like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

Daily Market News

Japanese Yen Q2 Fundamental Forecast: Brighter Days Ahead, Catalysts to Watch

Market Recap: Another Bad Quarter

The Japanese yen took a beating during the first three months of 2024, depreciating sharply against the U.S. dollar, the euro, and the British pound, with the bulk of this weakness stemming from monetary policy divergence. While top central banks such as the Fed, ECB, and BoE kept rates at multi-decade highs to defeat inflation and restore price stability, the Bank of Japan stuck to an ultra-loose stance for the most part, amplifying the yield disparity for the Japanese currency.

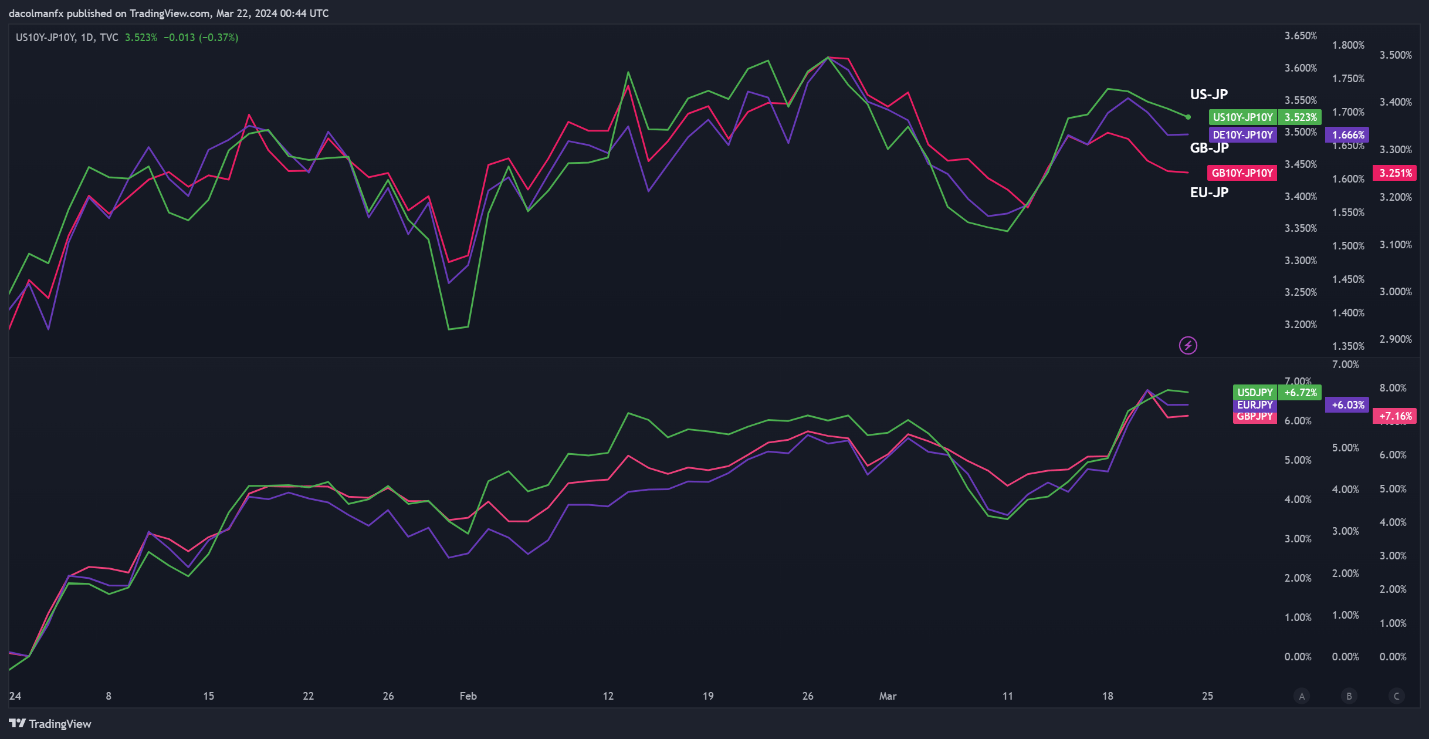

The chart below shows how USD/JPY, EUR/JPY, and GBP/JPY have performed year-to-date (as of March 21). It also showcases the widening yield differentials between the US, Eurozone, and UK 10-year government bonds and their Japanese equivalents – a bearish catalyst for the yen.

Japanese Yen Performance and Yield Differentials in Q1

Source: TradingView, Prepared by Diego Colman

BoJ Abandons Negative Rates in Seismic Shift

A significant shift occurred towards the end of Q1. In a historic move, the BoJ raised borrowing costs from -0.10% to 0.00%-0.10% at its March gathering – the first hike in 17 years. This marked the end of the bank’s longstanding experiment with negative rates designed to stimulate the economy and to break the deflationary "mindset" of the Japanese people. In this meeting, the institution led by Kazuo Ueda also announced it would end its yield curve control regime and cease purchases of ETFs.

The decision to start unwinding stimulus came after salary negotiations between Japan’s largest federation of trade union groups and the biggest corporations resulted in bumper pay hikes for workers in excess of 5.2%, the highest in more than 30 years. Policymakers believed that strong wage increases would foster durable economic growth, creating a virtuous spiral of sustainable inflation of 2.0% underpinned by robust domestic demand.

Despite the BoJ’s pivot, the yen continued to wither, showing paradoxically little signs of recovery in the days that followed. The reason: markets perceived the central bank's liftoff as a "very dovish hike" and were betting that financial conditions would still remain extremely loose for a long period, meaning a very slow normalization cycle. According to their logic, this would ensure that Japan's yield disadvantage vis-à-vis other economies would be maintained for the foreseeable future.

Clearer Skies Ahead

The second quarter may herald a bullish shift for the yen, although this may not happen immediately. One potential driver could be the Bank of Japan's tightening campaign. Although the BoJ signaled neutrality and did not provide clear guidance on when to expect another rate rise after concluding its March meeting, the next adjustment could arrive in July or more likely in October, just as the Federal Reserve, the ECB and BoE begin to dial back on policy restraint.

With the yen languishing at multi-year lows and rising oil prices globally, headline inflation in Japan, which accelerated to 2.8% y-o-y in February and marked the 23rd straight month being at or above BoJ’s target, could remain skewed to the upside. This situation, coupled with government officials' dissatisfaction with the currency's extreme weakness and desire to reverse the trend, increases the likelihood of seeing another BoJ move sooner rather than later. Traders may be underestimating this risk.

There is another variable that could prompt the BoJ to take action earlier than many anticipate: reports that many Japanese companies are front-loading capital spending and rushing to obtain bank loans before lending costs rise again. All things being equal, this is positive development that could underpin economic activity and boost demand-pull inflation in the coming months, giving policymakers more confidence in the outlook to press forward with another hike.

Repatriation of Funds Underway

In recent years, Japanese investors, contending with Bank of Japan’s ultra-dovish posture and unorthodox monetary policy, had no choice but to deploy their capital oversees, dispatching more than $4 trillion of funds in pursuit of higher yields. Despite the significant currency-hedging costs associated with this strategy, it was the go-to option for local investors seeking more attractive investments opportunities abroad in quality assets.

With the BoJ finally unwinding stimulus and other central banks going in the opposite direction, Japanese investors could soon start liquidating positions in foreign assets, repatriating funds to their homeland in an orderly process - a development that would boost demand for yens. This won't happen overnight, of course, but the reversal of trillion-dollar flows should be a tailwind for the yen in due course, paving the way for a more durable rebound.

Fundamental Outlook

Looking ahead to the second quarter, the yen appears better positioned for stability and a potential turnaround. This optimism isn't solely a result of the Bank of Japan's exit from negative rates. The imminent easing cycles of the Federal Reserve, European Central Bank, and Bank of England are poised to provide added reinforcement. With that in mind, we could see USD/JPY, EUR/JPY, and GBP/JPY drift progressively lower over the coming months.

https://www.dailyfx.com/news/forex-japanese-yen-q2-fundamental-forecast-brighter-days-ahead-catalysts-to-watch-20240330.html