. Any break above could open the way toward 1.7700 (the 61.8% retracement of the 2020-2022 slide). From a medium-term perspective, the trend is up given the higher-top-higher-bottom sequence since late 2022, as highlighted in the previous update. EUR/GBP Daily Chart EUR/GBP: Upside capped EUR/GBP continues to be weighed by a stiff converged hurdle, including the 200-day moving average, a downtrend line from early 2023, around the July high of 0.8700. Beyond any short-term sideways price action, the overall bias remains toward the downside while the resistance holds. https://www.dailyfx.com/news/euro-ahead-of-euro-area-gdp-fomc-minutes-eur-usd-eur-aud-eur-gbp-price-setups-20230816.html

2023-08-15 02:36

Wall Street managed to start the week higher (DJIA +0.07%; S&P 500 +0.57%; Nasdaq +1.05%), tapping on some recovery in big tech and semiconductors to override earlier jitters around China’s property and financial sector risks. There was not much to note on the economic calendar overnight, with the relief potentially attributed to the positive view on Nvidia from Morgan Stanley, along with some attempt to stabilise after recent sell-off. US Treasury yields continue its way higher, with the 10-year yields back at its year-to-date high around the 4.2% level. The two-year yields edged near its 5% level as well, largely a reflection for US rates to be kept high for longer. The US dollar index tapped on higher yields to gain 0.3%, but are now facing a crucial test of resistance at its 200-day moving average (MA), which it has not overcome since November 2022. Its weekly relative strength index (RSI) is hanging at its key 50 level as well, suggesting that its moves over the coming days may be critical in determining the trend ahead. Perhaps one to watch may also be the Russell 2000 index, which is currently back at its previous horizontal resistance-turned-support at the 1,900 level, in coincidence with the upper edge of its Ichimoku cloud on the daily chart. A long-legged candle denotes some overnight dip-buying, but buyers may potentially find greater conviction from a move in the daily RSI back above its 50 level. For now, the 1,900 level will need to see some defending, failing which may pave the way towards the 1,820 level next. Source: IG charts Asia Open Asian stocks look set for a positive open, with Nikkei +0.70% and ASX +0.38% at the time of writing. South Korean markets are off-trading for Liberation Day. Despite the relief in Wall Street, Chinese equities are more subdued, with the Nasdaq Golden Dragon China Index down 0.5% overnight. Economic releases this morning saw a pull-ahead in Japan’s 2Q GDP (annualised 6% vs 3.1% forecast), the strongest expansion since 4Q 2020. The data is likely to provide the Bank of Japan (BoJ) with more room for normalisation, although the initial short-lived bounce in the Japanese yen seems to reflect some market expectations that patience from the central bank is still the likely stance. Ahead, focus will be on the Reserve Bank of Australia (RBA) minutes. At the previous meeting, the RBA has kept its tightening bias in place for some policy flexibility, so the minutes will be scrutinised on the factors to guide the RBA’s next decision. The China’s monthly economic data dump will be in focus as well. Industrial production is expected to stay unchanged, while retail sales are projected to recover to 4.5% from previous 3.1%. The downside surprises in economic data lately may leave room for disappointment and it may still have to take a trend of recovering economic data to convince markets that the worst is over. The Straits Times Index is attempting to defend its trendline support after unwinding all of its past month’s gains, alongside its 200-day MA at around the 3,245 level. Failure to defend the trendline support with a break below its 3,230 level may potentially support a move to retest its July 2023 bottom at the 3,130 level. On any upside, the 3,260 level will be an immediate resistance to overcome. Source: IG charts On the watchlist: AUD/USD attempting to find support from year-to-date low Ahead of the RBA meeting minutes and China’s economic data today, the AUD/USD is tapping on some relief in the risk environment overnight to hold its year-to-date bottom at the 0.645 level. The formation of a bullish pin bar on the daily chart reflects some near-term dip-buying, although one may watch for a confirmation close to potentially support a move to retest the 0.659 level. Thus far, rate expectations remain firm that the RBA is nearing the end of its hiking cycle but the central bank’s data-dependent stance will still leave eyes on incoming data such as wage growth and inflation for confirmation. For now, while there is an attempt to stabilise after recent sell-off, the broader trend still seems to carry a sideway to downward bias, with the weekly RSI hanging below the 50 level. The year-to-date bottom at the 0.645 level may have to see some defending ahead for some near-term relief. Source: IG charts Friday: DJIA +0.07%; S&P 500 +0.57%; Nasdaq +1.05%, DAX +0.46%, FTSE -0.23% https://www.dailyfx.com/news/market-relief-in-wall-street-amid-china-s-jitters-russell-2000-straits-times-index-aud-usd-20230815.html

.png)

2023-08-15 02:34

S&P 500, NASDAQ ANALYSIS US indices off to a slow start – Tesla down after Chinese vehicle discounts US PPI, Treasury yields and the US dollar weigh on US stocks The analysis in this article makes use of chart patterns and key support and resistance levels. US INDICES OFF TO A SLOW START – TESLA DOWN AFTER CHINA VEHICLE REPRICING Tesla announced it was cutting prices of its popular Model Y offering in the competitive Chinese market for electric vehicles. The move has been prompted by a tricky trading environment, as the Chinese economy faces a number of challenges to the highly anticipated economic rebound. Economic data since Q1 has placed the recovery in doubt. The manufacturing sector continues to contract, exports and imports declined in July and according to the latest inflation report, deflation appears to be setting in. Tesla gapped lower at the start of trading but has attempted to bridge the gap since. The June swing low will be telling as it serves as a tripwire for potential continued selling. Tesla Daily Chart Source: TradingView, prepared by Richard Snow US PPI, TREASURY YIELDS AND THE DOLLAR WEIGH ON US STOCKS Friday’s hotter than expected PPI print resulted in further rising US 10-year yields which supports the US dollar. Such a result typically weighs on indices as rising risk-free rates carry a more attractive yield and, as the name suggest, its as close to risk free as you can get. US 10-year yields approach levels last seen at the end of October – the highest since 2007/2008. A lack of high importance US data this week leaves US indices looking for direction. One thing markets will get clarity on this week is the state of the US consumer, with US retail sales data and earnings updates from Target and Walmart. The S&P 500 recently broke below trendline support – highlighting the potential for an extended pullback. The June 16th high at 4450 appears to have provided a level of support as price action now tests the trendline resistance (former support). The MACD highlights the bearish momentum which remains in play, resulting in renewed interest in trendline resistance. If broken with momentum, 4450 is followed by 4325 on the downside. A move and close above trendline resistance highlights the yearly high of 4607. S&P 500 Daily Chart Source: TradingView, prepared by Richard Snow NASDAQ 100 BREAKS TRENDLINE SUPPORT The Nasdaq (E-Mini Futures) chart reveals a very similar charting posture, although, only on Friday witnessed a break of trendline support. 14,853 is the tripwire for bearish momentum with 14,251 coming into focus thereafter. Tech stocks however, have been resilient in 2023 despite interest rates rising above 5%. As such, the outlook remains in favor of the uptrend. 15,260 is the immediate level of resistance followed by 15,710 and 16,062. Nasdaq 100 Daily Chart (E-Mini Futures) https://www.dailyfx.com/news/s-p-500-nasdaq-update-us-stocks-resilient-despite-tesla-s-china-woes-20230814.html

.png)

2023-08-15 02:32

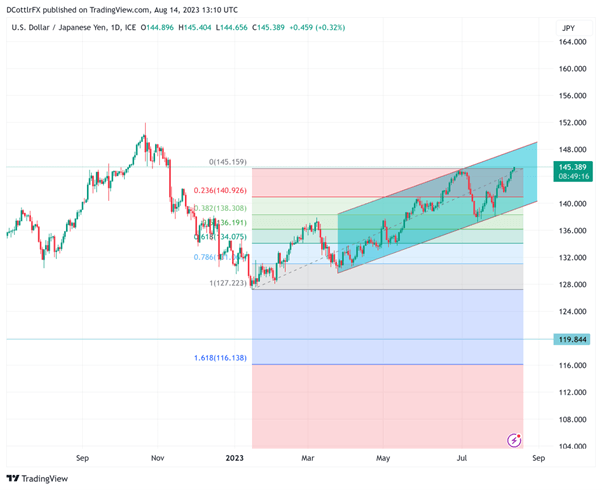

JAPANESE YEN (USD/JPY) ANALYSIS AND CHARTS USD/JPY Posts new 2023 high as risk aversion, yield differentials boost the Dollar Key 145 region now in play The Bank of Japan bought Yen above this point in 2022 The Japanese Yen weakened further against the United States Dollar as a new trading week kicked off on Monday, taking USD/JPY into a region that saw ‘intervention’ action from the Bank of Japan to curb Yen weakness back in 2022. The pair charged back above the psychologically important 145.00 handle, posting a new high for this year of 145.40 in the process. The last time it topped this point was in September 2022, when the Dollar’s rise eventually saw the BoJ stepping in to bring the pair back down, buying Yen directly for the first time since 1998. The market will accordingly be back on intervention watch whenever the pair creeps back above the 145 line, with HSBC reportedly suggesting that BoJ action can be expected in the 145-148 band. Bank of Japan (BoJ) - Foreign Exchange Market Intervention The latest move was part of a general bout of Dollar strength, with the greenback supported by rising Treasury yields and some broad risk aversion. Asian stocks were buffeted by new concerns about the ailing Chinese economy. With demand sluggish and deflation taking hold in the world’s second-largest economy, secondary effects are now being felt. Worries about the debt-laden real estate and construction sectors are nothing new, but on Monday came news that property-development giant Country Garden had suspended trade in eleven of its onshore bonds. This in turn prompted speculation that the company will have to restructure its debts, with its shares falling 16% in Hong Kong. There were also some concerns about Typhoon Lan, which is expected to make landfall in Japan on Tuesday. Air and rail travel is already seeing restrictions. The Bank of Japan offered unlimited Japanese Government Bonds with residual maturities of between five and ten years on Monday, part of its policy of Yield Curve Control. Tuesday will see the release of official Gross Domestic Product numbers out of Japan for the second quarter of this year. A modest increase is expected for the annualized growth rate. That’s tipped to come in at 3.1%, above the 2.7% seen in the first three months. The on-quarter rate is expected to have ticked up to 0.8%. As-expected data would suggest that the economy continues to recover from the Covid pandemic, albeit at a quite modest rate. The BoJ wants to see a durable return of domestic demand before it unwinds its outlying loose monetary policy. USD/JPY TECHNICAL ANALYSIS USD/JPY Daily Chart USD/JPY has seen a renewed bout of strength since late July but this is merely the latest move in a well-respected broad uptrend channel in place since March. Monday’s trade has seen initial resistance at 145.258 topped, but it remains to be seen whether Dollar bulls can hold above that on a daily close basis. If they can, they’ll be looking at more resistance points from November 2023, the last time the pair pushed up this high. The 146.414 region, from which the Dollar slid on November 9 last year now comes in as resistance. There’s likely support at 143.26, Aug 2’s intraday top, and, well below that, there’s initial Fibonacci retracement support at 141, defending channel support at 139. 202. Those last two levels don’t seem in immediate danger but a market wary of central bank intervention will keep them in mind. As Monday’s European session fades out, the Dollar is hovering around the psychologically important 145.50 level. A close above that will probably embolden bulls to try and push on higher, although the broader market may suspect that the Dollar is becoming a little overstretched, at least in the short term. Retail trader data shows 19.91% of traders are net-long with the ratio of traders short to long at 4.02 to 1. https://www.dailyfx.com/news/japanese-yen-jpy-clobbered-to-new-23-lows-skirts-intervention-zone-20230814.html

2023-08-15 02:29

Gold, XAU/USD, US Dollar, China, Yuan, Treasury Yields, DXY Index, GVZ - Talking Points The gold price headwinds persist as Treasury yields push higher, boosting USD The PBOC has adjusted policy as the outlook for China faces challenges Volatility remains low but has inched up slightly. If it goes higher, where to for XAU/USD? The gold price continues to languish going into Tuesday’s trading session as the US Dollar pursues higher ground, assisted by rising Treasury yields. The metals complex is generally weaker across the board, impeded by the stronger Dollar and deteriorating appetite for risk and growth-orientated assets. Industrial metals have been hit harder than the yellow metal with the outlook for China facing increased scrutiny. Generally weaker economic data there last week has been compounded by property groups Country Garden and Ocean Sino missing debt payments. Country Garden defaulted on US Dollar coupon payments last week and this week saw trading in its onshore debt suspended alongside Ocean Sino. The market is awaiting concrete action from authorities to deal with the economic uncertainty. A plethora of Chinese data will be closely inspected for further clues on the state of the world’s second-largest economy. The details can be viewed here. The People’s Bank of China (PBOC) fixed the Yuan stronger today at 7.1768 per USD. The bank also cut the medium-term lending facility rate to 2.50% from 2.65%. While that is unfolding, the benchmark 10-year Treasury note is surging above 4.20% for the first time since November last year after dipping to 4.73% a month ago. The Treasury curve seems more firmly anchored with the market now viewing the Federal Reserve as near the end of its tightening cycle. The 2-year bond is nearing 5.0%, still some way from the peak of 5.11% seen last month. This appears to have underpinned the DXY (USD) index. At the same time, forward-looking gold volatility has been languishing of late, but it has inched up in the last few trading sessions. This may hint toward some uncertainty within the market and a significant move in price might be in the offing. The GVZ index is a measure of implied volatility for gold that is calculated in a similar way to the VIX index’s interpretation of volatility for the S&P 500. Looking ahead, the precious metal has held up reasonably well given the state of play, but if these headwinds persist it could be further undermined. SPOT GOLD AGAINST US 10-YEAR TREASURY YIELD, DXY (USD) INDEX AND GVZ INDEX https://www.dailyfx.com/news/gold-price-loses-its-lustre-as-the-us-dollar-and-treasury-yields-climb-lower-xau-usd-20230815.html

.png)

2023-08-11 03:51

US DOLLAR (DXY) PRICE, CHART, AND ANALYSIS The US dollar sheds half a point after the CPI release. Headline inflation rises by less than expected. Core inflation fell and headline inflation rose by less than expected in July, according to the latest US Inflation Report. Core inflation fell to 4.7% y/y, the lowest level since October 2021, while headline inflation rose from 3% to 3.2% but missed market expectations of 3.3%. Bureau of Labor Statistics Release The marginally better-than-expected report sent the US dollar lower by around 50 pips as further rate hike expectations eased a fraction. EUR/USD touched 1.1065 before retreating back to 1.1035 at the time of writing, while GBP/USD clipped 1.2820 before falling back to 1.2775. Interest-rate sensitive gold rose to $1,930/oz after opening Thursday at $1,914/oz. before slipping back to $1,925/oz. The US dollar (DXY) currently trades at 102.02 after opening the session at 102.489. US DOLLAR (DXY) DAILY PRICE CHART – AUGUST 10, 2023 https://www.dailyfx.com/news/breaking-news-us-dollar-slips-after-inflation-data-miss-forecasts-20230810.html

.png)