like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

US banks 4Q earnings preview: What to Expect

Article by IG Market Analyst Jun Rong Yeap

US Q4 Bank Earnings Preview

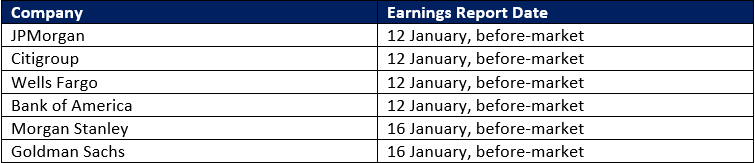

As per tradition, the 4Q 2023 earnings parade will kick off with the major US banks, starting this Friday (12 January 2024) with JPMorgan (JPM), Citigroup, Wells Fargo, and Bank of America (BAC) leading the pack.

US bank stocks: Earnings schedule

Source: Refinitiv

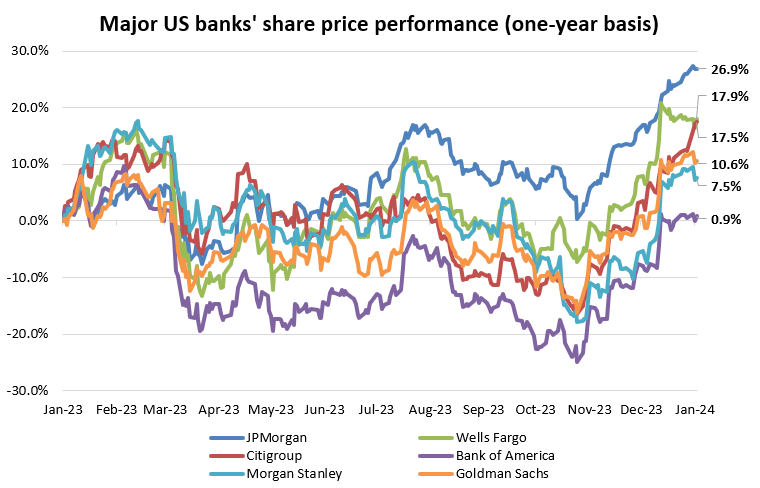

US bank stocks: Share price performance

On a one-year basis, the share price performance for the banks has varied widely. JPM is the clear outperformer with a 26.9% gain over the past year, while BAC lagged the broader industry (+9.3%) with a mere 0.9% gain. Its underperformance may partly be attributed to a slower price recovery from the March 2023 US banking turmoil, given its relatively larger exposure to unrealized losses in its bond portfolio.

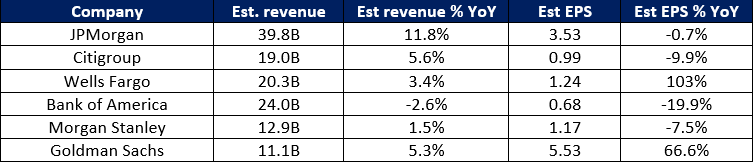

US bank stocks: Revenue and earnings expectations for 4Q 2023

Source: Refinitiv. Data as of 3 January 2024.

For 4Q 2023, expectations are for most major US banks to turn in positive revenue growth from the previous year. Notably, a double-digit growth (11.8%) for JPM is the consensus, with optimism surrounding the revenue and cost synergies brought by the ongoing integration of First Republic Bank into its business.

On the other hand, BAC is expected to be the exception with negative top-line growth (-2.6%) out of the major US banks, while turning in the biggest earnings per share (EPS) decline (-19.9%).

Falling bond yields in 4Q 2023 may offer banks stock some breathing space

4Q 2023 has seen a drastic plunge in bond yields on expectations of rate cuts ahead, with the US 10-year Treasury yields easing sharply from its peak of 5.02% to the current 4.05%. Given that the banks are previously forced to pay up for deposits to compete with higher-yielding instruments, falling yields may aid in easing some pressures on the bank’s funding costs.

The recovery in bond prices in 4Q 2023 may also alleviate the losses on the bank’s securities portfolio, potentially aiding in bringing back some confidence for the stability of the banking sector.

Impact on net interest income on watch

In 3Q 2023, most banks' net interest margins (NIM) largely declined, as banks moved to provide higher deposit costs to limit deposit outflows. Therefore, with the rate narrative pivoting towards lower rates through 2024, eyes will be on the subsequent impact on the banks’ NIM and whether margins can remain supported.

Based on the Federal Reserve (Fed)’s data which tracks commercial bank balances, lending activities in the 4Q 2023 may remain weak, amid tighter lending standards and high interest rates. This seems to be a continuation of the prevailing trend throughout 2023, and market participants will be on the lookout for any positive surprises on the lending front from the banks.

Validation for soft landing hopes on the lookout

With market participants basking in hopes of a soft landing scenario into 2024, the banks’ guidance will be closely watched for validation of a resilient economy. During 3Q 2023, the major banks have provided lower-than-expected allowance for credit losses, with a decline from 2Q 2023.

The extent of provisions for credit costs provides a gauge of economic risks that the banks foresee, therefore, market participants will want to see loss provisions moderating further towards ‘normal’ levels (levels preceding the Covid-19 pandemic) to support views of a soft landing.

The banks have also previously guided that US consumers' finances remain healthy while noting some resilience in US economic conditions, which leaves views in place for similar positive guidance ahead.

Improved risk environment may support investment banking and wealth management activities

Following a disappointing first nine months of 2023 in investment banking activities, expectations are in place that better times are ahead, with resilient economic conditions and a different course of rate outlook into 2024.

The improved risk environment seen in 4Q 2023 could be supportive of such views and with early signs of revival in deal-making, market participants will want to see the positive impact being reflected in the banks’ results, although it may come with a few months lag. Nevertheless, any signs that the worst is over on that front will be very much cheered and may help to contribute to the banks’ earnings recovery.

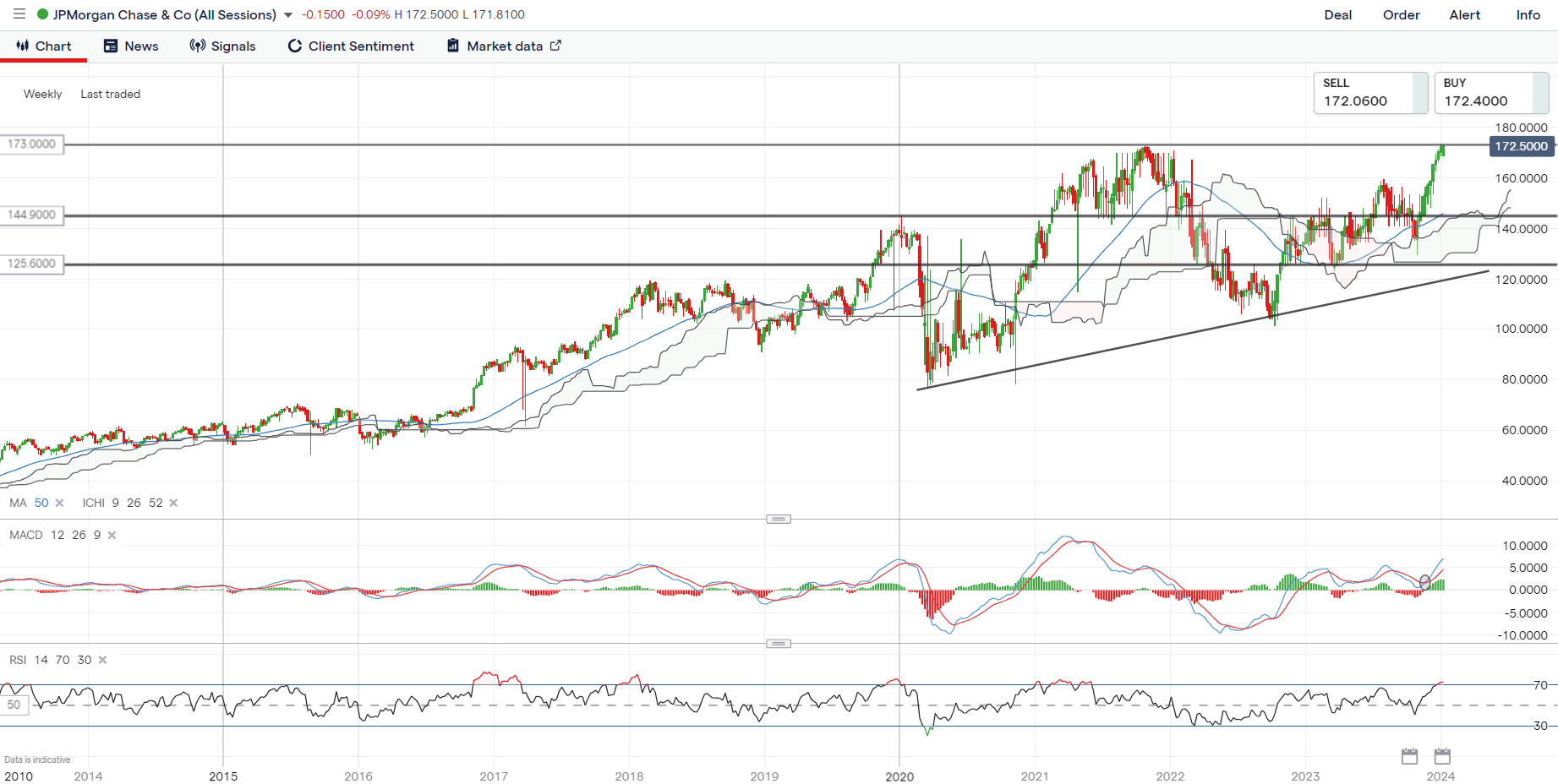

Technical analysis – JPMorgan’s share price hovers around record high

JPMorgan’s share price briefly touched a fresh record high last week for the first time in more than two years, hovering around its October 2021 peak at the US$173.00 level. Near-term overbought technical conditions may call for some cooling in its recent rally, but any sell-off could still be a near-term retracement within a broader upward trend at the current point in time. Prices continue to trade above its Ichimoku cloud support on the weekly chart, alongside various moving averages (MA) which keep the bullish bias intact. On the downside, the US$166-$168 level may serve as a support zone to hold with recent consolidation.

Source: IG Charts

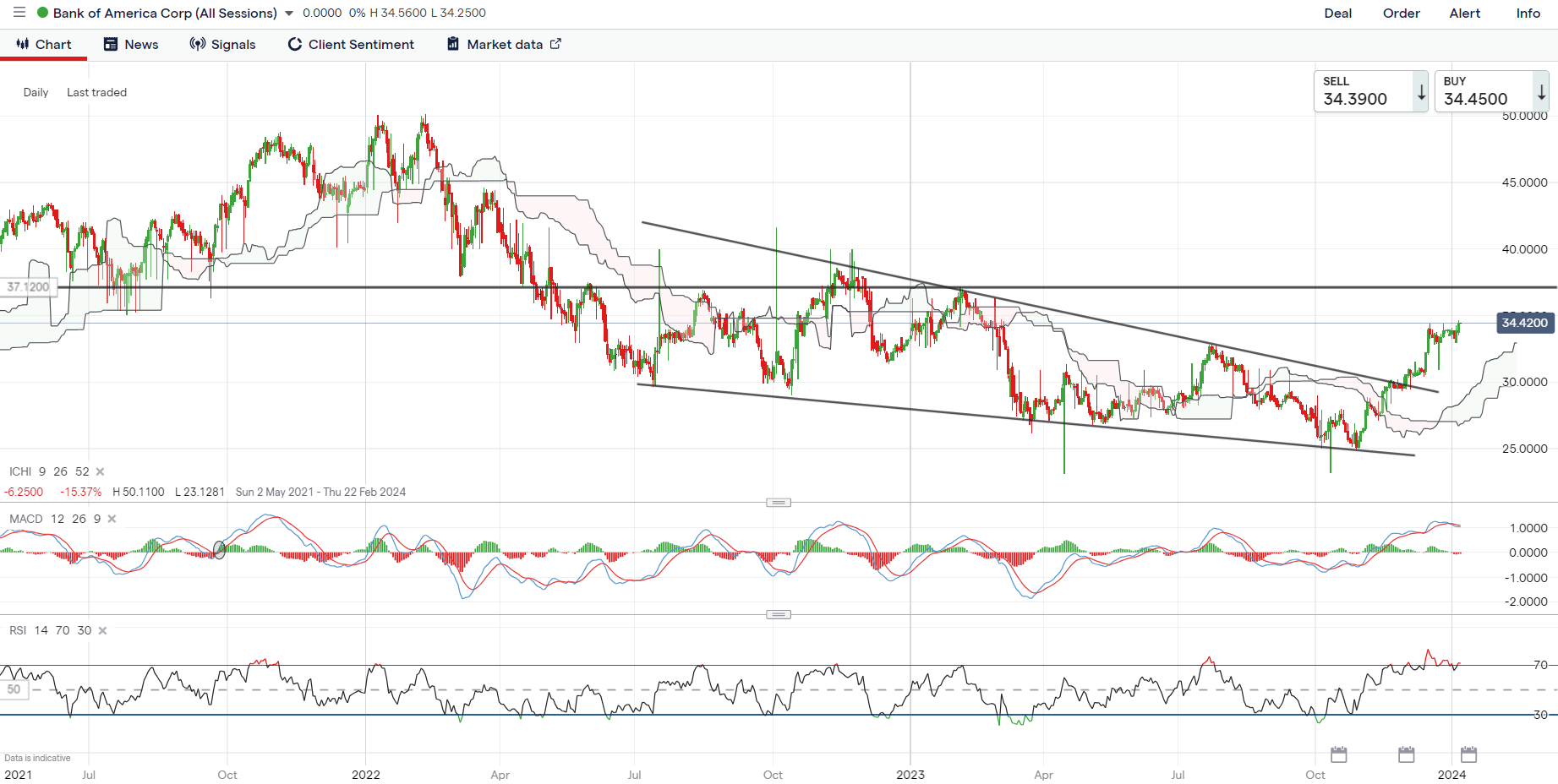

Technical analysis – Bank of America’s share price showing some signs of life

Despite underperforming the broader industry for the bulk of 2023, BAC share price has been showing some signs of life lately, having broken above a broad descending wedge pattern in November 2023. Notably, on the weekly chart, its share price has overcome its Ichimoku cloud resistance for the first time since March 2022, while its weekly moving average convergence/divergence (MACD) headed above the key zero mark as a sign of building upward momentum. Further upside may leave its 2023 high at the US$37.12 level on watch for a retest, while on the downside, recent consolidation leaves US$32.84 as potential support to hold.

Source: IG Charts

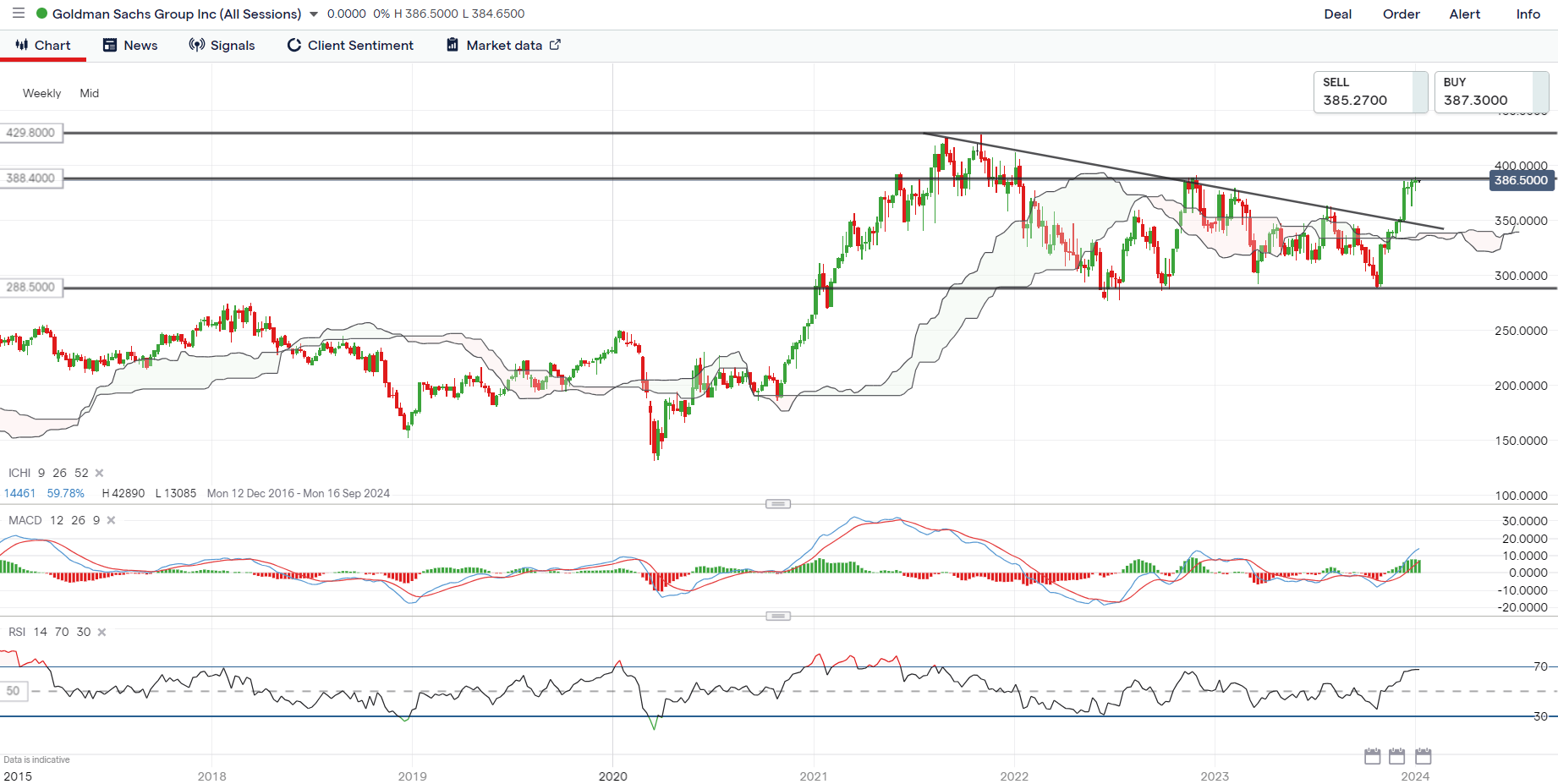

Technical analysis – Goldman Sachs’ share price broken out of descending triangle

Goldman Sachs’ share price broke out of a broad descending triangle last month, moving on to retest the US$388.40 horizontal resistance, which marked its November 2022 peak. Similarly, on the weekly chart, its MACD has also reverted back above the zero level as a reflection of building upward momentum. Overcoming the US$388.40 level of resistance may leave its all-time high at the US$429.80 level on watch next.

Source: IG Charts

https://www.dailyfx.com/news/us-banks-4q-earnings-preview-what-to-expect-20240111.html