like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

The US has announced a 10% baseline tariff effective 5 April, along with additional individual reciprocal tariffs of up to 49% on some economies beginning 9 April. The previously announced 25% tariff on autos is expected to take effect from 3 April.

For the US, tariffs remain a key tool for negotiations. If maintained, the announced tariffs could cut expectations for global economic growth and corporate profits, and lift fears of supply chain disruptions and result in higher finished goods prices.

Mexico and Canada are exempt from any new tariffs as they continue to negotiate with the Trump administration on immigration, border security and the drug wars.

Many of the US trading partners should have sufficient time to at least start negotiating with the Trump Administration, and the hope is that they hold back on any retaliatory measures, which could otherwise further escalate this tension into a broader trade war.

Source: The White House, HSBC Global Private Banking and Wealth as at 3 April 2025.

Key highlights of the announcements:

We are not making further revisions to our global growth forecasts which were already lowered to 2.5% in March, due to the tariffs already announced. President Trump has indicated room for negotiation by asking the trading partners to reduce the barriers they put up to US firms. But the executive order also said tariffs could rise further if there is retaliation or if, for example, trade deficits widen.

Going forward, if Trump is able to incorporate a lower corporate tax rate (from 21% to 15%) in the next budget, it could result in an expansion of production in the US by foreign companies who choose to move production to the US. This could result in increased revenues as more production and job opportunities emerge in the US economy and would then lower the trade deficit, which is a positive factor for US financial markets.

Liberation Day will probably not represent the bottom for US equities. Much uncertainty remains about the breadth and depth of tariffs and the ensuing negotiations that the Trump administration is currently engaging in.

It is unlikely that we will see the net alpha shift upward in prices and subsequent resumption of disinflation in time for the Fed to ease in June. Once the market understands that the likelihood of a Fed cut in June is not properly priced in, it could create further volatility for US equities. Currently, the market is attaching a 70% probability of a Fed cut in June, which seems high.

We expect to see continued volatility in both US equities and bonds in the short term, driven by the combination of the budget battles, treasury issuance, and tariff and trade policy.

From a medium-term perspective, though, negotiations should reverse some of the tariffs, while US innovation and re-onshoring should help. There is also the potential for tax cuts to bring better news.

Source: Bloomberg, US Census Bureau, HSBC Global Private Banking and Wealth as at 3 April 2025. Forecasts are subject to change.

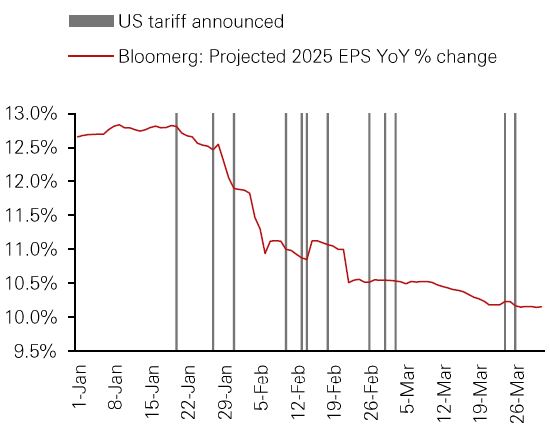

Bloomberg’s projected 2025 EPS growth dropped from approximately 13% at the start of the year to around 10% by end of March. The downward trend accelerated in February, coinciding with more frequent and broader tariff measures.

Europe’s stock market rally may see a pause as negotiations start. Automotives are vulnerable but the absence of a pharma tariff is good news. The UK got a relatively lower tariff, but its open economy makes it vulnerable – not retaliating could help cap inflation and support gilts.

The largest US trade deficit is with China, totalling – USD295 billion, reinforcing China’s central role in the trade policy debate. In China and the rest of Asia, we continue to favour domestically oriented businesses. We also think that regional integration will further accelerate.

https://www.hsbc.com.my/wealth/insights/market-outlook/special-coverage/liberation-day-an-opening-salvo-to-negotiate-creates-further-uncertainty/