2023-08-11 03:50

EUR/USD PRICE, CHART, AND ANALYSIS EUR/USD topped 1.10 After Jul’s US Inflation Data Core CPI’s Deceleration Trend Remains In Place even as headline inflation ticked up Eurozone inflation expectations remain uncomfortably high The Euro popped above its last ten days’ trading range against the United States Dollar in Thursday’s European afternoon as important US inflation data came in broadly as expected, with markets reportedly daring to hope that interest rates might not have to rise again this year in the world’s largest economy. July’s official Consumer Price Index rose by an annualized 3.2%. That was above June’s 3% rise. Food, housing, and automobile insurance costs were largely to blame for the increase. The core measure strips out the volatile effects of food and fuel. It rose by 4.7%. That was a tick below June’s outcome. The rate has been gradually weakening since it peaked at 6.6% back in September 2022. Headline inflation meanwhile peaked at 9.1%. A good session for market forecasters, then, but a rather less good one for Dollar bulls. EUR/USD popped above $1.10 on the news, as markets stick with the view that, while US borrowing costs may have further to rise, they’re not likely to go too much higher in this cycle given clear signs that inflation is coming to heel. Indeed, the Wall Street Journal reported after the data that derivatives markets now predict that the current Fed Funds Target Rate of between 5.2%% and 5.5% is likely to stay put for the rest of this year. Of course, this thesis will be highly data dependent and there’s one more CPI report and another official employment data release between now and the next meeting of Open Market Committee rate-setters on September 20. The Euro has slipped against the greenback since it printed seventeen-month highs in mid-July, but it hasn’t fallen very far despite a rather gloomy outlook for the Eurozone economy. The European Central Bank released its monthly bulletin this week. It was a downbeat roundup that spoke of a deteriorating economic outlook and weaker domestic demand thanks to rising inflation and tight financing conditions. Inflation expectations within the currency bloc remain uncomfortably high, despite the ECB itself hinting that it might be close to the end of its own tightening cycle after nine consecutive increases in borrowing costs. Still, the Euro retains a degree of interest rate support which has seen EUR/USD climb steadily from its lows of last September. The week hasn’t got a lot more to give in terms of tradable economic numbers. Friday’s Yuan-loan data out of China could move EUR/USD given the market focus on China’s stuttering recovery. The University of Michigan’s venerable consumer sentiment snapshot will round out the week. EUR/USD Technical Analysis EUR/USD Daily Chart Compiled Using TradingView EUR/USD has been rangebound since July 26 between 1.0909 and 1.1041. Thursday’s trade has seen the pair probe above that but the break doesn’t at this point look conclusive. Euro bulls will need to retake July 6’s peak of 1.1103 to convince and, perhaps, push on to key resistance at 1.1275, but so far they haven’t had the conviction to do so. Near-term support comes in at 1.0912 and 1.07329, with the latter below trendline support from last November which comes in at 1.07905. Longer-term, the Euro remains well within the impressive uptrend established since last September’s lows and seems likely to retest its recent highs once the present consolidative phase plays out. Sentiment toward the pair is bullish according to IG Group data, although not overly so, and the uncommitted may want to wait and see where the pair closes out the week relative to its current trading range before taking a directional view. https://www.dailyfx.com/news/eur-usd-gains-on-target-us-cpi-has-markets-betting-rates-will-stay-put-20230810.html

2023-08-11 03:43

GOLD, XAU/USD, CPI, TRENDLINE BREAKOUT – PRECIOUS METALS BRIEFING: Gold prices sink in the aftermath of US inflation data Longer-term Treasury yields outpaced the front-end This will continue making life difficult for XAU/USD Gold prices weakened in the aftermath of US inflation data on Thursday, reversing upside progress accumulated during the first 12 hours of the day. Headline CPI clocked in at 3.2% y/y in July against the 3.3% consensus, which was a little softer. But, it marked an uptick from last month’s 3% outcome. Meanwhile, the core gauge weakened slightly to 4.7% y/y from 4.8%, as expected. Treasury yields aimed higher as well – see chart below. A closer look at Federal Reserve monetary policy expectations reveals that while the report did little to alter near-term interest rate bets, the broader horizon looks a little bit different. The 3+ year horizon added the most tightening, which speaks to a central bank that is hawkish for longer. During the past 24 hours, San Francisco Fed President Mary Daly mentioned that the central bank still has “more work to do”. As such, it is unsurprising to have seen longer-term Treasury rates rally the most as it reflects financial markets increasingly looking at a central bank that delays the next rate cut cycle. Gold, being the anti-fiat instrument, unsurprisingly did not fare well. Gold and Treasury Yields After US CPI Data Gold Technical Analysis These developments are leaving the yellow metal in a precarious state heading into the final 24 hours of this week. On the daily chart below, gold appears to be confirming a breakout under a rising trendline from February. From here, immediate support is the 38.2% Fibonacci retracement level at 1903. Pushing below this price opens the door to an increasingly bearish technical bias. XAU/USD Daily Chart https://www.dailyfx.com/news/gold-price-outlook-at-risk-as-markets-embrace-tighter-fed-for-longer-after-us-cpi-20230810.html

.png)

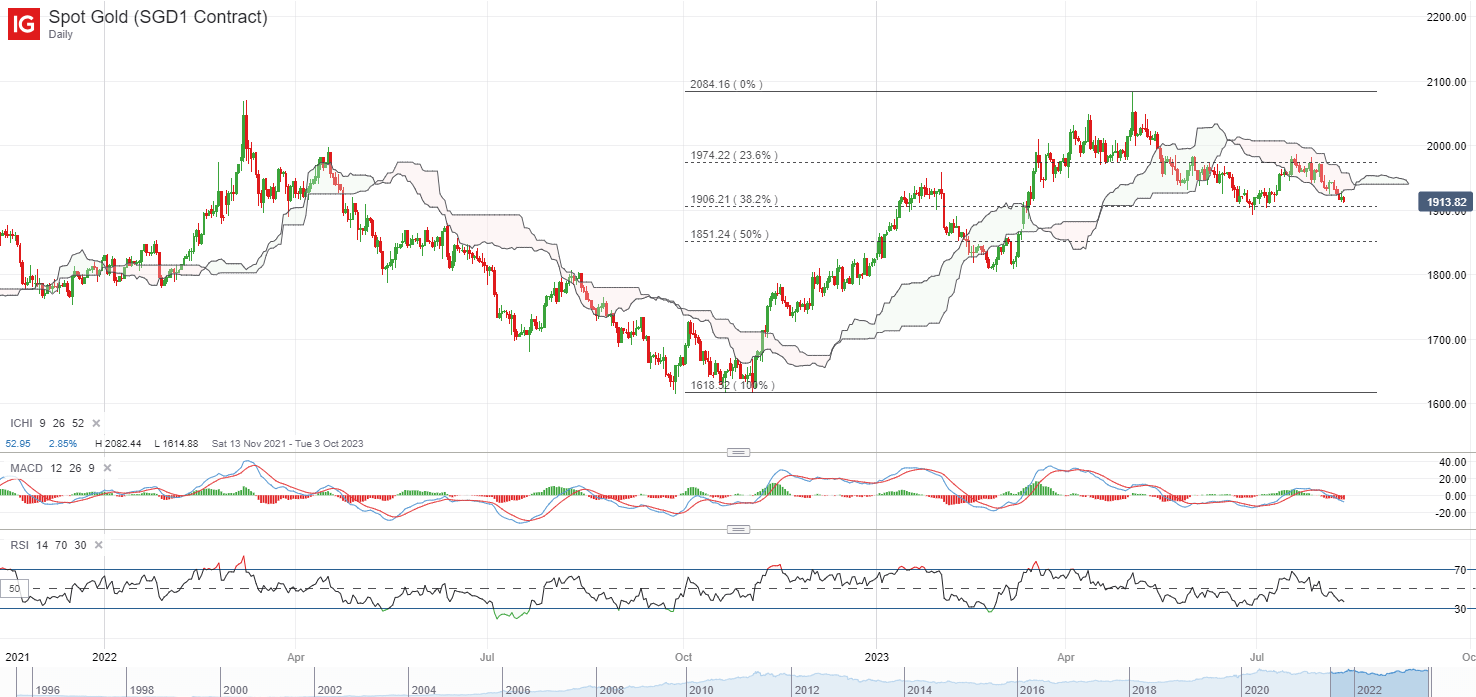

2023-08-11 03:41

An initial rally in Wall Street eventually fizzled into the close, as Treasury yields headed higher in the aftermath of the US Consumer Price Index (CPI) release, prompting the US dollar to pare its earlier losses. Both headline and core US CPI surprised on the downside, which will likely provide grounds for the Fed to keep rates on hold in September, but with Fed funds rate expectations already priced heavily for an end to the Fed’s tightening process, some selling on the bounce seems to be triggered. The real-time daily inflation estimates from the Cleveland Fed also suggests that US headline inflation may continue to pull ahead further this month, which will likely keep the Fed on their toes. For now, the US core CPI has ticked lower to 4.7% versus the 4.8% expected. On the other hand, headline inflation has seen its first increase since August 2022, rising to 3.2% from previous 3% (consensus 3.3%) on higher energy costs. Month-on-month, both registered an expected 0.2% increase. The day ahead will leave US producer prices and consumer sentiment data on watch. A similar story is expected for US headline producer prices to reveal a 0.7% increase year-on-year from previous 0.1%, while the core aspect is expected to tick slightly lower to 2.3% from previous 2.4%. Given the lukewarm reaction to the recent CPI data, it seems that some market indecision is in place, with one to watch if market sentiments will turn to selling the bounce once more. Higher yields have not been well-received by gold prices, which continues to head lower to its one-month low overnight after treading in its Ichimoku cloud resistance over the past weeks. The US$1,900 level may have to see some defending ahead, with previous dip-buying efforts sighted at this level. Its RSI on the weekly chart is also back at its key 50 level, with any failure to defend the 50-mark potentially indicating a wider trend reversal to the downside. Source: IG charts Asia Open Asian stocks look set for a subdued open, with ASX -0.15% and KOSPI +0.07% at the time of writing. Japan markets are closed today due to holiday. The pocket of relief may come from the release of Alibaba’s results yesterday, which reflected a more resilient showing with a top and bottom-line beat. The Nasdaq Golden Dragon China Index is up 0.7%, but given that a recovery in China’s economic conditions still lacks conviction at current point in time, traction towards Chinese equities could remain more lukewarm. This morning, Singapore’s final estimates for 2Q GDP has registered a softer read of 0.1% growth quarter-on-quarter (initial estimate: 0.3%), which may dampen previous optimism and continue to highlight the challenges in the manufacturing sector from a weak external demand outlook. More notably, the Ministry of Trade and Industry (MTI) has narrowed its GDP growth forecast for this year to ‘0.5% to 1.5%’ from the previous ‘0.5% to 2.5%’, which puts in place a more subdued growth picture through the rest of the year. With the local banks’ results behind us, the Straits Times Index will have to seek out other catalyst in order to sustain its recent rally. Recent attempt to bounce off a 38.2% Fibonacci retracement level seems to reflect some lingering caution with more measured green candles. The 3,330 level will be an immediate resistance to overcome ahead, while on the downside, its recent low at the 3,287 level will be one to watch. Source: IG charts On the watchlist: GBP/USD heads below trendline support Ahead of the UK GDP release, the GBP/USD has failed to hold above an upward trendline support in place since October last year, with dragged lower by a stronger US dollar lately. This has brought the pair back to retest a support confluence at the 1.264 level, where the lower edge of its Ichimoku cloud on the daily chart coincides with its 100-day moving average (MA). Breaking below the 1.264 level may potentially pave the way to retest the 1.239 level next. The upcoming UK 2Q GDP data is expected to turn in a 0.2% growth, unchanged from 1Q, which will suggest that the UK economy has managed to steer clear of a recession for now. Monthly GDP is expected to register a 0.5% year-on-year growth for June. But given that the Bank of England (BoE) is expected to push on with further tightening over the coming months, downside risks to growth conditions persist. Any weaker-than-expected GDP read ahead may challenge views of a more aggressive BoE and weigh on the pair further. Source: IG charts https://www.dailyfx.com/news/asia-day-ahead-subdued-start-in-asia-as-wall-street-rally-fizzles-20230811.html

2023-08-11 03:38

For so many countries, getting inflation down has been a real challenge. So, a bit of deflation might be seen as a good thing. But the opposite of inflation is also a problem for an economy. And the existence of deflation in a period when the economy is supposed to be growing, can be a significant warning sign. Yesterday, China reported an annual CPI of -0.3%, which was actually higher than the -0.4% expected. An important portion of that could be down to base effects, because the monthly rate grew once again at 0.2%. But the fact that the world’s second largest economy is seeing deflation right after reporting a significant slowdown in trade can be a problem for the global economy. Markets are under pressure There were several issues that have continued to hurt risk appetite through the start of the week, such as the downgrade of several US banks. But the situation in China is apparently the largest factor driving markets lately, as investors are once again pricing in the chance of a global recession. Just that now it seems more likely to be due to China underperforming than the US. Typically, August is a growth month for markets, fueled by summer optimism with many risk events taken off the table. The reversal in fortunes usually doesn’t come until September. But, the summer might be ending a little early this year, as risk shifts away from the US towards China. To further emphasize that trend, 499 of the S&P 500 components have reported as of yesterday, with over 80% beating earnings estimates, with an average beat of 7%. That exceeds the inflation rate of the period, suggesting US major corporations are seeing growing profits. The China risk Meanwhile, a slowing economy despite the Chinese government’s best efforts to push domestic demand seems to be the best explanation for the recent deflation reports. Headline inflation benefited from an increase in fresh food supplies. But what concerns global markets is that factory-gate inflation was negative. That means slowing demand for Chinese-made industrial products. The other major driver of falling prices in China was a drop in commodity prices, driven by slowing demand. That could have knock-on effects on China’s major suppliers, notably the Australian dollar. China has continued to buy many commodities, including crude – but that buying has gone to stockpiles, as domestic demand remains weak. With Chinese factories selling less, as measured in fewer exports, demand for raw materials remains under pressure. What about gold? Besides commodities, China is the world’s largest retail buyer of gold. The central bank keeps adding to its gold reserves. But, with a slowing economy, Chinese citizens are less likely to have extra capacity to buy gold. Additionally, a strengthening currency reduces the motivation to buy gold, as well. With investors piling into safe havens like the dollar, commodities priced in dollars including gold, could come under renewed pressure. Crude being the notable exception, as a more resilient than expected US economy has seen increasing demand from the world’s largest consumer. https://www.orbex.com/blog/en/2023/08/china-deflation-and-commodity-currency-outlook

2023-08-11 03:37

EURUSD struggles for bids The euro slips as consumers across the Euro zone lower their inflation expectations. On the daily chart, the pair is looking to hold onto July’s lows around 1.0840 as the euro’s recovery seems to have gained traction this year with a series of higher lows. A close above the immediate resistance of 1.1020 has eased the selling pressure but came to a halt at 1.1040. The bulls may need to consolidate their gains before they could push back once for all. 1.0910 is the closest support and its breach would trigger a retest of 1.0840. USDJPY bounces back The Japanese yen retreated as consumer spending continued to shrink in June. The greenback has met some buying interests at the resistance-turned-support of 141.50 after a brief retracement. 143.80 where the previous rally came under pressure is a major ceiling to lift. A breakout would force the remaining bears out and cause a runaway rally above the recent high of 145.00, paving the way for a bullish continuation in the weeks to come. On the flip side, a fall below 142.40 would expose the key level at 141.50. USOIL claws back losses WTI crude recouped losses after the EIA painted a rosy picture of US GDP growth in 2023. A brief fall below 80.80 earlier this month has allowed some long positions to close in profit, shaking out weaker hands in the process. After the psychological level of 80.00 proved to be a solid support with the RSI’s double dip in the oversold zone attracting renewed bids, a fresh high near April’s peak of 83.40 is a sign that the bulls are still in control of the direction. A bullish breakout may trigger a broader rally to last November’s high of 93.00. https://www.orbex.com/blog/en/2023/08/intraday-analysis-usd-gains-support