like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

US Dollar Forecast: The Fed and US Yields Sustain USD Support

US DOLLAR WEEKLY FORECAST: NEUTRAL

- US treasury yields continue higher, reaching key levels

- Are DXY bulls running out of momentum? Consolidation pattern emerges

- Risk events: US Q3 GDP and PCE data, Middle East conflict, Mega-cap earnings

The ‘neutral’ stance adopted for the coming week was arrived at due to the following considerations:

- USD has not broken new ground despite a tendency for data to outperform consensus estimates (NFP, CPI, retail sales)

- Yields, which typically drive dollar valuations, continue to rise without much of an effect on the dollar.

- With safe-haven demand present in the gold market and the S&P 500 ‘fear gauge’ (VIX) picking up, there’s been little movement in the dollar – a typical safe haven.

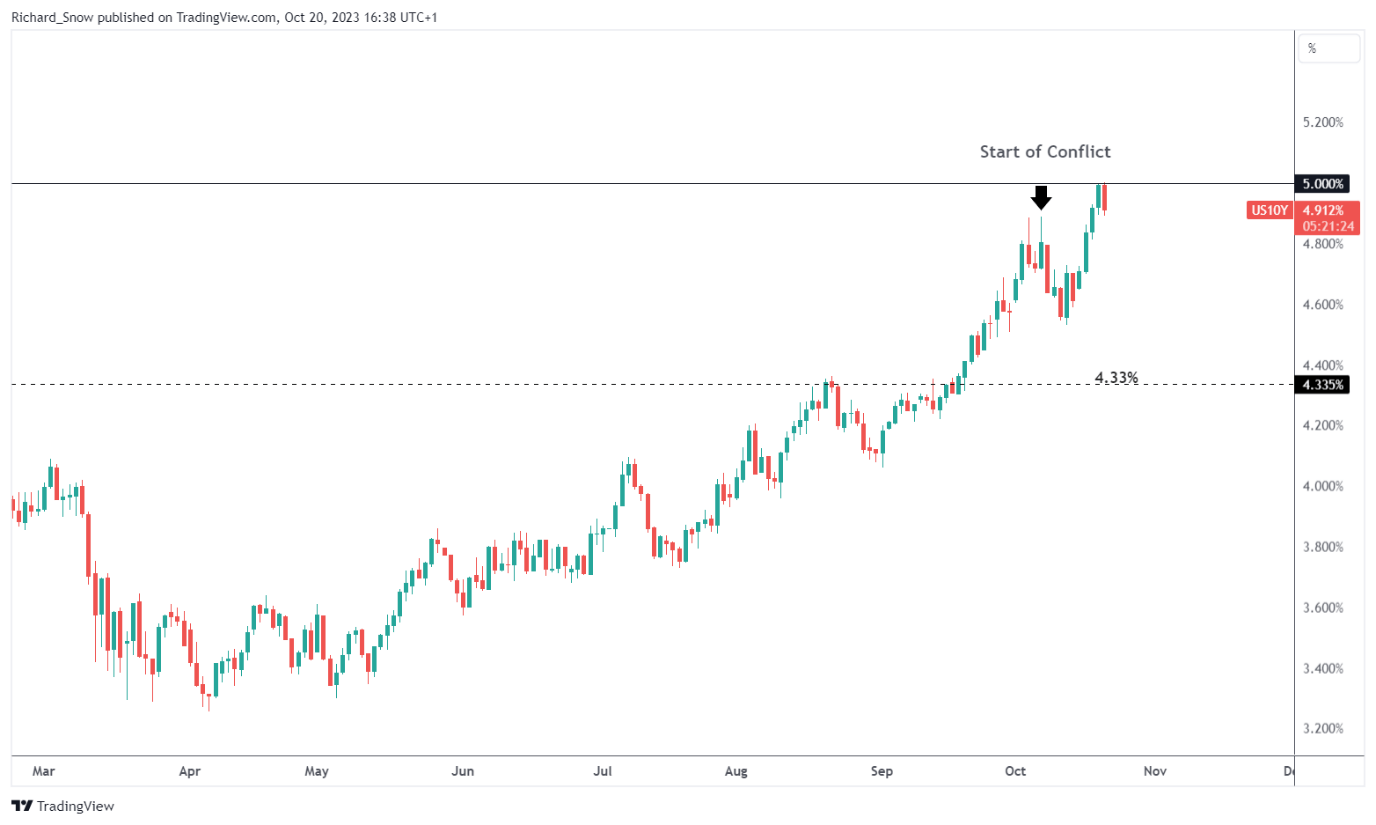

US TREASURY YIELDS CONTINUE HIGHER, REACHING KEY LEVELS

One of the most widely followed benchmarks is the US 10-year yield, which hit the psychological 5% level yesterday after prominent Federal Reserve Bank officials continued to tow the line on the widely supported policy stance summed up as ‘higher for longer’.

Yields typically influence the dollar and the fact that there hasn’t been a continuation of the prior uptrend suggests the dollar may be reaching a peak. If not, then it would require a massive catalyst to kickstart the upward momentum – perhaps to be provided by US Q3 GDP data on Thursday.

US 10-Year Treasury Note Yield

Source: TradingView, prepared by Richard Snow

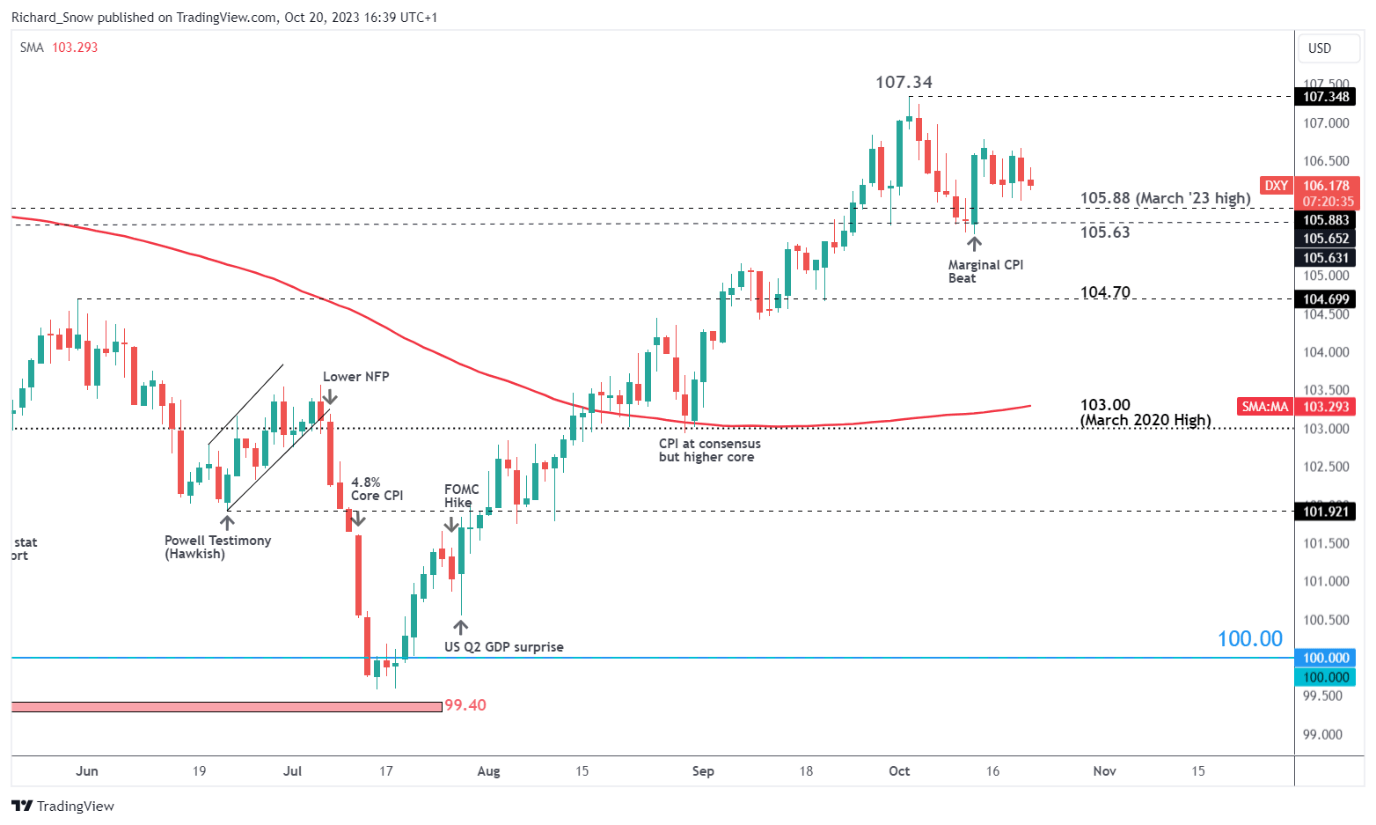

DXY BULLS RUNNING OUT OF MOMENTUM?

The US dollar basket (DXY) struggled to build on the surge higher after the CPI print revealed lingering price pressures last Thursday. In fact, despite other fundamental drivers listed at the beginning of this forecast, the dollar has actually dipped and consolidates around lower levels.

The inability for the dollar to make new highs does not mean it is primed for a reversal. However, the fact that price action has moved sideways despite strong fundamental backing is a sign of bullish fatigue.

Immediate (intra-day) levels of support appear at 105.88 and 105.63 but a close on the daily chart below 104.70 needs to materialize before even entertaining the idea of a broader reversal. Resistance appears at the recent high followed by the 107.34 turning point.

US Dollar Basket Daily Chart

Source: TradingView, prepared by Richard Snow

MAJOR RISK EVENTS OF THE WEEK

Central banks re-emerge as the Bank of Canada and ECB provide updates on their respective monetary policies where the general consensus suggests no change on the interest rate front. Military activity has notched up in recent hours with more bombing in northern Gaza. As the conflict continues, market participants need to be aware if the ramifications in financial markets and the war will continue to play a major role in determining risk sentiment in the coming days/weeks.

US data continues with the first look at US GDP for the third quarter which is anticipated to reveal a further economic expansion in the US as the nation appears unaffected by restrictive financial conditions. US PCE on Friday will also attract the attention of many after US CPI data revealed robust price pressures for the month of September.

Keep in mind that third quarter earnings from mega-cap stocks Alphabet, Microsoft, Amazon and Meta are due next week potentially adding volatility. As always, markets will read into the forward guidance offered by the respective company heads about the current and future operating environment.

https://www.dailyfx.com/news/us-dollar-forecast-the-fed-and-us-yields-sustain-usd-support-20231022.html