like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

Japanese GDP Strained by Rising Inflation and BoJ Spurs Hawkish Bets

Japanese GDP and JPY Analysis

- Japanese Q3 GDP revised lower as inflation weighs on spending

- Japanese government bond yields recover sharply, buoying the yen

- Non-farm payrolls could extend recent moves on weaker jobs data

- The analysis in this article makes use of chart patterns and key support and resistance levels. For more information visit our comprehensive education library

Japanese Q3 GDP revised lower as inflation weighs on spending

Japanese (final) Q3 data was revised lower as inflation appeared to be negatively impacting spending in the region. Inflation has been above the Bank of Japan’s (BoJ) 2% target for more than a year but officials require more convincing before putting an end to years of stimulus, spearheaded by negative interest rates.

BoJ Governor Kazuo Ueda has often listed the preconditions that inflation needs to be stably and consistently above the 2% target and expected to continue in such a manner going forward. The other condition concerns wage growth, which likewise needs to show persistence. Previously, Ueda was confident the bank will have enough data by year end to make a decision on possibly withdrawing negative interest rates, however, recent comments suggest this may be delayed to Q1 of next year, after wage negotiations have taken place.

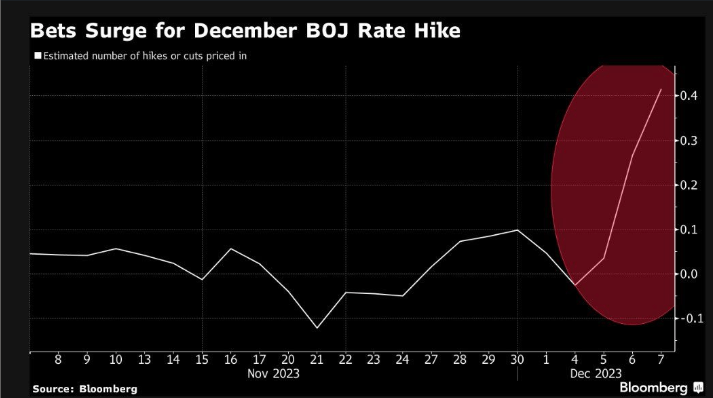

Markets now see credible signs of a BoJ rate hike which has resulted in a notable rise in expectations via interest rate futures. Therefore, the yen has benefitted from the prospect of future rate hikes and stronger Japanese Government bond yields, particularly the 5 and 10 year.

Markets see credible signs of BoJ rate hikes on the horizon (basis points priced in)

Source: Bloomberg

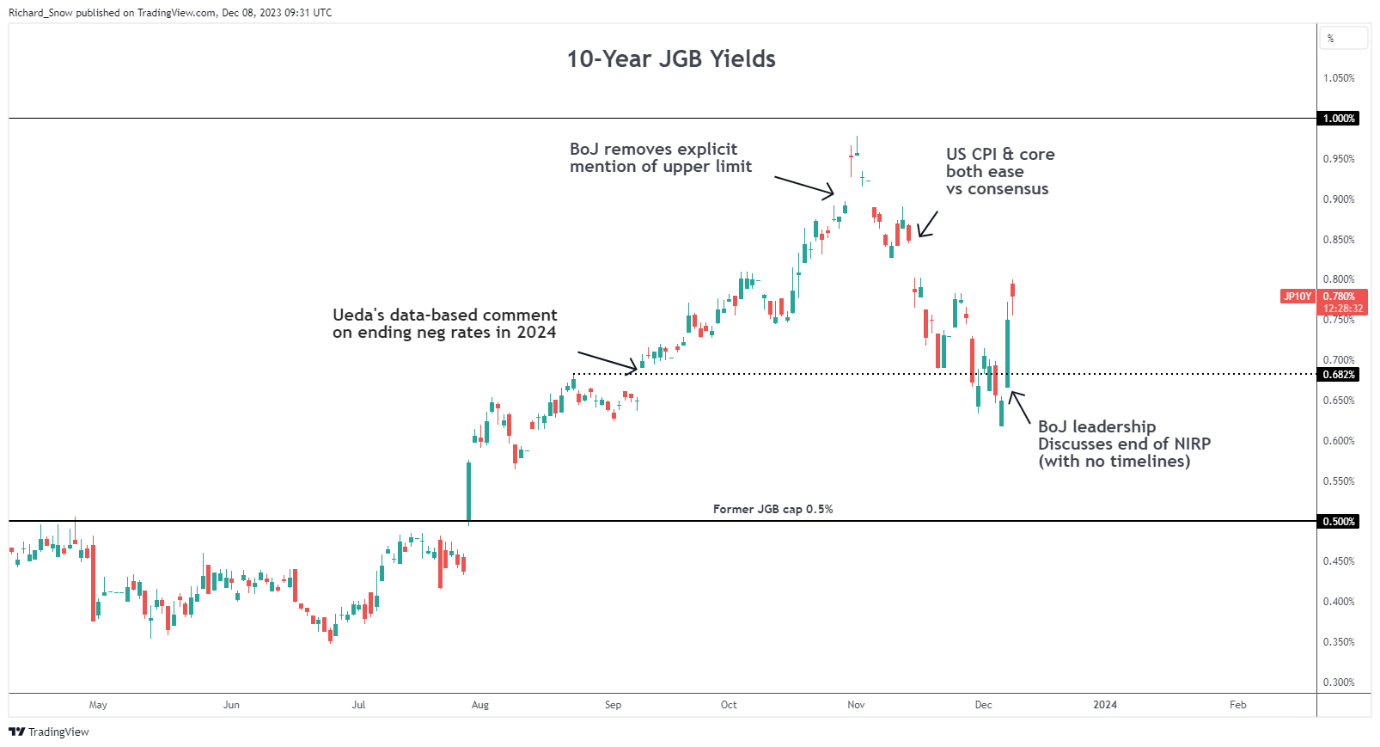

The chart below shows the sharp recovery in Japanese Government bond yields (10-year). The rise is in contrast with the US which is witnessing cooling yields on the basis of increasing rate cut expectations for the world's largest economy. The widening yield differential helps prop up USD/JPY.

Japanese 10-year government bond yields rise

Source: TradingView, prepared by Richard Snow

Non-farm payrolls could extend recent moves on weaker jobs data

This week has shown us that US job openings are fewer than anticipated, people are less likely to quit and ADP private payrolls disappointed expectations. All of these signs point to a potentially disappointing NFP print but with that said, the above-mentioned data points have proven lousy predictors of the NFP print.

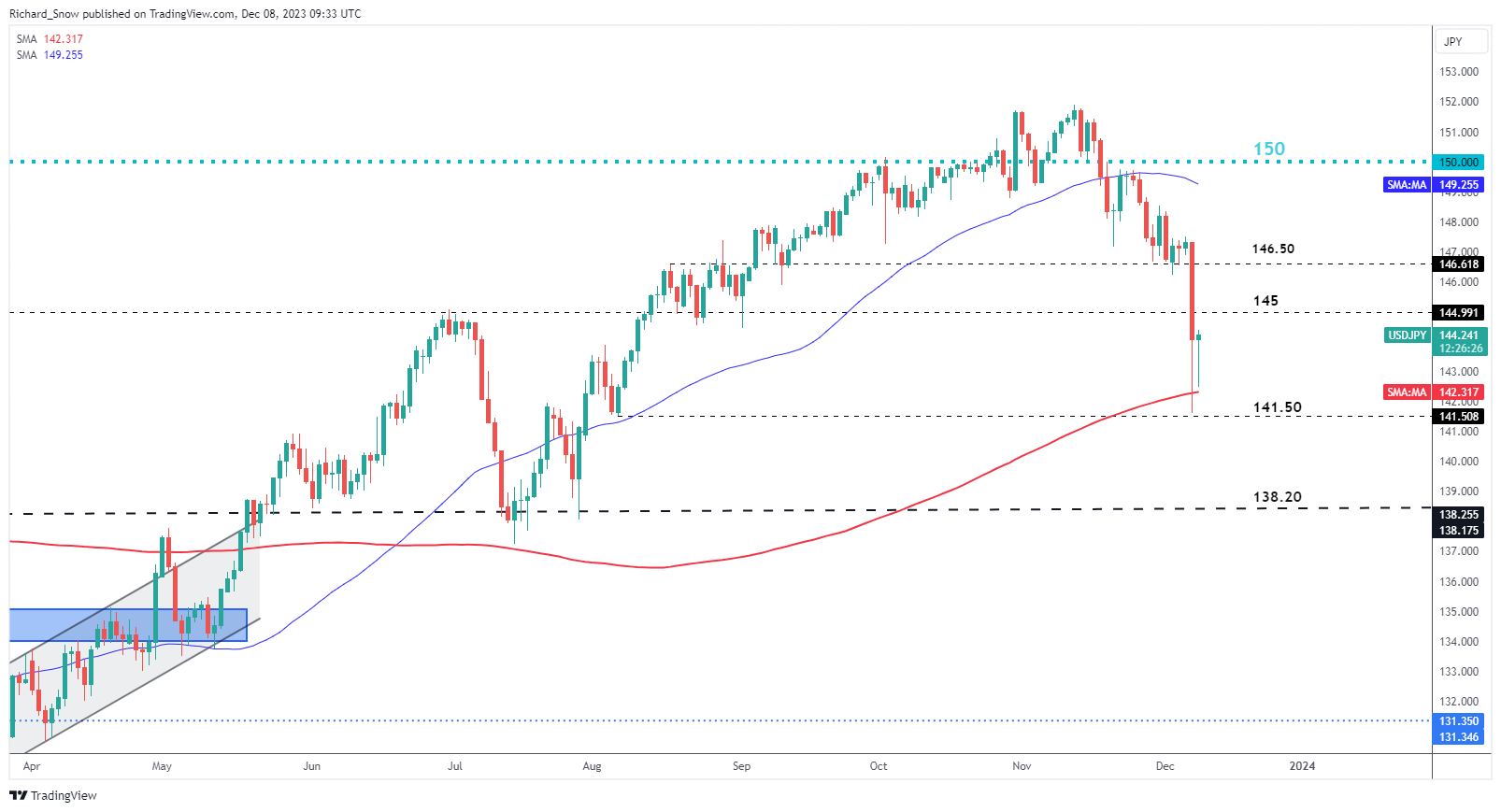

A strong NFP figure could help stall the decline in USD/JPY temporarily but the winds of change are clearly upon us (US expecting cuts, Japan to hike in 2024). A worse than expected number could easily reengage USD/JPY sellers, potentially retesting the 200-day simple moving average (SMA) or even the 141.50 prior low before the week is up. A surprise to the upside in US labor data could see an imminent test of 145 but any longer lasting dollar strength looks unlikely. Another statistic to monitor is the unemployment rate and the market reaction if we are to finally see a tag of the 4% mark as this could cause a greater level of concern that the job market may be easing a little too fast for comfort.

USD/JPY Daily Chart

Source: TradingView, prepared by Richard Snow

https://www.dailyfx.com/news/japanese-gdp-strained-by-rising-inflation-as-boj-spurs-hawkish-bets-20231208.html