2025-09-10 06:38

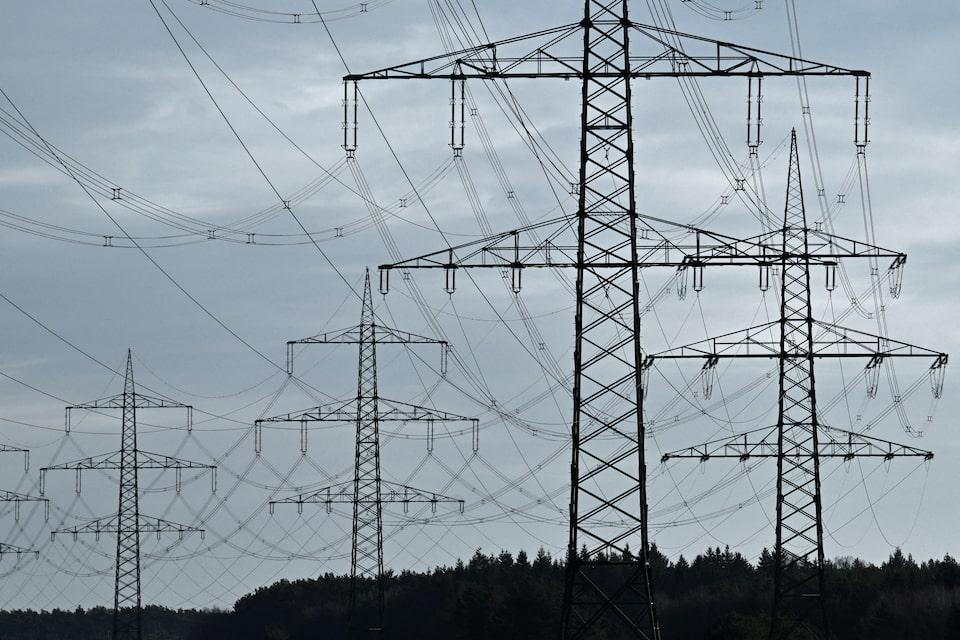

SOFIA, Sept 10 (Reuters) - Nearly four years after Europe’s energy crisis erupted in late 2021, the continent has moved from emergency response to system redesign. But the European Union is not out of the woods. Deep vulnerabilities persist, and progress toward clean, secure and affordable supply is highly uneven across the continent. The Energy and Climate Security Risk Index , opens new tab (ECSRI), developed by the Center for the Study of Democracy (CSD), measures energy security across four pillars: geopolitics, affordability, reliability and sustainability. Its findings reveal a widening energy security divide between leaders like France, Sweden and Denmark and laggards such as Hungary, Italy and Bulgaria. Sign up here. Europe’s biggest success on the energy security front has been reducing dependence on Russian fossil fuels. Gas imports from Russia have fallen from about 40% of EU supply in 2021 to around 10% in 2025, according to Eurostat. EU members achieved this by boosting purchases from the U.S., Norway and Qatar. Countries such as Italy and Germany that used to be some of the biggest consumers of Russian energy have almost ceased Russian gas imports, but several nations in Central Europe remain highly exposed. Hungary still buys more than three-quarters of its gas from Russia, based on estimates using Eurostat data, and Slovakia remains tied to Russia's Gazprom (GAZP.MM) , opens new tab contracts. New dependencies are also emerging, however. First, the EU now gets much of its liquefied natural gas (LNG) from the U.S., leaving it vulnerable in future negotiations with Washington on trade or other matters. Additionally, Europe’s rapid buildout of solar, wind and battery infrastructure has increased Europe’s reliance on Chinese supply chains. China dominates refining of many critical minerals. It processes , opens new tab over 60% of global lithium, 80% of cobalt, and around 70% of rare earths, all critical for the EU energy sector. Without diversification, Europe risks replacing one dependency with another. Yet Europe is not without options. France has significantly increased its silicon refining capacity for solar manufacturing, while Sweden already supplies up to 90% of the EU’s domestically produced iron ore and is expanding its copper and zinc output. Portugal is developing vast lithium reserves, and Finland hosts major nickel and zinc refineries. In the EU’s neighbourhood, Serbia’s Jadar mine could meet nearly 90% of Europe’s lithium current needs if commissioned, though those needs are expected to rise significantly in the coming years. Ukraine is also believed to hold significant titanium and rare earth deposits, but whether these can be mined and processed profitably remains an open question. AFFORDABILITY CHALLENGES If geopolitics defined energy policy in 2022, affordability is now the central challenge. Affordability risks in Europe have surged fivefold since 2020 largely due to the price shocks following Russia’s invasion of Ukraine. Retail power and gas bills remain 40–70% above pre-crisis levels in Southern and Eastern Europe, with coal-heavy Poland, Bulgaria and the Czech Republic the most vulnerable, based on an analysis of Eurostat data. Nordic countries and France, with less-carbon-intensive systems, face much lower affordability risks. European industry remains under significant pressure due to high energy costs. Between 2021 and 2024, more than 1 million industrial jobs disappeared from Europe, largely due to elevated energy costs. Without long-term clean power contracts and stronger efficiency measures, Europe risks losing competitiveness. RELIABILITY ISSUES The nature of energy reliability risks has also shifted in Europe. In an energy system dominated by fossil fuels, the challenge was securing supply. Today, the problem is that renewables are being rapidly integrated into grids without the infrastructure to underpin them. A clear example of this was the blackout that struck the Iberian Peninsula in April. The sudden loss of 15 gigawatts of solar power overwhelmed systems dominated by inverter-based generation that lacked sufficient backup. Wealthier states like Germany and the Netherlands are investing in digitalised grids, interconnections and storage. However, in Central and Eastern Europe, outdated grids and limited investment leave energy systems exposed to future outages. SUSTAINABILITY GAP On sustainability, the EU has set ambitious goals through the Green Deal, Fit for 55 and REPowerEU. But implementation is uneven across the region. For example, Sweden, Denmark and Finland have combined renewables, industrial decarbonisation and strong governance to reduce their risk here. And France benefits from nuclear power, which has kept a lid on emissions and costs. In contrast, many Central and Eastern members are constrained by legacy infrastructure and weaker governance. In turn, they are seeing both emissions and energy costs rise. Importantly, the ECSRI suggests that energy risks tend to cluster, as countries with high sustainability risks also typically face affordability and geopolitical challenges. Those integrating clean energy, industrial strategy and grid investment are more resilient across the board. The past four years proved Europe can act in crisis, but the next phase of the energy transition will require more than just reactive policy. It will demand a long-term coherent strategy and better coordination across the region – a heavy lift. But the energy security data make one thing clear: without closing the energy policy divide, Europe’s prosperity and sovereignty remain at risk. (The views expressed here are those of Martin Vladimirov, Director of the Geoeconomics Program of the Center for the Study of Democracy (CSD)). Enjoying this column? Check out Reuters Open Interest (ROI), , opens new tab your essential new source for global financial commentary. ROI delivers thought-provoking, data-driven analysis of everything from swap rates to soybeans. Markets are moving faster than ever. ROI, , opens new tab can help you keep up. Follow ROI on LinkedIn, , opens new tab and X. , opens new tab https://www.reuters.com/markets/commodities/europes-next-big-challenge-is-closing-its-energy-security-divide-2025-09-10/

2025-09-10 06:37

MUMBAI, Sept 10 (Reuters) - The Indian rupee inched lower on Wednesday with focus remaining on U.S. tariffs, while near-term implied volatility hit multi-month lows, signaling that traders see limited risk of a large decline in the Asian currency. The rupee was trading at 88.1250 per U.S. dollar at 12:02 p.m. IST, down from 88.1025 on Tuesday and just 0.2% shy of its record low of 88.36 hit last Friday. Sign up here. The currency in late August weakened past 88 per dollar for the first time, sparking expectations of a sharp fall. That has not materialised so far. An increase in implied volatility after the currency drop has also faded. Typically, when a currency is near all-time lows, traders brace for larger swings and implied volatility tends to rise. The 10-day realized volatility has been holding below 4%. Tracking this relative calm, one-month implied volatility has declined to levels last seen in March. The subdued expectations for near-term swings despite the rupee hovering near lifetime lows reflects in part the stabilizing role of the Reserve Bank of India's intervention, bankers say. Corporates have been steadily selling volatility, "and RBI has done an excellent job in managing spot," an FX derivatives trader at a private sector bank said, "That is why implied volatility keeps falling." ALL ABOUT TARIFFS Rupee traders are squarely focused on U.S.-India trade relations, a key driver for the currency’s near-term direction. On this front, developments offered a mix of positive and negative signals. U.S. President Donald Trump said on Truth Social that Washington and New Delhi are continuing negotiations to address trade barriers, expressing confidence in a successful outcome. At the same time, he pushed the European Union to impose tariffs of up to 100% on India over their purchases of Russian oil, a move that could add fresh pressure on the rupee. https://www.reuters.com/world/india/rupee-drifts-lower-volatility-hits-multi-month-lows-2025-09-10/

2025-09-10 06:34

Israeli strike on Hamas leadership in Qatar supports prices Trump asks EU to put tariffs on China, India to pressure Russia Possibility of secondary tariffs spurs supply concerns Longer-term outlook still for oversupply as OPEC+ ups production BEIJING, Sept 10 (Reuters) - Oil prices rose on Wednesday after Israel attacked Hamas leadership in Qatar and U.S. President Donald Trump asked Europe to impose tariffs on buyers of Russian oil buyers, though a weak market outlook capped further gains. Brent crude futures were up 61 cents, or 0.92%, at$67 a barrel, as of 0620 GMT, and U.S. West Texas Intermediate crude futures gained 61 cents, or 0.97%, to $63.24 a barrel. Sign up here. "The current uptick in oil prices has been primarily attributed to an increase in geopolitical risk premiums after Israel's unprecedented strike in Doha," said Kelvin Wong, senior market analyst at OANDA. "This increases the fears of a short-term supply crunch if OPEC+ members' oil production facilities are hit by Israel." Prices had settled up 0.6% in the previous trading session after Israel said it had attacked Hamas leadership in Doha, which Qatar's prime minister said threatened to derail peace talks between Hamas and Israel. The oil price reaction was relatively muted due to overall market weakness. Both benchmarks rose nearly 2% shortly after the attack, but retreated after the U.S. assured Doha that such an incident would not recur on its soil and because there was no immediate impact on supply. "The modest reaction in crude oil prices to this news, along with scepticism regarding U.S. President Trump's claims about potentially ramping up sanctions on Russian oil ... leaves crude oil vulnerable to lower prices," IG market analyst Tony Sycamore said in a note. Trump has urged the European Union to impose 100% tariffs on China and India as a strategy to pressure Russian President Vladimir Putin, according to sources. China and India are major buyers of Russian oil, which has helped to support Russia's coffers since it launched its invasion of Ukraine in 2022, despite heavy sanction pressure from the U.S. "The expansion of secondary tariffs to other major buyers such as China could disrupt Russian crude exports and tighten global supply, a bullish signal for oil prices," LSEG analysts wrote. "However, uncertainty remains over how far the administration will go, as aggressive action could conflict with efforts to manage inflation and influence the Federal Reserve to reduce interest rates." Traders expect the Federal Reserve to cut interest rates in its meeting next week, which would boost economic activity and demand for oil. But the supply outlook remains bearish. The U.S. Energy Information Administration cautioned global crude prices will be under significant pressure in the coming months because of rising inventories as OPEC+ increases output. https://www.reuters.com/business/energy/oil-prices-rise-after-israeli-attack-qatar-trumps-russia-tariff-push-2025-09-10/

2025-09-10 06:31

GDANSK, Sept 10 (Reuters) - Poland's biggest energy utility PGE (PGE.WA) , opens new tab reported a second-quarter net loss of 9.61 billion zlotys ($2.65 billion) on Tuesday, in line with the company's estimates as impairments on its tangible assets took a toll. WHY IT'S IMPORTANT PGE is the biggest state-controlled Polish utility, with market capitalisation of 24.83 billion zlotys. Sign up here. The substantial loss, driven by write-downs on its conventional assets, highlights the financial cost of Poland's energy transition and underscores the urgency behind the company's strategic pivot away from fossil fuels and toward its new investment plan. CONTEXT PGE, like other Polish utilities, is navigating structural shifts in the country's energy landscape as it transitions away from coal. In June, it unveiled a new strategy to invest 235 billion zlotys by 2035 in renewable, gas-fired power plants, and energy storage. The company had previously announced it expected a net hit of around 11.6 billion zlotys in the first-half from impairments on its tangible assets, mainly related to its conventional energy segment. BY THE NUMBERS The company's reccuring earnings before interest, taxes, depreciation, and amortization (EBITDA) for the first half of the year was 7.60 billion zlotys. Sales revenue for the quarter stood at 13.80 billion zlotys. ($1 = 3.6291 zlotys) https://www.reuters.com/sustainability/climate-energy/pge-swings-quarterly-net-loss-asset-write-downs-2025-09-10/

2025-09-10 06:30

Sept 10 (Reuters) - The impact of U.S. tariffs on the Indian economy will be partially offset by recent consumption tax cuts that are expected to boost domestic demand, India's Chief Economic Advisor said on Wednesday. The goods and services tax (GST) cuts announced by Prime Minister Narendra Modi's government would have "compensating effects" on India's economy, V. Anantha Nageswaran said. Sign up here. The net impact of higher tariffs and lower domestic taxes will be a drop of 0.2%-0.3% points on GDP growth estimates for the year, he said. India's GDP growth for the current financial year is projected at 6.3%-6.8%. "GST reforms will play a very good offsetting role, by substituting domestic demand for whatever the export demand that may not materialise from the United States," Nageswaran said. The initial impact of U.S. tariffs on Indian goods in the current financial year will be limited, but prolonged tariff uncertainty from the 25% penalty duty imposed by the United States on India for buying Russian oil could weigh on the South Asian economy, he said. https://www.reuters.com/world/india/indias-tax-reforms-partially-offset-tariff-hit-gdp-growth-economic-adviser-says-2025-09-10/

2025-09-10 06:29

LONDON, Sept 10 (Reuters) - A sense of normality has returned to the copper market now the threat of U.S. import tariffs on refined metal has been deferred. Physical copper is still flowing into CME warehouses after the rush to move metal to the United States but the CME spot premium over the London Metal Exchange (LME) is now stabilizing around the $100 per ton level, which is pretty much where it was before the tariff scare. Sign up here. Fund managers, however, are still fighting shy of the metal after the roller-coaster ride in the first part of the year. Investor positioning on the CME copper contract shrank to a decade-low in August and has edged up only slightly since. Investors remain net long but largely thanks to a complete collapse in short positions. Bulls, meanwhile, are only tentatively dipping their toes back in the water. The tariff heat may have gone out of the market, but there is still little light on price direction as physical arbitrage flows muddy the fundamental picture. Fund managers have evidently decided there is easier money to be made in other commodity sectors, particularly precious metals. BEAR EXODUS Fund positioning, long and short, on the CME copper futures contract sank to just 51,685 contracts on August 18, which was the lowest level of participation since 2013. The mass departure of investors resulted in average daily volumes slumping by 42% to 53,776 contracts, the lowest activity rate since December 2021. Trading in the CME's main copper options contract fell even more, by 56% year-on-year. Particularly noticeable has been the exodus of short-position holders among the investment community. Outright short positions have collapsed from a February high of 72,858 contracts to just 11,792, the lightest bear positioning since 2011. The first half of the year was a scary time to be short CME copper as the U.S. price soared to a record premium over the LME international price. It wasn't easy being a bull either, given the extreme volatility in the U.S. premium trade. Fund long positions are also much reduced relative to the first months of 2025. They hit a three-year low of 35,447 contracts last month but have since picked up to 46,443 contracts. THE LURE OF GOLD Funds are still evidently bruised from the tariff tumult and remain wary of copper, or at least the CME copper price, which will continue to be highly sensitive to any change in tariff policy. President Donald Trump's administration has left the door open to a possible phase-in of refined copper import tariffs from 2027, which in Trump-time is a very long time indeed. Nor is the copper market generating any clear technical signals, which are the lifeblood of momentum funds. The London Metal Exchange (LME) copper price has been trading a $9,500-10,000 per ton range since May and the CME price is also now churning sideways after the tariff implosion at the end of July. Fundamental signals have been distorted by the massive relocation of copper to the United States, where CME inventory of 277,400 tons is now higher than LME and Shanghai Futures Exchange stocks combined. Until copper regains directional impetus, upwards or downwards, there are richer pickings for investors in the super-hot gold and silver markets. By nominal value, managed money accounts now hold 47% of their total commodity exposure in gold and 7% in silver, according to Ole Hansen, head of Commodity Strategy at Saxo Bank. With gold prices hitting another record high of $3,659 per ounce on Tuesday and silver trading above the $40-per ounce level for the first time since 2011, it could be a while before funds commit again to copper. The opinions expressed here are those of the author, a columnist for Reuters. https://www.reuters.com/markets/commodities/bruised-funds-retreat-copper-after-tariff-turbulence-2025-09-10/