like_count_tpl like_count_text_tpl

like_tooltip_tpl

comment_count_tpl comment_count_text_tpl

comment_tooltip_tpl

The Liberation Day announcement on 2 April triggered a 13% sell-off of the S&P 500, but markets bounced sharply yesterday, reducing the damage to ‘just’ 4% from the 1 April closing price. Non-US markets are also bouncing.

The trigger was yet another surprise announcement by the White House that most countries will be given a reprieve of 90 days on the reciprocal tariffs, meaning that the 10% blanket levy now applies to most countries. The (very important) exception is for imports from China, which saw their tariff raised further, to 125%; China’s own tariff of 84% on US imports comes into force today. Many commentators now assume trade between the US and China will collapse.

While the US President did acknowledge the market turmoil, we think it would be too optimistic to assume that there is some kind of ‘government put’ protecting us against equity market downside. Tariffs have only been delayed and significant concessions from other countries will be needed to avoid them being imposed in 90 days time. The question is whether countries are willing and able to give in to the high US demands.

The main positive is that fears of a financial market meltdown should now ease. The Federal Reserve’s intervention through Treasury purchases or liquidity measures no longer seems needed for now. Volatility has come down and Treasury markets have recovered sharply. It also means, however, that markets no longer expect four or five rate cuts this year, but only three, which aligns with our assessment.

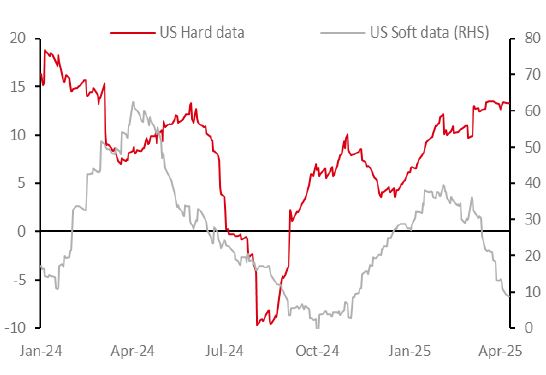

We think investors will start to look at growth, inflation and earnings fundamentals again. In fact, US consumers had already started to worry about signs of some weakening in the labour market and a re-acceleration of inflation as a result of the tariffs. The 125% tariff on Chinese imports will have a big effect on consumer prices.

For companies, not every import from China can easily be substituted by another provider. Even if the final good can be made locally or outside of China, some of the components may still need to be sourced from China. As a result, growth and inflation pressures remain.

Uncertainty is another negative as it delays investment and spending decisions, and – unfortunately – that uncertainty is further extended due to the 90-day reprieve.

Overall, we think markets will no longer assume a US recession as their base case, but it remains a risk. And we believe that companies will start to guide down earnings expectations more actively, which should hurt cyclicals vs defensives, goods vs services, and big importers compared to more local players.

Source: Bloomberg, HSBC Global Private Banking and Wealth as of 10 April 2025.

We think US growth and earnings continue to be more negatively affected by the tariffs than in Europe, Japan and India, for example. That’s to a large extent because of the very broad-based tariffs, which mean that US importers cannot find any imports without levies. That increases their cost base, margin pressures and inflation pressures. Companies elsewhere in the world on the other hand can find plenty of goods without tariffs.

We also believe that foreign companies and countries will continue to build regional networks to secure new suppliers and new markets. The announcement by the UK and India that they are in the final stages of a trade deal is just one example.

Investors who try to time the market have been shown that this is very difficult to do. Panic-driven moves may have led some people to sell on Tuesday and miss the rally on Wednesday. Once again, volatility spikes do not tend to last long. The strongest days often follow the weakest days, and investors better stay in the market to avoid missing those bounces. Diversification and a focus on quality are a much better strategy.

We focus on multi-asset strategies with an active approach as managers can actively take advantage of opportunities and dislocations when they occur (without the need to forecast everything). We favour quality assets with stable cash flows – which include high rated bonds and defensive stocks with strong market positions. High yield bonds are less preferred as spreads look somewhat tight compared to their usual relationship with equity volatility.

As for Chinese markets, our focus on domestically oriented companies is even more important now than before. That said, China’s onshore and offshore equity markets have stayed relatively resilient as compared to the sharp selloff in the US market in recent weeks. Many investors don’t know that the MSCI China has only very limited exports goods sales exposure to the US at only 2% (exports to the US account for only 2.5% of China GDP). We expect severe tariff headwinds to prompt the Chinese government to further ramp up fiscal and monetary stimulus to strive for its 2025 GDP growth target of “around 5%”. The DeepSeek-driven AI innovation and investment boom should offer an important domestic growth engine to mitigate the impact from reciprocal tariffs. We like the domestically-driven sectors of consumer discretionary and financials in Asia but think technology hardware companies are significantly exposed to US tariff and growth risks.

https://www.hsbc.com.my/wealth/insights/market-outlook/special-coverage/90-day-tariff-reprieve-can-the-bounce-last/