like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

UK Autumn Statement: Tax Cuts, Business Investment and Debt Reduction

Main Takeaways from the 2023 UK Autumn Statement

- Main national insurance rate to be cut by 2%, from 12% to 10% for 27 million people

- Full expensing of capital investment for businesses made permanent. Business investment to improve by £20bn per year according to estimates

- State pensions to rise by 8.5% from April 2024

- Welfare benefits grow in line with the September’s CPI figure of 6.7% instead of the rumoured, lower October figure

Tax Cuts, Debt Reduction and Massive Boost to UK Businesses

Last autumn, Chancellor Jeremy Hunt was brought in as damage limitation, now he has a tiny bit of wriggle room in his budget and has his sights set on growth. Now that inflation has been halved and stimulus/support packages have been phased out, the government has a minimal amount of headroom within the budget which many were anticipating would be utilized to ease the burden of taxes. They were right, well kind of.

The tax cuts weren’t applied to income tax but rather to the percentage of national income tax that will be applicable to 27 million people in the UK. This has now created an expectation that the prime minister’s calls for a drop in the basic tax rate will be the main event of the pre-general election budget in the spring.

Furthermore, businesses will be able to fully expense investment expenditure permanently. This is potentially going to attract around £20bn worth of investment per year. In addition, the UK government is committed to reducing the rate of government borrowing compared to the rate of economic growth – with OBR forecasts seeing debt as a percentage of GDP fall for the majority of the forecast period, approaching the low 90% level.

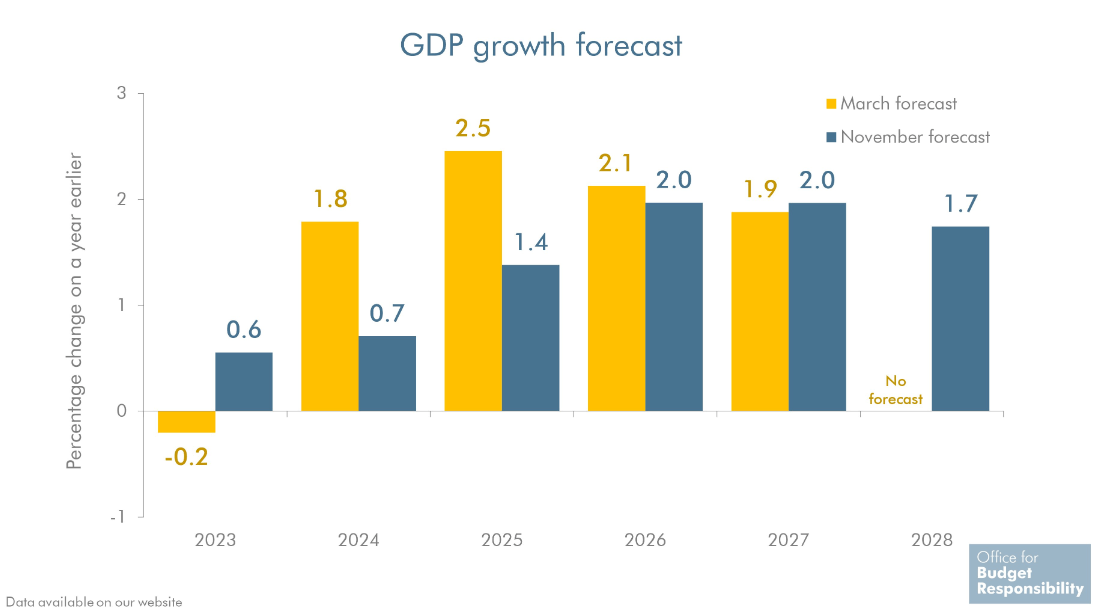

The OBR provided updates to its UK growth forecasts which were revised considerably lower – highlighting the need for increased productivity. 2023 is on track to outperform the March forecasts but that is where the good news ends. 2024 is expected to see a meagre 0.7% growth vs prior 1.8% and 1.4% growth in 2025 vs the earlier estimates of 2.5%. The IMF’s world economic outlook in October revealed growth of 0.5% and 0.6% in 2023 and 2024, respectively.

OBR Forecasts on UK Growth

Source: OBR, prepared by Richard Snow

Immediate Market Reaction

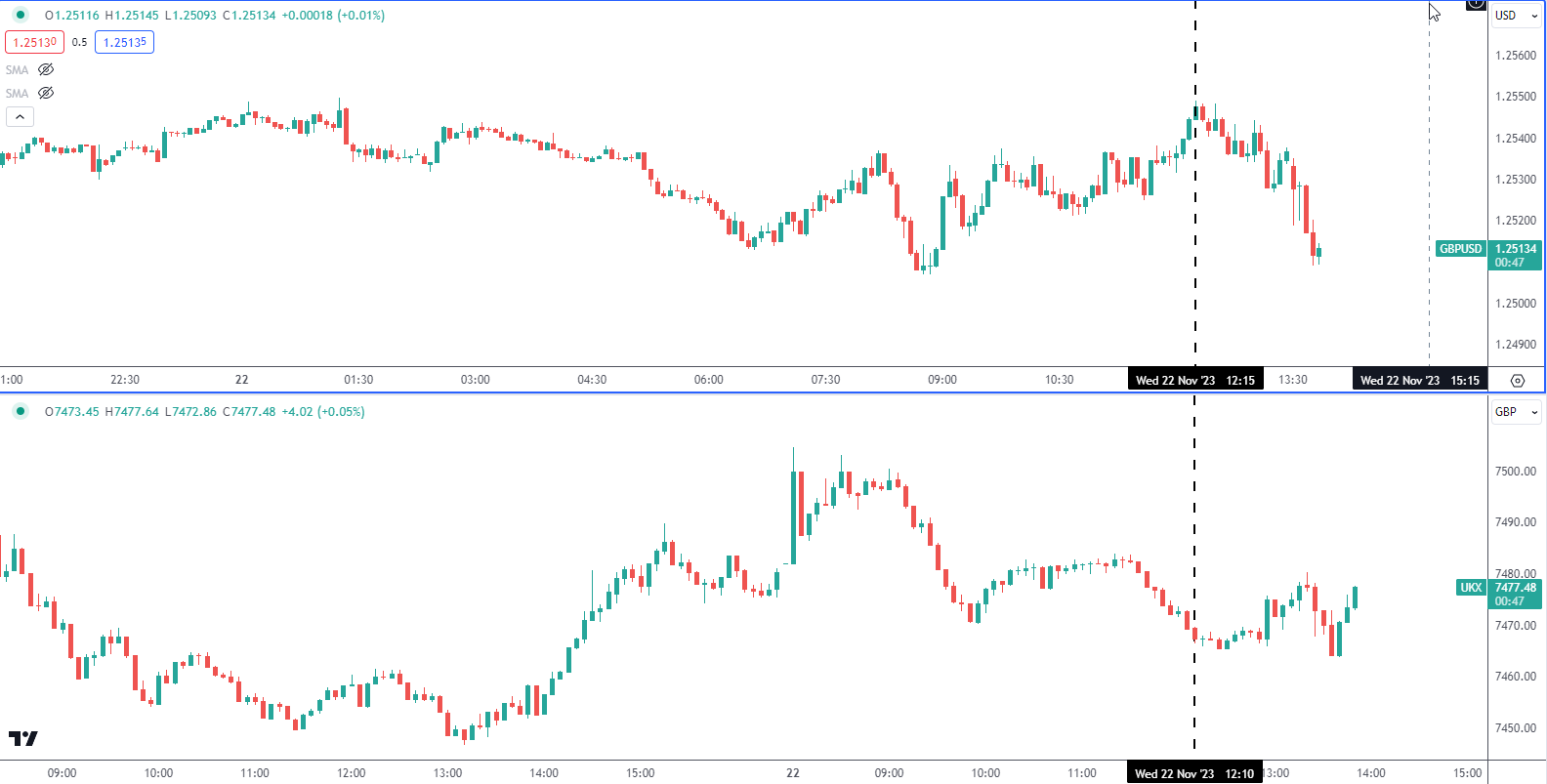

The statement saw little movement across UK assets as can be seen below via cable and FTSE 5-minute charts.

GBP/USD, FTSE 5-minute chart

Source: TradingView, prepared by Richard Snow

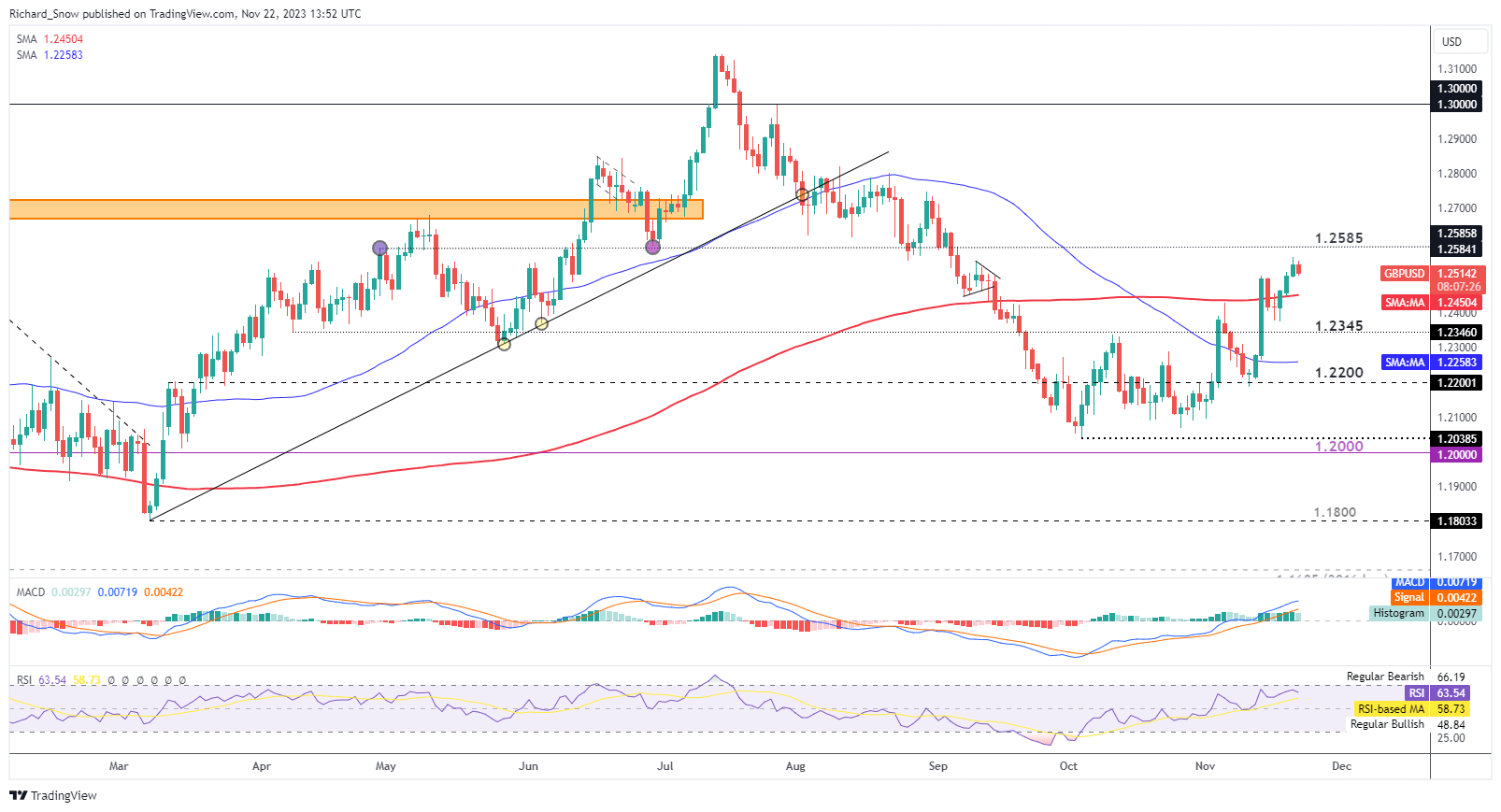

Sterling received a tiny boost yesterday as policy setters at the Bank of England (BoE) continued to warn about the upside risks to inflation and issued a warning over reading too much into recent inflation prints. This has buoyed cable despite the dollar also receiving a small boost after the rather hawkish but outdated FOMC minutes last night.

GBP/USD Daily Chart

Source: TradingView, prepared by Richard Snow

https://www.dailyfx.com/news/uk-autumn-statement-tax-cuts-business-investment-and-debt-reduction-20231122.html