like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

Australian Dollar Q1 Fundamental Forecast: Monetary Policy Will Take Center Stage

This article is specifically dedicated to analyzing the fundamental prospects for the Australian dollar. For insights into the Aussie’s technical outlook, request the comprehensive Q1 forecast without delay!

Optimistic Doves Must Proceed with Caution

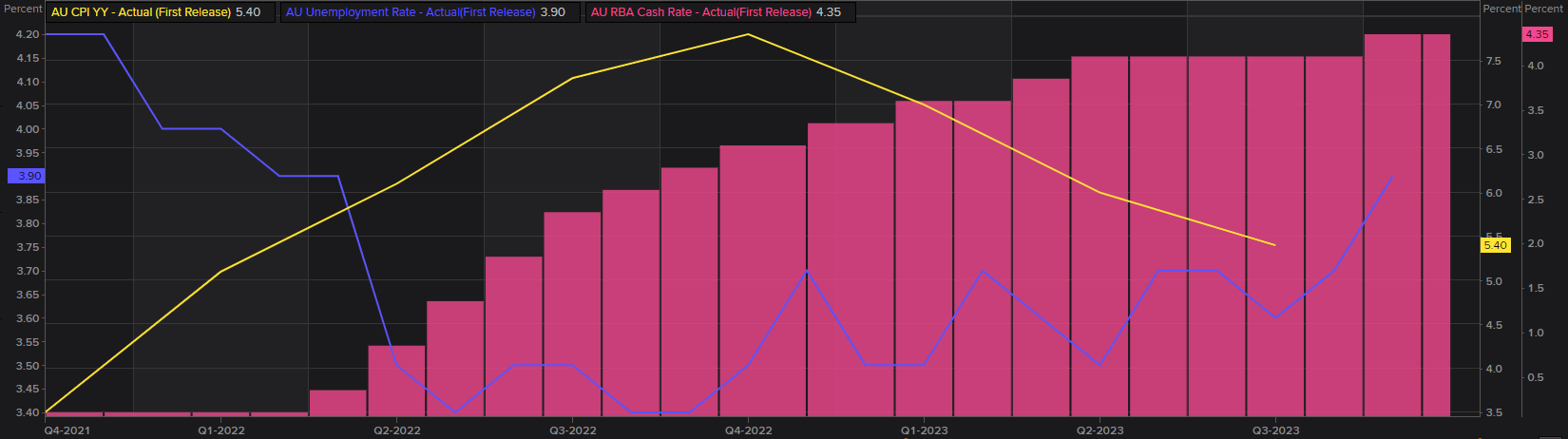

The Reserve Bank of Australia (RBA) ended 2023 by deciding not to raise interest rates for a second consecutive time although the possibility was not ruled out. Members cited disinflation both locally and globally as well as weakness appearing in the labour market. The graphic below illustrates the progress made through restrictive monetary policy measures to reduce inflationary pressures (yellow). While there has been significant improvement, the RBA will have a tough task to juggle the pace of easing as to avoid a resumption of higher prices, thus undoing much of their prior advancements. It is important to note that current headline inflation (5.4%) is far off from the RBA’s target level of 2-3% range with forecasts implying a move back into the desired range in late 2025.

Australian CPI Vs Unemployment Rate Vs Interest Rate

Source: Refinitiv, Prepared by Warren Venketas

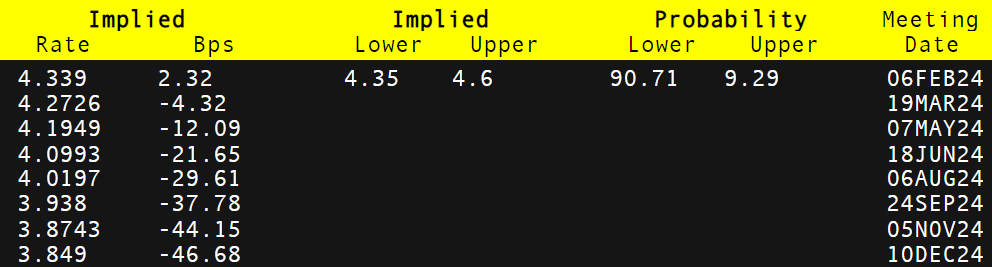

Current money market pricing below suggests that markets expect no additional rate hikes from the RBA in 2024 but with inflation at elevated levels, any external shock may slow this last bid to quell inflation and potentially ‘hawkishly’ reprice rate projections. Data dependency as with many other global central banks will be key for the RBA and consequently forward guidance. If market expectations are to be accurate, both the RBA and the Federal Reserve should have policy rates around similar levels by December 2024 with the Fed scheduled to cut by roughly 143bps versus the RBA’s 46bps. This substantial decline by the Fed could support the Australian dollar over this period; however, with rate cuts unlikely to begin in Q1 of 2024, the pair will be more sensitive to incoming data that could give more colour to the current fundamental backdrop.

Reserve Bank of Australia (RBA) Interest Rate Probabilities 2024

Source: Refinitiv, Prepared by Warren Venketas

Commodities: USD & China

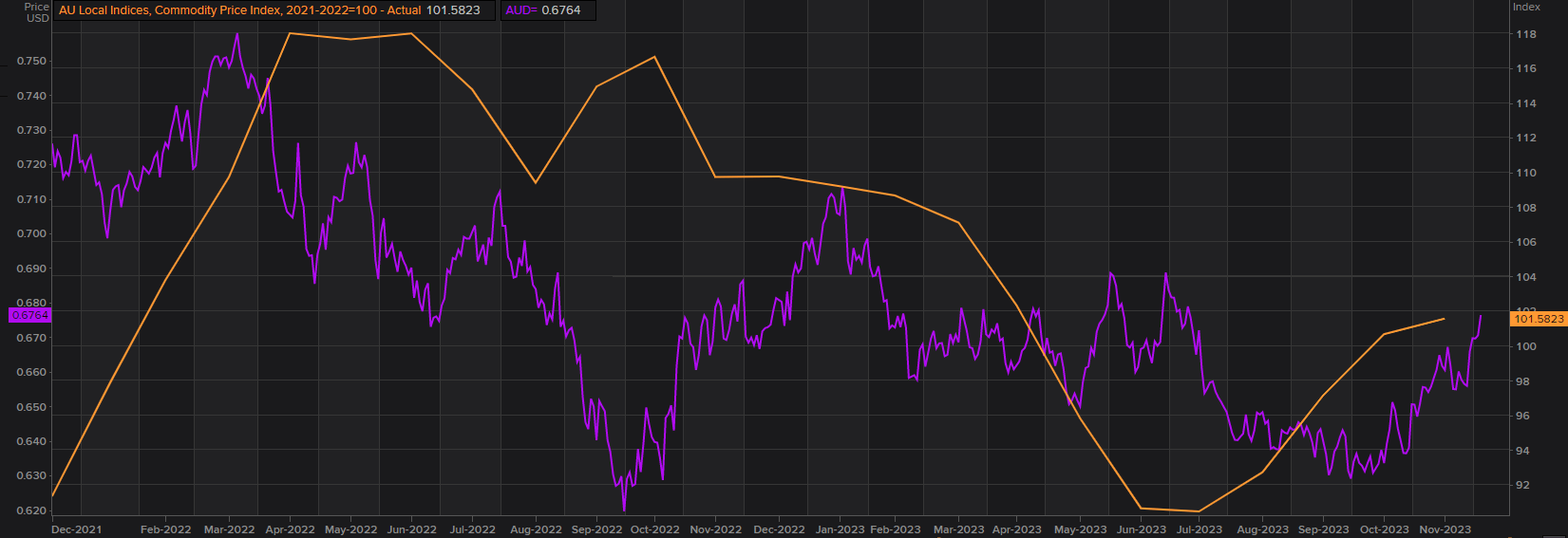

From a commodity perspective, the latter part of 2023 has proven to be encouraging for as reflected by the commodity price index (refer to graphic below). While growth has been limited, Pavlovian response after the Fed’s Dovish December announcement has weakened the US dollar and pro-growth currencies like the AUD have benefitted tremendously. The question going forward is “how long will this last”? The Fed and RBA are yet to pivot but markets have already pre-empted this move leaving incoming data that much more important.

Another key component to the commodity landscape has been China and its close ties with Australian exports. China has not exited from its COVID-19 limitations as many predicted, leaving disinflation, slow growth and grim production (as measures by PMI data) a major concern for the Chinese government. In response, the PBoC introduced stimulus measures to the economy by way of liquidity injections and an accommodative monetary policy stance. Should these channels achieve the required outcome, Australian commodity prices could continue to rise and maintain upside impetus for the Australian dollar.

Australian Commodity Price Index Vs Australian Dollar

Source: Refinitiv, Prepared by Warren Venketas

In summary, AUD/USD could be hampered by the overexuberance of market participants in terms of a turnaround in Fed rhetoric within the first quarter. But as mentioned above, every additional layer of new data focusing on inflation and labor will give more clarity to AUD traders.

https://www.dailyfx.com/news/forex-australian-dollar-q1-fundamental-forecast-monetary-policy-will-take-center-stage-20240105.html