like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

US equities defied logic for the first half of 2023 but has shown signs of concern more recently as the Fed makes its final policy adjustments before attempting to dismount from its aggressive rate hiking campaign. The fundamental landscape appears to be changing as equity markets struggle to bounce back with the same vigour as before. The Fed’s promise to maintain a restrictive stance sees real yields beginning to detract from expensive US stocks, the AI hype-train slows on TSMC demand concerns, and tech stocks show signs of vulnerability to higher rates.

Without actually hiking rates the Fed issued a hawkish message with the assistance of its summary of economic projections. The committee wiped out 50 basis points worth of cuts next year while raising estimates of growth and longer-term inflation. Equity markets appeared to look right past the growth story and focused on the chance of fewer cuts next year, effectively delaying when the first cut is likely to materialise. Raising rates to such restrictive levels and then holding can be likened to doing stomach crunches until you really start to fatigue and then being told to hold at the top. It’s going to be a major challenge!

Rising rates have spurred US treasury yields higher. So much so, that the ‘risk-free’ 10-year yield is on the cusp of catching the S&P 500 earnings yield. Should equity values continue to decline into Q4, investors would be tempted to pivot from risky stocks into bonds purely to receive that risk-free yield. Elevated interest rates globally also weighs on US stocks moving forward as foreign revenues are likely to come under pressure.

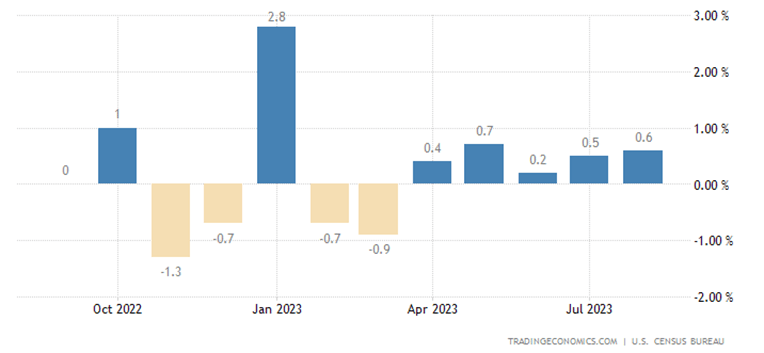

The US economy has put in an impressive performance ever since that technical recession in 2H 2022 and shows little sign of petering out and the Fed agrees. An uncharacteristically robust labour market means more people are employed and have discretionary income at their disposal. Of course, higher rates reduce disposable income but there is still a lot of money changing hands within the local economy. Services PMI data also remains in expansion territory but has been edging closer to the all-important 50 mark separating expansion from contraction.

US Retail Sales Data (Monthly)

Source: Tradingeconomics, Prepared by Richard Snow

Additionally, forecasters now see earnings per share (EPS) growth turning positive for the first time since Q3 2021. While earnings per share consistently beat estimates throughout 2023, expectations had been moving lower as rate hikes flew higher. Now, in the first two months of Q3 analysts collectively reported higher expected EPS growth into year end.

Source: Factset, Prepared by Richard Snow

From a seasonal perspective, US stocks (using the S&P 500 as a proxy here) tend to rise over Q4 but something to look out for is the increased variation in returns over the near 23-year period analysed. The observed standard deviation in October and November is higher than that witnessed in other periods.

Source: Refinitiv, Prepared by Richard Snow

https://www.dailyfx.com/news/equities-q4-fundamental-outlook-fed-rate-outlook-to-weigh-on-stocks-20231001.html