like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

US Dollar Index (DXY) Unfazed as Business Activity in the US Held Firm

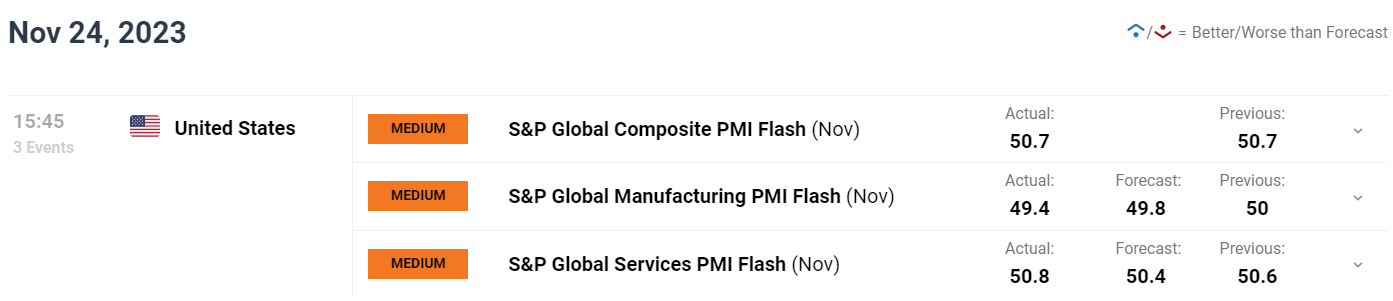

US PMI KEY POINTS:

- S&P Global Composite PMI Flash (Nov) Actual 50.7 Vs Previous 50.7.

- S&P Global Manufacturing PMI Flash (Nov) Actual 49.4 Vs Forecast 49.8.

- S&P Global Services PMI Flash (Nov) Actual 50.8 Vs Forecast 50.4.

- Employment Declined at US Service Providers and Manufacturers in November for the First Time Since Mid-2020 Amid Tepid Demand and Elevated Costs.

- To Learn More AboutPrice Action,Chart PatternsandMoving Averages, Check out theDailyFX Education Section.

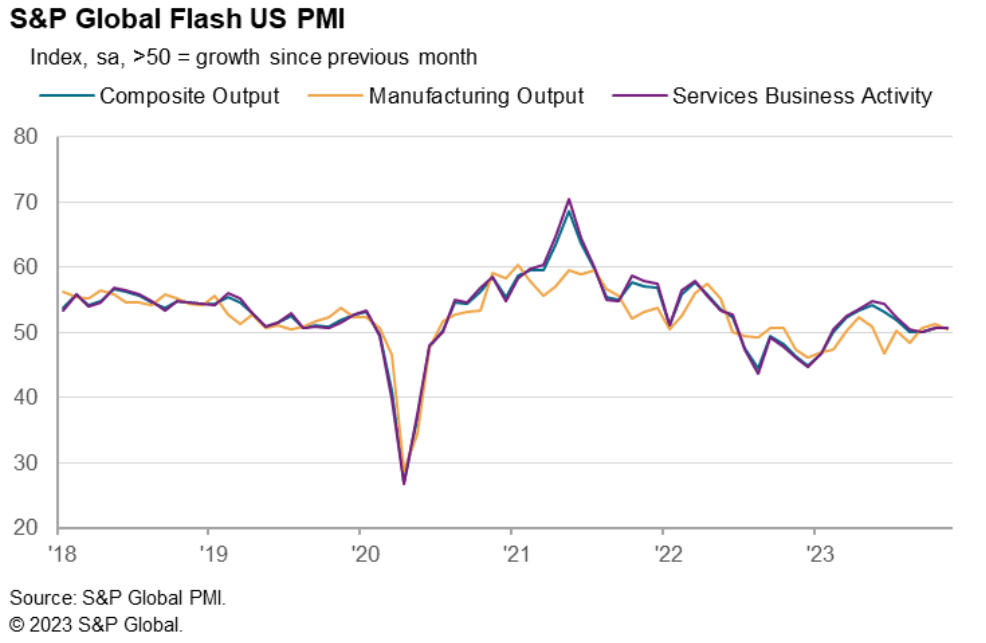

US Business Activity remained steady in November with a marginal expansion in output. The rate of growth in business activity in line with that seen in October. Although manufacturers and service providers registered another monthly rise in activity, paces of expansion were only slight overall.

Source: S&P Global PMI

Service providers witnessed a fractional uptick in the rate of output growth, the fastest since July. Total new orders increased slightly, driven by the first expansion in service sector new business in four months, while employment levels declined for the first time in almost three-and-a-half years. At the same time, total new export orders rose for the first time since July as manufacturers noted an expansion in new sales from external customers. Less robust expectations regarding the outlook for output over the coming 12 months at service providers weighed on overall business confidence in November.

Looking at pricing, input costs experienced the smallest increase since October 2020 due to lower energy and raw material expenses, while selling prices advanced at a faster pace.

Commenting on the data, Siân Jones, Principal Economist at S&P Global Market Intelligence said: “Moreover, demand conditions – largely driven by the service sector – improved as new orders returned to growth for the first time in four months. The upturn was historically subdued, however, amid challenges securing orders as customers remained concerned about global economic uncertainty, muted demand and high interest rates. On a more positive note, input price inflation softened again while selling price inflation remained subdued relative to the average over the last three years and was consistent with a rate of increase close to the Fed’s 2% target.”

THE US ECONOMY AND DOLLAR OUTLOOK

The US Economy continues to surprise and frustrate in equal measure. Each time we get a few data releases which suggest a cooling in the economy, it is usually followed by a data print that suggests the opposite. This week has been no different even though the calendar has been a bit quiet coupled with the Thanksgiving Holiday.

This week saw initial jobless claims fall once more just as it seemed that the labor market may be entering a phase of sustained cooling. This weeks print however will keep market participants on the edge heading into next month’s jobs data and inflation prints. A robust labor market will continue to keep demand at elevated levels and thus inflation and this is where the concern comes in. There was a positive on the demand front from todays report however as the report revealed that employment declined at US service providers and manufacturers in November for the first time since Mid-2020 amid tepid demand and elevated costs.

I still expect market participants to continue to flip-flop after every data release heading into next months Federal Reserve meeting which could clear things up a bit more. Personally, is still believe the road ahead will be a bumpy one with the DXY likely to struggle heading into 2024.

MARKET REACTION

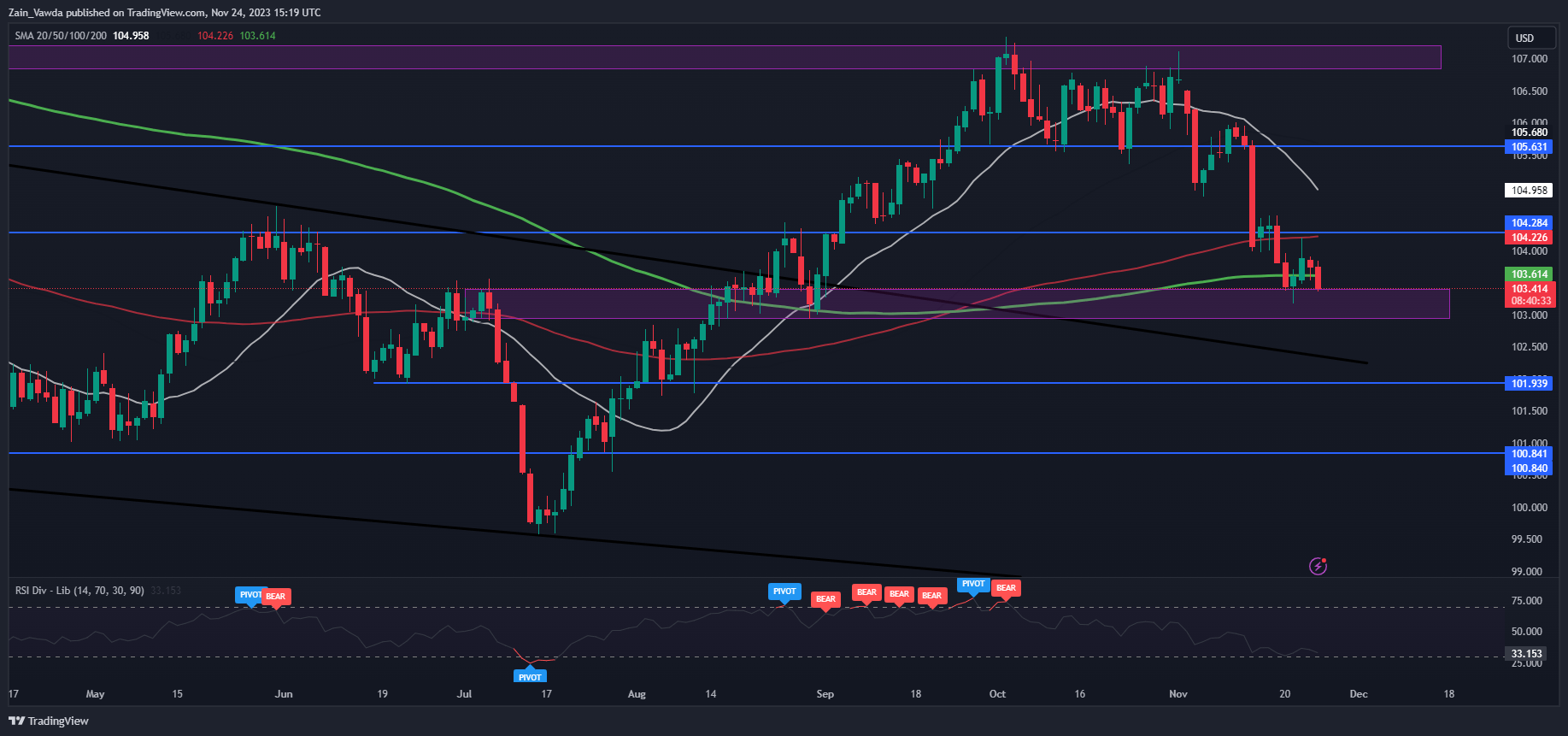

Dollar Index (DXY) Daily Chart

Source: TradingView, prepared by Zain Vawda

The Initial reaction to the data saw the DXY edge slightly lower into the key support area between the 103.40-103.00 area.

Looking at the bigger picture and the US Dollar Index was caught between the 100 and 200-day MA but is attempting to break and print a daily candle close below the 200-day MA. However, there is a key area of support resting just below around the 103.00 handle which poses a bigger threat to further US Dollar downside.

Looking at the potential for a move to the upside and immediate resistance rests at 104.24 with the 20-day MA resting higher at the 105.00 psychological level. This however would require a stark change in fortune for the Greenback in the early part of next week.

https://www.dailyfx.com/news/us-dollar-index-dxy-unfazed-as-business-activity-in-the-us-held-firm-20231124.html